Premium Value of an Option

|When trading options, you are trading premium value. If you buy an option, you want to sell it in the future for a higher premium, and if you sell an option, you want to buy it back for less.

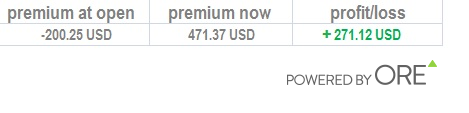

Buying an option

In the example below, the option holder has paid 200.25 USD to buy an option and now it is worth 471.37 USD, hence the profit is 271.12 USD.

{kind=link}

Selling an option

In the example below, the option writer (seller) received 450.95 USD when he sold an option and now it is worth 149.56 USD, therefore he can buy it back for less and his profit is 301.39 USD.

Premium value is comprised of two parts: Intrinsic value and time value. These values change as the underlying market changes.

Premium = Intrinsic Value + Time Value.

Intrinsic Value

This is the portion of the premium that depends on the difference between the strike and the market rate. When the option is in-the-money (when the strike rate is better than the market rate) the option has intrinsic value. But if the option is out-of-the-money or at-the-money (when the strike is worse than or equal to market), the intrinsic value is zero. When intrinsic value is zero, it does not mean the premium is zero as it may still have time value!

Example

Let’s say you buy a EUR/USD Call with a strike of 1.1200 and an amount of 100,000 EUR, as per the option trade details in this image:

If the underlying market is trading at 1.1300, your strike rate (to buy) is 100 pips better than the market, hence your trade is in-the-money (ITM). We calculated this by subtracting the market rate (1.1300) from the strike rate (1.1300) giving us 0.0100 or 100 pips. In fact, on expiry the spot is trading above 1.1200 (the Call with the strike 1.1200), the Call option has intrinsic value.

Intrinsic value = Amount x Difference between market rate and strike rate

= 100,000 x (1.1300 – 1.1200)

= 100,000 x 0.0100

= $1,000.

Therefore, the Call option’s premium = $1000 + Time Value.

Time value

Time value, also known as extrinsic value, is the portion of the premium left after deducting the intrinsic value and is determined by external factors: Time Value = Premium – Intrinsic Value.

Premium can increase or decrease depending on time value and the two main external factors are time until expiry and implied volatility.

Options with a longer expiry are more expensive since you are buying more time for the market to move in your favour. The opposite is also true, options with a closer expiry cost less. When holding an option, the expiry date moves closer for each day passing. The time value portion of the premium declines reflecting this. The process of time value declining each day is known as time decay. Values at expiry have no time value, hence they are intrinsic value only.

Net Present Value (NPV)

Net Present Value (NPV) figures are an indication of what your option trade’s ‘premium now’ would be if the market moved. The indication is based on the current market environment. NPV is useful to forecast the trade’s pay-out.

If you are long (by buying) an option, then the NPV value will be positive and this is the amount you will receive when you sell your option back. The example below is a snap-shot of the optionsReasy sensitivity table for a long Call option. The NPV column indicates how the option’s value increases as the underlying market rises.

If you are short (by selling) an option, then the NPV value will be negative and this is the amount you will pay to buy back the option. The example below is a snap-shot of the optionsReasy sensitivity table for a short Call position. The NPV column indicates that the cost to the seller increases as the underlying market rises.

Volatility

The marketplace’s consensus on future volatility affects an option’s premium (time value portion). This is known as implied volatility (IV). If the market is expecting more volatility, you will pay more for the option. If there is increasing volatility, it is more likely the market will move in your favour.

Tips:

- If the implied volatility increases after an option trade has been purchased, this is good for the buyer and bad for a seller. Buyers like increasing volatility!

- At any time, your option’s premium will be at least the intrinsic value. At expiry, time value = 0 and the premium = intrinsic value.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.