Who Are the Option Market Makers?

|The listed options market in its current form exists because some people are willing to make a business of being option dealers. The job of each option dealer, or market maker, is to make a two-sided market in the options of certain stocks. Making a two-sided market means that at all times the firm is willing both to buy and to sell those options. Their computer systems continuously feed their quotes – the prices at which they are willing to buy and to sell – to the options exchanges where they operate. The market makers’ profit comes from the difference between the prices at which they buy and those at which they sell.

At one time, being an option market maker was something that could be done profitably on a pretty small scale by an individual trader using his own capital. In recent years, though this has changed so that now only bigger firms can afford the required technology. Large banks and brokerages like Goldman Sachs, JP Morgan, Barclays Bank and so on are the kinds of companies that make up the majority in this business today.

When we want to know what options are available for a particular stock or exchange-traded fund, we consult the option chain for that stock. The information for the chain is provided by a central agency called the Options Price Reporting Authority. OPRA’s computers receive the information from all market makers, other traders and option exchange, consolidate it and feed it back out again. Here is OPRA’s own explanation, from their website:

“All of the transactions executed on, and price quotations for options generated by, each options exchange are communicated to the public by OPRA… Each trade that is executed on an options exchange, as well as each price change quoted on an options exchange, is reported to OPRA as a ‘message.’ … The messages are sent to OPRA and distributed to market data vendors on a consolidated basis for use by options market participants, including retail investors, broker-dealers, and the exchanges themselves.”

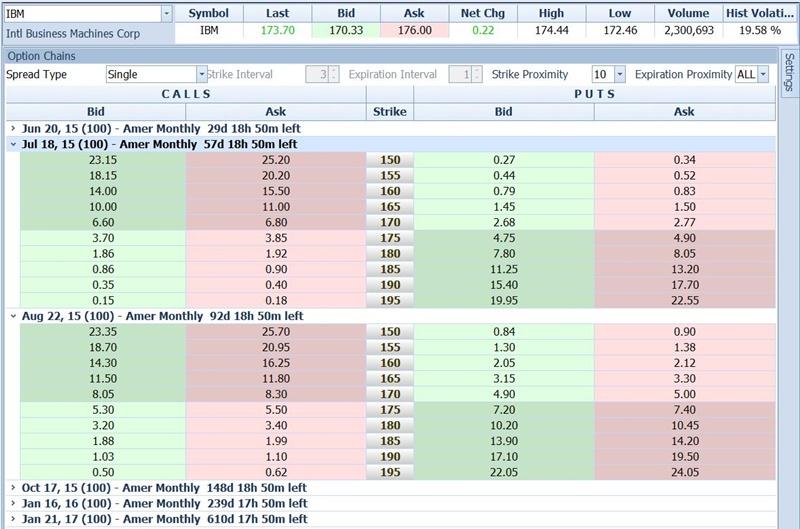

We can get access to OPRA’s data through our option broker or in delayed form online through various web sites. Here is an option chain from one broker (Tradestation) in its most minimal form:

{kind=link}

This option chain lists some of the available put and call options for the stock of IBM.

Down the middle of the screen, the “Strike” column lists different option strike prices. At each strike price (each row in the table) information for the Call (option to buy IBM) is listed on the left and information for the Put (option to sell IBM) is listed on the right.

For each individual Call or Put option, the Bid column shows the level of the highest limit order to buy that exists at that time for that option (consolidated from worldwide data by OPRA). In the first set of options above, July 2015 for example, the number in the green column under “Bid” for the Call at the Strike of 170 is $6.60. This means that in the whole world at that moment, the highest price at which anyone had committed to buy that option was $6.60. This quote might be from one of the market makers for IBM options. It might also be from some other institutional trader or even a retail trader like us.

The “Ask” column shows the lowest price at which any trader anywhere has committed to sell the option. For our July 170 call, the Ask is $6.80. Again, this quote might be from anyone, including possibly (but not necessarily) the same market maker who is simultaneously bidding $6.60.

The market maker’s profit comes from buying at the Bid price and selling at the Ask price. Our July 170 call provides a $.20 profit margin ($6.60 vs $6.80).

Notice that we see a fully populated matrix here, with no holes. Every option has both a Bid and an Ask price. This is true whether there have been any actual trades on a particular option or not. The reason for a complete and fully populated chain at all times is that the market makers are always quoting every option whether anyone else is or not. They literally make the market.

If many other people aside from the market makers are also interested in buying and selling a company’s options, they of course will be placing their own orders. If they want to buy at a price that is a touch higher than the Bid price shown, they are free to place a limit order to buy accordingly. If we wanted to buy some of those July calls for example, there is nothing stopping us from placing a limit order to buy at $6.65, $.05 more than the current $6.60 bid. We then become the best bid, rather than the market maker. We are in line in front of the market maker, and he will get less business. If he wants to get more he will have to raise his bid. This will narrow his spread. The same thing is true in reverse for Ask prices. If the market makers are quoting a high price others are free to offer to sell at lower prices. Again the market makers will have to narrow their spreads to compete.

In stocks where many thousands of traders participate, the bid-ask spread can narrow to as little as a penny. This is the case, for example, on options of heavily traded index exchange-traded funds like QQQ (NASDAQ 100 index fund) or SPY (S&P 500 index fund).

As a general rule, the narrower the spreads on options are the better it is for the retail traders like us. That spread is the markup between wholesale and retail. Friends don’t let friends pay retail. In our Professional Options Trader class we teach our traders always to look for narrow spreads and to give options with wide bid-ask spreads a pass. I suggest that you also follow this example.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.