Common Mistakes with 401(k) Accounts: 401(k) Fees

|When it comes to managing your 401(k), most people making three major mistakes that cost them thousands of dollars; and the scary part is they likely don’t even know it. This is article is the first in a three part series on retirement planning and your 401k. The three biggest mistakes that cost people thousands are related to:

Fees

Taxes

Losses

Fees

Most individuals that have a 401(k) plan aren’t aware of how much they’re actually paying in fees. To illustrate this common lack of awareness let me tell you what happened when we met with a Chief Financial Offer at a company several weeks back. He was shocked when we told him that he was paying Wall Street 5.75% on every dollar he was contributing to the company’s 401(k). If an expert in the field of finance who is a CFO is not aware of the hidden fees, how could the average investor know?

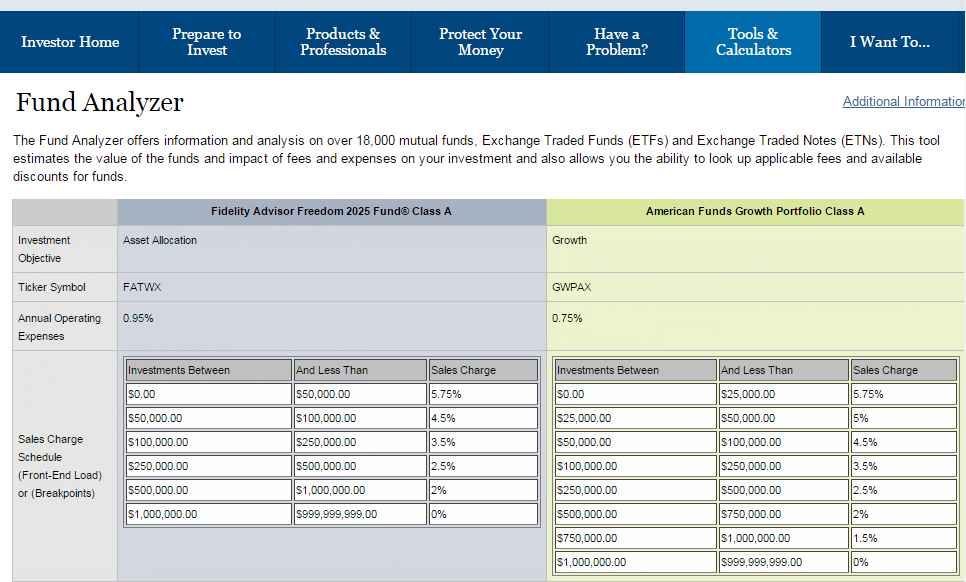

Let’s begin to focus on what you may be doing wrong and how to fix it. It’s important to understand how much you are actually paying in 401(k) fees because it will dramatically impact your investment returns over time. Annual operating expenses, sales charge and investment manager fees are key fees you need to be aware of. To illustrate the fee structures that are embedded with hidden costs let’s look at the screen shot below. What you’re looking at is a screen shot from the FINRA (Financial Industry Regulatory Authority) website. I’ve picked out two very popular mutual funds to make my point. On the left is the Fidelity Advisor Freedom 2025 Fund (a 2025 target date fund) and the second, on the right, is American Funds Growth Portfolio.

What you’ll notice are two expense areas that we should pay particular attention to. The first is the annual operating expenses; this is the operating expenses of the mutual fund itself. You’ll notice that the Fidelity Fund has an annual operating expense of 0.95% and the American Funds annual operating expense is 0.75%. Additionally, you’ll notice the front end loaded sales charge schedule, which is what most people are NOT familiar with. Take note that every dollar you contribute to these 401(k)s has sales charge (some call it a commission) of 5.75%. This is true for both the Fidelity and American Funds below. There may be situations where your company may have negotiated a lower fee structure with the mutual fund companies.

