Common Mistakes with Investments: Retirement Fund Allocation

|Last week we talked about the “Common Mistakes with your investment: Losses.†We covered how some of the common investing strategy mantras like “buy and hold†haven’t worked over the last decade and a half with the S&P 500 index averaging a meager 2% annual return. We also discussed how you can utilize the strategies employed by Wall Street professionals themselves. Strategies like leveraging predictable monthly income payments which can then be utilized to enter directional positions in the stock market. This week, I’ll focus on keeping more of what you make and show you how easily you can put thousands of dollars in your pocket that you’re likely not doing now.

How many times have you heard the following from Wall Street, the financial media, your CPA or your financial advisor, “Max out your 401(k).†Almost every day there is another article on how and why you should “Max out your 401(k).â€

The marketing powerhouses behind Wall Street program tells us to contribute as much money as we can to our 401(k)s. But why? Is this really the best way to save for your retirement? Who really benefits, you or banks and financial institutions?

There are two primary benefits to contributing to your 401(k):

Tax deferred growth – your 401(k) contributions are tax deductible and grow tax deferred. However, when you need the money the most during retirement, your withdrawals are 100% taxed.

Your employer provides a match on your contributions – typically a company matches your contributions up to a certain amount or percentage. This is a big benefit because it’s free money and there aren’t too many places where you can find free money.

Most people understand these benefits upfront but don’t really think about the consequences of over contributing until they’re retired and it’s too late. To illustrate, let’s run through an example.

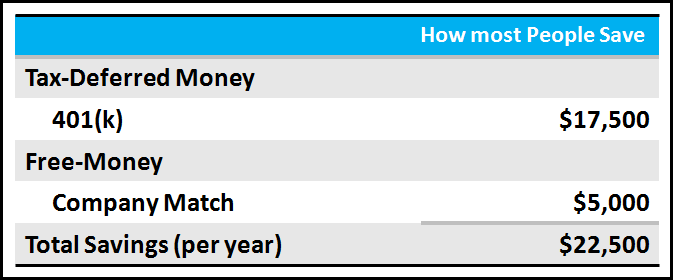

How Most People Save for Retirement:

Say you’re age 40, plan to retire at age 65 and you intend to max out your 401(k) contributions for 25 years. That maximum per year is $17, 500. In addition, you will receive a $5,000 company match. So your total savings for the year will be $22,500, as illustrated below.

{kind=link}

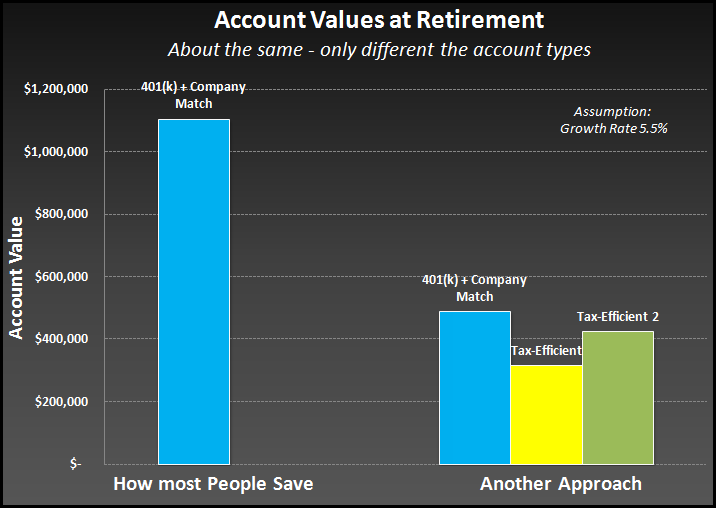

Assuming a modest 5.5% growth rate, over the 25 years your 401(k) account value will grow to roughly $1.1 million. That’s the good part. The challenge, what most people don’t realize is this money has been growing tax deferred, but when it comes time to withdraw, both your contributions and your gains will be taxed and taxed hard.

In our Financial Matters program, we teach students a concept called Power Ranking your Money and I want to share this with you here. The four different types of money, ranked best to least best, are:

free money – a 401(k) company match is considered free money

tax-free money – money you can access without paying taxes (i.e. Roth IRA)

tax-deferred money – traditional monies from a 401(k) or IRA, where you get the upfront tax deduction, tax-deferred growth and pay taxes when you withdraw

lastly, taxable money – every other kind of money falls in the taxable money category… we want to avoid this as much as possible. There is no tax advantage now or in the future.

