It may be a quiet week in financial markets, with no central bank meetings or any other major events on the agenda, as the summer lull finally kicks in. Economic data will therefore attract most of the attention, though any tweets on the trade war or Brexit news could always stir things up.

British data unlikely to be a game-changer for the pummeled pound

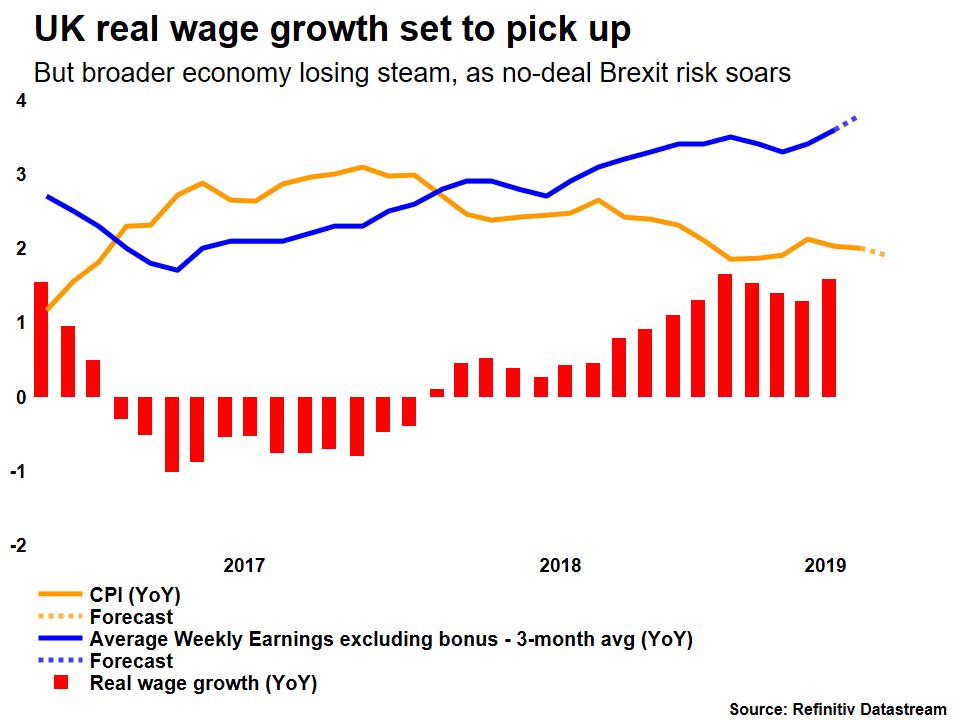

The UK economy continues to feel the heat, with GDP growth contracting in Q2, as Brexit fears keep holding back business investment. The nation will see a barrage of data releases next week – with employment data for June hitting the markets on Tuesday, inflation figures for July on Wednesday, and retail sales stats on Thursday – but as usual the pound will be driven mainly by politics.

On that front, Boris Johnson has been playing a game of ‘chicken’ with the EU lately, threatening a no-deal Brexit in October to extract concessions. The EU, meanwhile, has been adamant that it won’t renegotiate the most important aspect of the deal – the Irish border. Neither side is likely to blink anytime soon, implying that there’s almost no scope for any breakthrough before October.

In this sense, the outlook for the pound remains negative overall, with the only saving grace for the currency being a potential General Election that raises hopes for another referendum. Alas, any such rebound may be at least one month away, given that a no-confidence vote in the government cannot be called until September 3, when the UK Parliament returns from summer recess.