{kind=link}

Additionally, what you won’t find in the screen shot are portfolio managers cost (or management fees). Typically these fees range between 0.25% and for smaller plans you may be charged an additional 1.5%. These fees are also known as investment advisory fees (or I like to refer to them as Wall Street’s pension plan). For example, for every dollar that you contribute to your 401(k) the fee can cost you anywhere from 6.5% to 8.0%. So, if the stock market has a good year and goes up 8% on the year, for that year you basically break even.

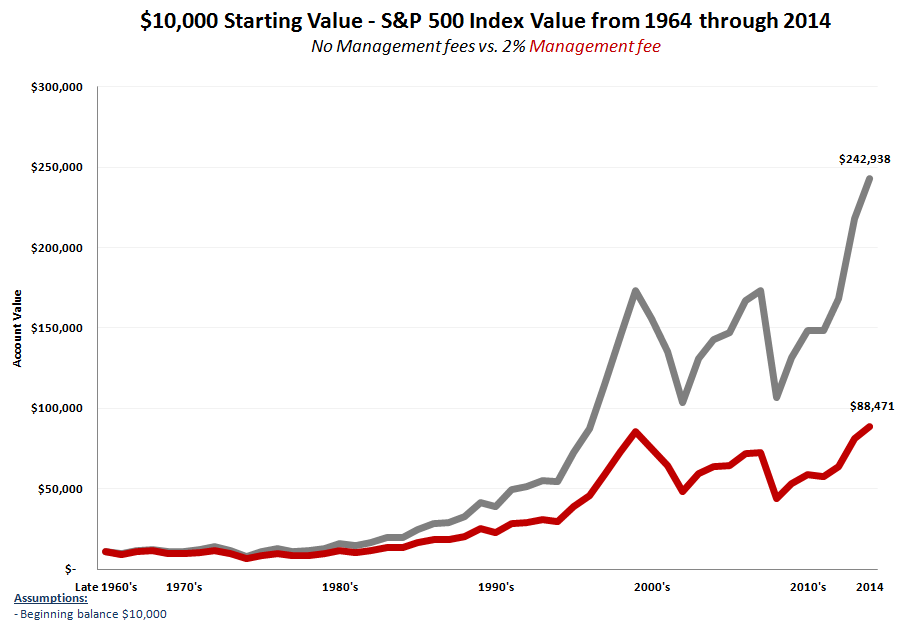

That’s why it’s important for you to be aware of all these different fees within your 401(k). The fees will reduce your overall performance and the amount of money you’ll have available to you when you need it the most, during your retirement years. Let me illustrate by using the chart below.

Below is a screen shot of the S&P 500 index value for the past 50 years, from 1964 through 2014. The beginning value of this hypothetical example is $10,000. The grey line represents the growth of that $10,000 over the 50 years with no management fees. That total is $242,938. The red line, however, is what most people experience with the growth of $10,000 in a typical 401(k). Please note that this red line has a 2% management fee and its value over 50 years is $88,471. The difference in account value between the two is approximately $150,000. This begs the question. “Where did the $150,000 go?” Hint, that’s the banks money – the pension you’re helping build for Wall Street. Think about it, you’re providing 100% of the money, taking 100% of the risk and only receiving 35% of the profits.

{kind=link}

Here’s how you can reduce some or all of your 401(k) fees and keep more of what you make. First, check within your existing 401(k) on your investment options and find funds with the lowest expense ratio by using the “Fund Analyzer”. Look for the lowest expense ratio funds and reallocate your positions to those funds. Typically look for funds with no front end load fees and expense ratios below 0.50%.

If your 401(k) does not offer funds with low expense ratios then you may want to consider transferring your existing balance (the balance that is vested) into your own IRA. Once you have your IRA established you’ll be able to choose from a variety of low cost funds and ETF’s. As I have mentioned so many times over the years, there is a major gap in profits between Wall Street and the average investor. The more you understand how the financial system really works, the more empowered you will be to make financial decisions that benefit you, not Wall Street.

We’ll discuss taxes and losses in the next two articles. Hope this was helpful, have a great day.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.