Using Options to Protect Profits

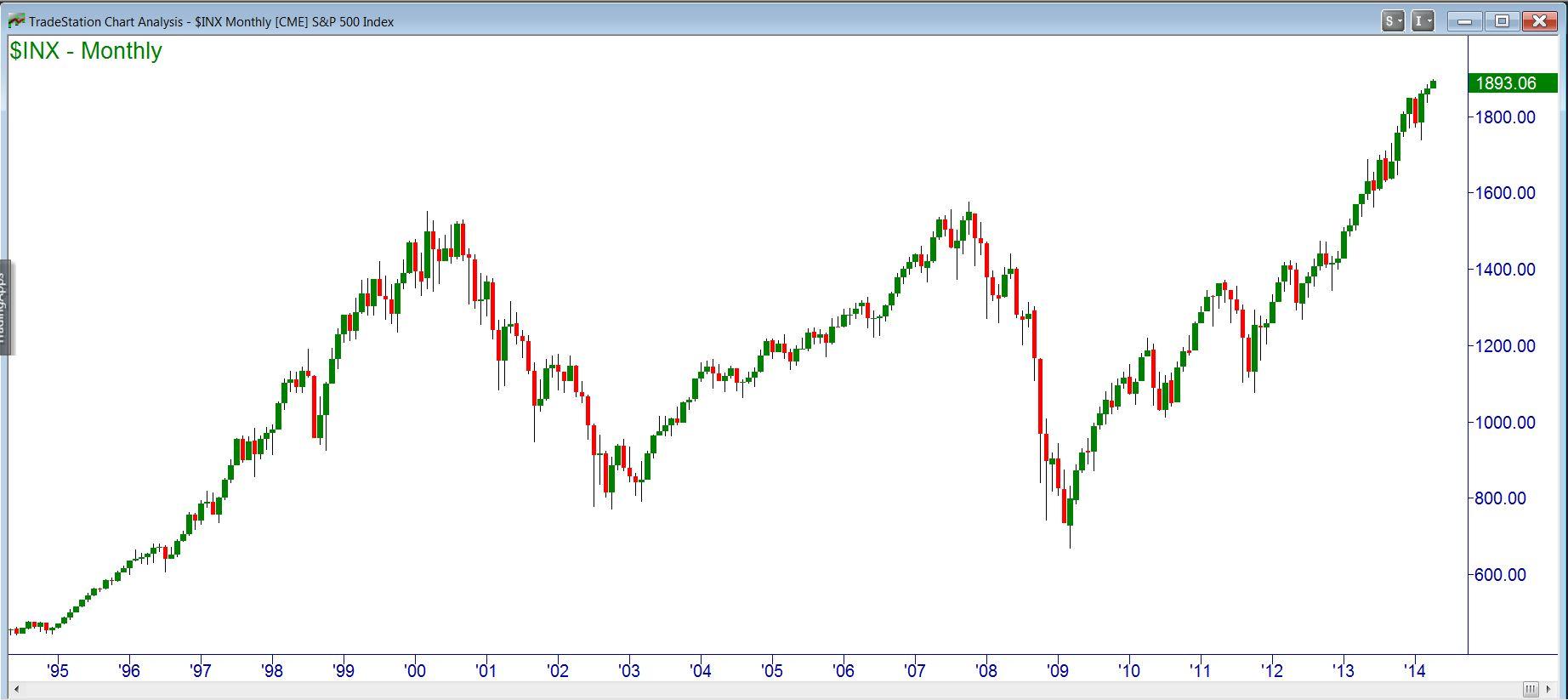

|On April 2, 2014, the S&P 500 Index notched yet another all-time high, closing in on the 1900 mark (points, not the year). From the lows following the 2008-09 crash, the index has climbed by over 180%. It has exceeded the 2007 high by over 20% (in nominal terms).

Here is the chart of the S&P 500 as it stood on April 2, 2014:

{kind=link}

In real (inflation-adjusted) terms, the index had exceeded the 2007 high, and was within a hair of exceeding the real all-time high, which was made in 2000.

The following chart, from multpl.com, shows the long-term inflation-adjusted chart for the index:

{kind=link}

After a run like this, an increase of 180% from the 2009 lows, could the top be far away?

Well, yes, it could. Or not.

When the great bull market of 1982-2000 had come this far, it was just getting started. Anyone who got out after “only” 180% missed most of a bull market that eventually saw over a 1200% gain.

So where are we now? Standing on the brink of a great crash, as in 2007? Or just in the warm-up stages of another epic bull, as in the 80’s?

I don’t know. Neither do you, nor does anyone else. There are excellent, nearly irrefutable arguments for both sides of that question. You hear them every day from all of the talking heads.