US inflation & retail sales the next pieces of the (easing) puzzle for Fed

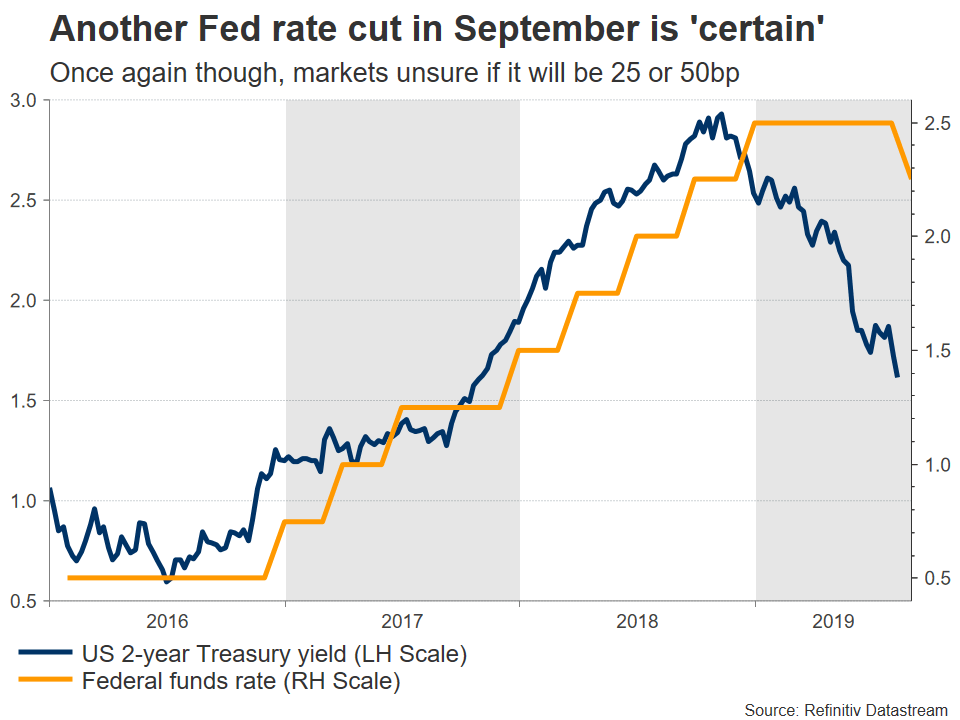

Across the Atlantic Ocean, investors will keep an eye on America’s latest CPI inflation data on Tuesday and retail sales stats on Thursday, for clues on how aggressively the Fed will cut rates in September. While the US economy remains in decent shape overall, market expectations for another cut in September skyrocketed lately following the latest escalation in the trade war.

Much like the story before the Fed’s July meeting, a typical 25 basis points (bp) rate cut is now fully priced in for September, with markets also assigning a ~35% probability for a more aggressive 50bp cut. Hence, investors believe that another move in September is a done deal, with the real question being how much the Fed will cut.

Overall, while more action is virtually certain, markets may have gotten ahead of themselves by pricing in so much easing so quickly, at least judging by recent comments from Fed officials. Even James Bullard – arguably the most dovish policymaker – recently appeared hesitant to commit to more cuts, indicating that the Fed can be patient for now and monitor the effects of its latest actions.

The point is that if Bullard is cautious about cutting again so soon, there’s probably zero appetite for an aggressive 50bp move in September among the rest of the Committee. Therefore, the near-term risks surrounding the dollar seem tilted to the upside, as the various officials may try to push back against the market’s overly dovish expectations in the coming weeks.

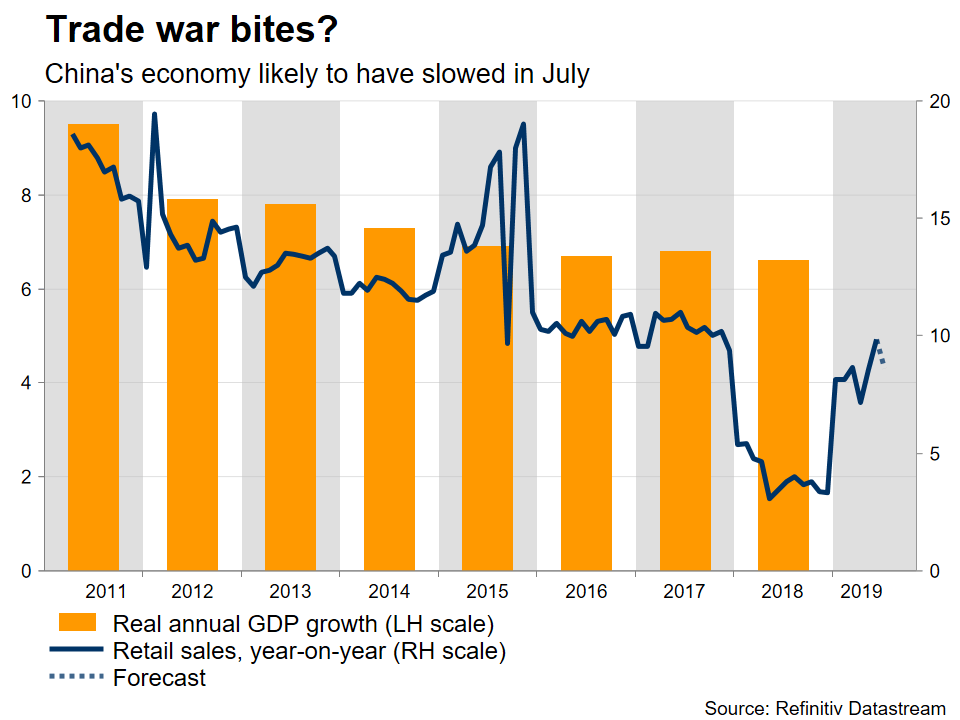

China’s monthly data dump eyed, as trade war intensifies

Meanwhile on Wednesday, the world’s second-largest economy publishes retail sales, industrial production, and fixed asset investment figures, all for July. Forecasts point to a slowdown in most of these indicators, which if confirmed, may be seen as a sign that the trade war has really started to inflict damage – despite sizeable stimulus measures.

In the markets, besides the yuan and the China-sensitive aussie, these data could also impact broader risk sentiment if they paint a darkening picture for the world’s growth engine. Perhaps more important for risk appetite though will be what happens in the trade saga, where the prospect of real progress looks highly unlikely given the recent tensions. In fact, Trump may even use this conflict to fire up his electoral base and score some political points as he hits the campaign trail, so another round of tariffs could be on the cards next month, keeping risk aversion in play.

