Options Income Generators – Part 2

|In last week’s article, which you can read here, I discussed relatively conservative income generating strategies. One of my examples was the credit vertical spread. Today we’ll look at a way to simulate that strategy in cases where we are not permitted to do credit spreads.

First, credit vertical spreads are positions that involve selling an out-of-the-money option in hopes of its expiring worthless; together with the purchase of an even further out-of-the-money option as protection. The long option covers the short option, limiting its risk. If both options are behind the “firewall” of a strong demand or supply level, both options are expected to remain out of the money until expiration.

OK. Why might we not be permitted to use credit spreads? The answer is that brokers have a hierarchy of “approval levels” for option trading. The higher the risk, the more stringent the requirement. Brokers set their own rules for who will be allowed to use each type of strategy. Note that it is not really the risk to you, the customer that is the issue. It’s the risk to the broker. If a strategy could possibly result in any loss to the broker, a higher level is required.

Here are a typical set of approval levels. Each level up the chain requires more money in the account and/or more years of experience than the previous one:

Level 1

Sell covered calls against a stock position

Buy protective puts on a stock position

Level 2

Buy puts or calls “speculatively” (without owning the stock).

Sell cash-secured short puts (without owning the stock, but with 100% of the money in the account that would be needed to buy the stock)

Level 3

Debit spreads (buy a more expensive option that covers a less expensive short option)

Level 4

Credit spreads (buy a less expensive option that covers a more expensive short option)

Sell short puts “naked” (with less than 100% of the cash required to buy the stock)

Level 5

Sell short calls “naked” (without owning the stock)

Notice that credit spreads are at level 4, while debit spreads require only level 3. Since level 4 is significantly harder to get than level 3, many people are able to use debit spreads but not credit spreads.

If this is the case, we can substitute a debit vertical spread for any credit vertical spread.

Here’s an example:

On February 20, Incyte Corp (INCY), at $63.92, was in a long-standing uptrend. It had recently pulled back to a long-term trendline, which had so far held (see chart below). There was good support in the area around $58.00.

{kind=link}

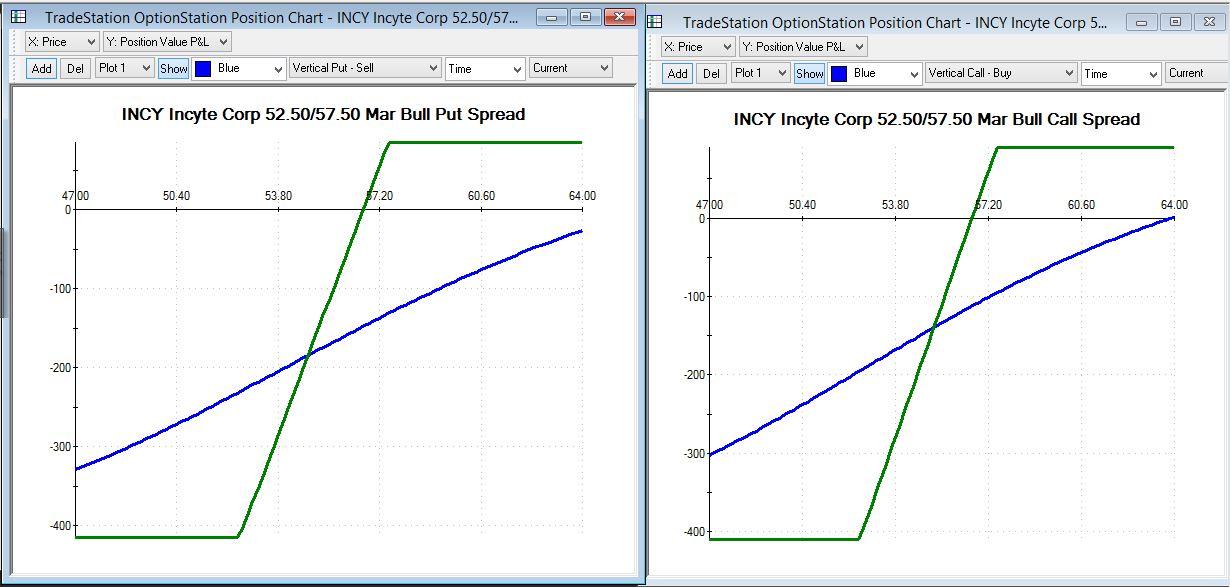

First, let’s look at the possibility of a credit spread – a Bull Put Spread. It looked like a good bet to sell the March $57.50 puts (at $1.65). As long as INCY remained above that $57.50 level for 29 days, they would expire worthless, allowing us to keep the premium. We could simultaneously buy the $52.50 March puts for protection at $.80. The net credit was $1.65-.80 = $.85 per share ($85 per contract). This amount was our maximum profit. Our breakeven price was the $57.50 strike less the $.85 credit, or $56.65.

Maximum loss on the credit spread would occur with INCY below $52.50 at expiration. In that case we would need to pay the $5.00 difference between the two strike prices to get out of the spread. Subtracting our $.85 credit, our net loss would be $4.15 per share ($415 per contract). This maximum loss would be our margin requirement. With strong technical support well above $57.50, this looked like a good trade.

Now let’s look at the debit spread alternative. If we had approval to buy debit spreads (level 3), but not to sell credit spreads (level 4), we could still get nearly the same deal. All that was required was to use the calls at the same strikes, in place of the puts.

We could have bought the $52.50 calls for about $12.05, and sold the $57.50 calls for about $7.95. The net debit was $ 4.10 per share ($410 per contract). Since this was a debit spread, the $410 we paid for was our maximum loss and our required cash outlay. This maximum loss would occur at any price of INCY of $52.50 or less at expiration. In that case our spread would be worthless. Note that this was almost identical to the $415 margin requirement for the credit spread. Like the credit spread, our maximum profit would occur at expiration at any price above $57.50. In that event, both options would be in the money, and we could sell the spread for the $5.00 difference between the strike prices. Subtracting our $4.10 cost would leave a net profit of $.90 per share, or $90 per contract – almost exactly the same as the credit spread’s $85 profit. Either spread would work out to a profit of about 20% in one month, as long as INCY held above that $57.50 level.

Below are the profit graphs of both spreads. Note that the charts look almost the same. Max profit, max loss, and break-even are within a few cents of each other.

{kind=link}

This same idea can be used to convert any credit vertical spread into its debit equivalent, or vice versa. In this case, the profits were almost identical. In other cases, one version may offer slightly more profit than the other, depending on volatility differences between the puts and the calls.

This shows another example of the versatility of options. Not only do we have many choices of strategies, but there is always more than one way to use any one of those choices.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.