Collars As a Protective Measure

|In the last two weeks’ articles, links here, I discussed some strategies that can be used to protect a stock portfolio from market crashes. Today we’ll continue that discussion.

In the first of the two articles, I listed four possible protective strategies:

Hold long-term positions, and buy put options as insurance.

Add covered calls to the long stock and puts, creating collars.

Substitute bullish vertical spreads for the collars, reserving the excess cash.

Convert most of a portfolio to cash. Use a small percentage to buy long-term call options to maintain exposure.

Last week we discussed alternatives 1. and 4., and demonstrated why they are actually two forms of the same trade. Today let’s tackle alternative 2., the collar.

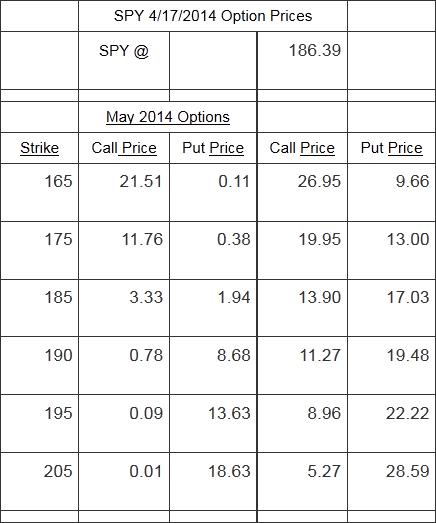

In the earlier articles, I listed some relevant option prices. Today I’ll update the example. The day of this writing happens to be an option expiration day, so it’s a nice cutoff point. The May options are now the next upcoming monthly options expiration, which is called the “front month.” Here are some selected current option prices:

{kind=link}

It is estimated that SPY will pay $5.25 in dividends between now and the December 2015 expiration.

With the current risk-free interest rate of .25%, carrying a position worth $186.39 for 20 months would cost about $.78 in interest.

Let’s look at the collar strategy as an extension of the protective put strategy.

With the SPY currently at $186.39, we could buy December 2015 put options at the 185 strike price for 17.03. These put options give us the right to sell SPY shares at $185 at any time through December 19, 2015, 20 months away. Our maximum loss on this position would be the drop from $186.39 to the $185 strike price, or $1.39; plus the $17.03 cost of the puts, for a total of $18.42 per share. Against this we would collect $5.25 in dividends, and have to pay or forego about $.78 in interest to carry the position. Our maximum net loss is thus (Stock price – put strike + put cost – dividends received + interest paid) = ($186.39 – $185 + $17.03 – $5.25 + $.78) = $13.95. This is about 7.5% of the current value of SPY.

So far our upside would still be unlimited, after overcoming the extra overhead of the cost of the puts. The puts would increase our break-even price to (stock price + put cost – dividends received + interest paid) = ($186.39 + $17.03 – $5.25 + $.78) = $198.95. We would have a profit at any SPY price above that at the December 2015 expiration, and our profit would be unlimited.

This is called a married put position. It can be used on its own, or as a subassembly of other positions, including the collar position, described below.

We could now take steps to recover some of the money spent for the protective puts, in the process creating the collar.

The December 2015 205-strike calls are now selling for $5.27. If we sold those calls, together with our married put position, the resulting position would be a collar. This would cut our maximum loss down by the call proceeds of $5.27, from $13.95 to $8.68. It would also reduce our break-even price by the same amount, from $198.95 down to $193.68

We could still profit on the SPY stock until it exceeded the 205 call strike. We would not participate after that, since we would be obligated to sell the SPY at that $205 strike price if SPY exceeded it at the December 2015 expiration. Our maximum profit would be the $205 strike/sales price, less our break-even price of $193.68, or $11.32

The new collar position, then, would look like this:

Maximum profit (at $205 or more on SPY): $11.32

Maximum loss (at $185 or less on SPY): $8.68

Break-even: $193.68

This does not seem all that attractive. Although our loss is now limited, so is our profit. We could allow for higher profit by selling calls at higher strikes. But the cost reduction from those higher strike calls goes down pretty fast.

There is another way we could make this collar potentially work better. This is by diagonalizing it. This means that we would keep the stock and the December puts. But instead of selling one call 20 months out, we sell 20 one-month calls, one after the other.

This has a couple of benefits:

With the calls closer in time, we can select an appropriate strike price each month based on the then-current price of SPY. We can give ourselves just enough room overhead to keep the call strike above the probable range. These strike prices will be nearer the current price than the 205 strike is now.

Options with only one month to go decline in value much faster than options with a long time to go. We will be collecting time value at accelerated rates. Meanwhile the time decay of our long-term puts will be very slow.

Together, these two points combine to produce a high probability that we will eventually collect much more for the 20 combined one-month calls than we would have collected for the one 20-month call.

Let’s see how this might work.

The May 190 calls are currently at $.78. The 190 strike price is above the weekly Bollinger Band on the SPY, so it is outside the probable range. 190 is also above the recent high, so there is built-in resistance there. If we sold those May 190 calls instead of the December 205 calls, our cost would not be reduced very much in the short term. But if we sold calls at a similar distance away every month for 20 months, our cost would eventually be reduced by 20 * $.78 = $15.60, almost completely paying for the $17.03 cost of the long-term put protection. We would end up with the SPY free and clear, at whatever price it might be at the December 2015 expiration, and with the 20 months of dividends in our pocket.

There are a couple of caveats about this position:

If the price of SPY shoots up above any of our monthly strike prices, our profit for that month drops off and can go negative, as the put value falls. We would then be forced to roll the calls to maintain the position, possibly at a loss.

If implied volatility is very low in the future, the amounts received for the calls would be lower (on the other hand, if IV goes up, those amounts could be higher).

On the whole the diagonalized collar is a method worth considering for protecting the value of a stock portfolio at a low cost.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.