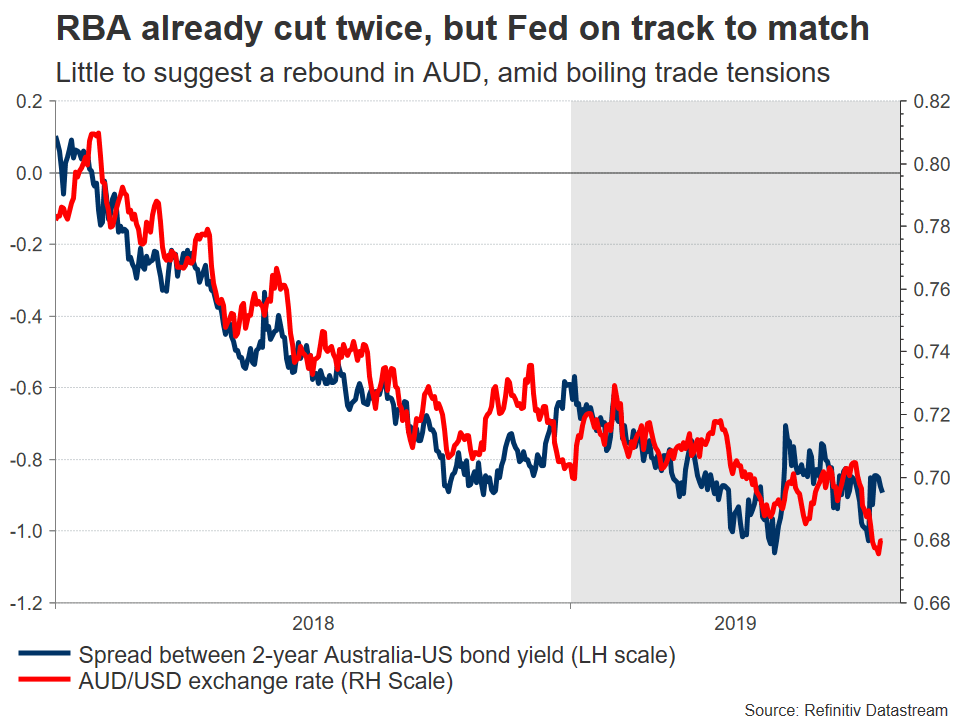

Australia’s employment data to decide timing of next RBA move

It will be a busy week in the ‘Land Down Under’ too, where wage growth stats for Q2 are due early on Wednesday, before the employment numbers for July hit the wires on Thursday. Wages are expected to have risen at the same pace, the unemployment rate is forecast to have held steady, while the net change in employment is expected to have increased – a positive sign.

The Reserve Bank of Australia (RBA), which cut interest rates at two of its last three meetings, made it clear that labour market developments will be the main factor influencing whether and how quickly it cuts rates again. Market pricing suggests a ~40% chance for another cut in September and if these data are indeed encouraging, that percentage could drop, helping the battered aussie to recover some of its losses.

That said, the broader picture for the currency still looks bleak. Even if the RBA doesn’t cut in September specifically, it will most probably cut again before year-end, perhaps even twice. Meanwhile, trade risks may continue to haunt the currency, given Australia’s export-heavy economy.

Europe will keep an eye on Italian politics

In the Eurozone, Germany’s ZEW survey for August is due on Tuesday, before the nation’s GDP data for Q2 are published on Wednesday. Growth figures for the entire euro area will also be released on the same day.

As for the euro, it may take its cue mainly from political developments, given the prospect of snap elections in Italy.

Forex trading and trading in other leveraged products involves a significant level of risk and is not suitable for all investors.

Recommended Content

Editors’ Picks

EUR/USD consolidates gains below 1.0700 amid upbeat mood

EUR/USD is consolidating its recovery below 1.0700 in the European session on Thursday. The US Dollar holds its corrective decline amid improving market mood, despite looming Middle East geopolitical risks. Speeches from ECB and Fed officials remain on tap.

GBP/USD clings to moderate gains above 1.2450 on US Dollar weakness

GBP/USD is clinging to recovery gains above 1.2450 in European trading on Thursday. The pair stays supported by a sustained US Dollar weakness alongside the US Treasury bond yields. Risk appetite also underpins the higher-yielding currency pair. ahead of mid-tier US data and Fedspeak.

Gold price shines amid fears of fresh escalation in Middle East tensions

Gold price rebounds to $2,380 in Thursday’s European session after posting losses on Wednesday. The precious metal holds gains amid fears that Middle East tensions could worsen and spread beyond Gaza if Israel responds brutally to Iran.

Ripple faces significant correction as former SEC litigator says lawsuit could make it to Supreme Court

Ripple (XRP) price hovers below the key $0.50 level on Thursday after failing at another attempt to break and close above the resistance for the fourth day in a row.

Have we seen the extent of the Fed rate repricing?

Markets have been mostly consolidating recent moves into Thursday. We’ve seen some profit taking on Dollar longs and renewed demand for US equities into the dip. Whether or not this holds up is a completely different story.