So, in practical terms, how can we continue to participate in further upside moves, while protecting ourselves in the event of a crash?

Here are a few alternatives using options:

Hold long-term positions, and buy put options as insurance.

Add covered calls to the long stock and puts, creating collars.

Substitute bullish vertical spreads for the collars, reserving the excess cash.

Convert most of a portfolio to cash. Use a small percentage to buy long-term call options to maintain exposure.

Let’s look at each one briefly today. In the future we’ll explore them in more detail.

1. Hold long-term positions, and buy put options as insurance.

This is a very straightforward way to buy protection. In this simplest of all uses of options, we just buy ourselves an insurance policy. If the bull market continues, we participate fully, minus the cost of the insurance. Here are two slightly different ways this could work:

First alternative: With the SPY (the exchange-traded fund that tracks the S&P 500 index) around 189, options are available as far out as December, 2015. We could buy a zero-deductible policy by buying the December 190 puts for about $18. The 9.6% cost , over the 623-day term of the puts, amounts to an annual premium rate of about 5.6%.

Second alternative: Buy a cheaper policy with a higher “deductible.” If we are willing to absorb a 10% loss in our portfolio before our insurance kicks in, the cost will be less. The December 2015 puts at the 170 strike would cost about $10.50. This amounts to an annual premium cost of about 3.2%

With both of these alternatives, our upside profit is unlimited, while our downside is protected. Which of the two will pay off better depends on how severe any downturn might prove to be. If there is no downturn, then no insurance would have been best. If losses turn out to be only minor, then the cheap insurance will have been adequate. If the market tanks severely, the buyer of the zero-deductible policy will look like the genius.

2. Add covered calls to the long stock and puts, creating collars.

In this variation, we add short calls to our long stock and long puts. The calls pay part or all of the cost of the puts. The tradeoff is that our upside is now limited.

For example, a December 2015 call at the 210 strike would bring in about $4.50, covering a quarter of the cost of the zero-deductible 190 puts, bringing their net cost down to $13.50, or about a 4.2% annual rate. The real cost, though, is the opportunity cost. If SPY increases beyond 210, we do not participate. We have limited ourselves to, at most, a $21 gross gain (210 – 189). After subtracting our net insurance cost of $13.50, our maximum net gain would be $7.50. Calls at higher strikes would reduce cost less, but provide more upside headroom.

We could improve the performance of the collar by diagonalizing it – buying the puts now, and then selling individual one-month calls each month. Each month’s call strike could be determined by chart technical indications at that time. Ideally, we would keep the call strike just out of reach each month, and end up with both the stock and some call premium in our pocket.

3. Substitute bullish vertical spreads for the collars, reserving the excess cash.

You may have worked out that the collar strategy is just a variation on a bull call spread. The collar uses puts to limit downside risk, and also has limited upside because of the short calls. This is exactly what a bull call spread does. In the first collar example above, we own the SPY and also puts at the 190 strike, at a total cost of 189 + 18 = 207. We are short the 210 calls, allowing for a $3 maximum profit.

We could substitute the 189 December 2015 calls for the SPY stock and puts. The calls give the same risk profile as the protected stock: unlimited upside and limited downside. The difference is that the protected stock costs $207 per share, while the 190 calls cost $12.50. (There are other differences, too – the protected stock will still be there when the put options expire. The calls will not. The protected stock will also pay dividends).

With the bull call spread using long December 2015 190–strike calls at $12.50 and short December 2015 210-strike calls at $4.50, we risk a net of $12.50-4.50 = $8.00. Our maximum profit is the $20 difference between the strikes (210 – 190), less the $8.00 cost of the spread, or $12.00. This is a better profit at lesser cost than the collar. It would also allow us to take most of our money off the table now, using just a fraction of it to buy the spreads ($8.00 per share in place of $189 for the unprotected stock).

Which brings us full circle to:

4. Convert most of a portfolio to cash. Use a small percentage to buy long-term call options to maintain exposure.

We could simply sell here to preserve our profits, converting our stock positions to cash. We could then use a fraction of the proceeds to buy call options to regain our upside potential. In fact this option is really very similar to option 1 (keep the stock and buy puts), but with most of our cash in our pockets. We have limited downside (the cost of the calls), and unlimited upside. The main difference is that our calls will expire, while the stock will not. In times of “normal” interest income from cash holdings, this is a very attractive strategy.

Which of these is best? As is often the case, there is no way to know ahead of time. The more conservative your stance, the less profit potential you have. Each one of these would turn out to be the perfect strategy with a particular market – we just don’t know which market we’ll have.

This has been an introduction to basic profit preservation strategies. In future articles we’ll explore them more deeply.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.