Smart Saving for Retirement:

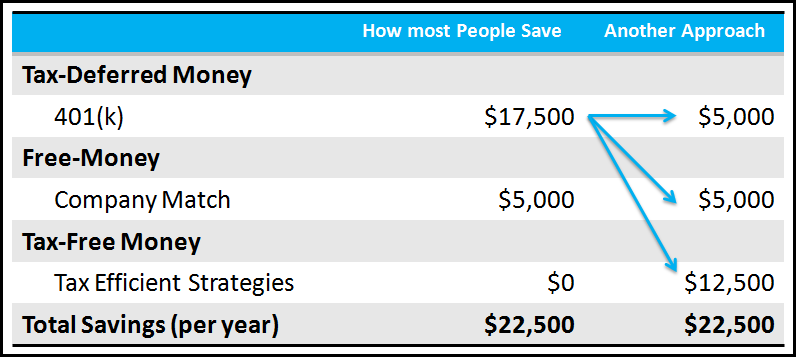

To show you why it’s so important to apply the “power-ranking-your-money†concept, let me illustrate what happens with these same numbers using “Another Approach†(this concept is what we teach our students). Let’s say an investor wants to save the same $22,500 a year. We know the company match is $5,000/year and so we’re only going to put that amount into the company 401(k); we want to take the free money. But, the remaining $12,500 will be saved utilizing another tax efficient strategy you may not be aware of. Basically, you’re still saving $22,500 per year but the money is allocated differently.

{kind=link}

Still assuming the same 5.5% growth rate, over the 25 years your account value will grow to roughly the same $1.1 million. However, the money is power-ranked differently. Look at the chart:

{kind=link}

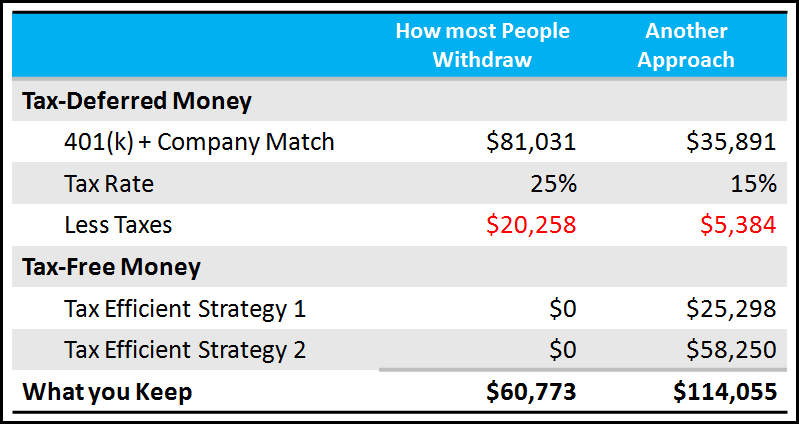

Now, here is why “max out your 401(k)†is a bad idea. Let’s fast forward to retirement. Let’s say you want to withdraw the same amount every year for 20 years until the funds are depleted.

What you keep:

To illustrate this, look at the chart below. With the traditional approach (what most people do) you take out $81,031 each year from Tax-Deferred Money (401k + company match). Don’t forget you need to now pay taxes on this money… at a tax rate of 25% you’ll pay $20,258 in taxes and so you end up keeping $60,773.

With the Alternative Approach you’re going to take out $35,891 from your tax-deferred account. Since you’re taking out less money you get the benefit of a lower tax bracket and only pay 15% in taxes or $5,384. Now, here is where the real advantage comes in… Remember those other accounts you saved in over the 25 years? Those funds were growing in tax-free accounts. Now, at retirement you withdraw $28,298 and $58,250 from two different types of tax-free money accounts and pay zero taxes on that money (if designed properly). If you add those numbers up you’re actually keeping $114,055.

That’s a difference of over $53,000 that you’ll be putting in your pocket every year. And remember, you’re withdrawing for 20 years and over that 20 year period you’ll be putting in your pocket over $1.0 million.

{kind=link}

You could argue, take the tax savings and invest it. We have actually run those numbers and you get a little more benefit but it still does not compare. What we’ve also discovered is that most folks don’t invest the tax savings and end up spending it.

While the example above is very simplified, the main point is to think about the max and understand that there is another strategy that may be a much better option for you. So why doesn’t Wall Street teach you about these concepts? Here’s a hint… mutual funds. What types of investment vehicles are mostly found in 401(k)s? That’s right, mutual funds. And what do most mutual funds have in common? We’ll if you’ve been reading my recent articles you know by now its fees, and most are not cheap. Who benefits from these fees charged in your 401(k) mutual fund? Right again, Wall Street Banks and Financial Institutions.

Are the banks and institutions doing anything wrong? I would argue “no.†They simply use smart strategies to attain profits and are very smart with their money and the vehicles they save in. You should not be thinking, “How can I beat Wall Street?†Instead, learn to think and act like Wall Street. Utilize strategies that put more money in your accounts, not the accounts of banks and financial institutions.

Hope this was helpful, have a great day.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.