Global equities are well supported for a third consecutive session as the U.S and China have found some common ground on trade.

Note: Both countries agreed to extend trade talks in Beijing for an unscheduled third-day.

Despite both negotiating teams being unable to reach an all-encompassing trade deal over the past 48-hours, the world’s two largest economies appear to have progressed towards bridging the hostile divide that has been able to unsettle capital markets over the past 12-months.

These positive signs have given investors the confidence to own risk once again, and has led the U.S dollar to dip against G10 currency pairs and Treasury yields to back up a tad before this afternoons release of the Fed’s December minutes (02:00 pm EDT).

The minutes are unlikely to have much impact on the ‘big’ dollar, given Fed chair Powell’s comments last week, where he indicated that U.S policy makers are prepared to shift the stance of its policy “significantly” if necessary.

On tap: Bank of Canada (BoC) monetary policy meeting (10:00 am EDT) – Governor Poloz is expected to hold rates steady (+1.75%), though pricing in the Overnight Index Swaps (OIS) market suggests there is a +17% possibility that the bank could reverse its most recent hike.

1. Stocks are a delight

With the U.S and China finding some common ground in their trade talks has made owning stocks more appealing.

In Japan, equities rallied for a third-day as signs of progress in Sino-U.S trade talks improved confidence, offsetting weakness in chip-related stocks. Both the Nikkei and the broader Topix advanced +1.1%.

Down-under, Aussie stocks rallied to a two-month high on trade optimism. The S&P/ASX 200 index closed up +1%, building on Tuesday’s gain of +0.7%. In S. Korea, the Kospi index posted its biggest daily percentage gain in two-months, closing +1.95% higher.

In China, these positive trade talks helped push the blue-chip CSI300 index up +1.0% and the Shanghai Composite Index up +0.7%. In Hong Kong, at the close of trade, the Hang Seng index was up +2.3%, while the Hang Seng China Enterprises index jumped +2.2%.

In Europe, with risk being well supported, regional bourses are trading higher – the DAX and the French CAC are the most notable.

U.S stocks are set to open in the ‘black’ (+0.35%).

Indices: Stoxx600 +0.76% at 348.50, FTSE +0.77% at 6,914.25, DAX +0.91% at 10,901.79, CAC-40 +1.09% at 4,825.08, IBEX-35 +0.15% at 8,861.15, FTSE MIB +1.14% at 19,220.50, SMI +0.36% 8,652.50, S&P 500 Futures +0.35%.

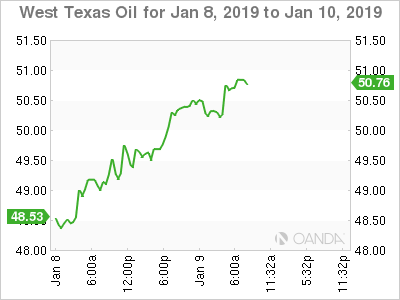

2. Oil rises over +1% on Sino-U.S trade talks, gold lower

Oil prices have extended their gains from Tuesday’s session on hopes that Washington and Beijing may soon resolve their trade disputes.

Brent crude futures are up +69c, or +1.2%, while U.S West Texas Intermediate (WTI) oil futures are at +$50.42 per barrel, up +64c, or +1.3% from yesterday’s close.

Note: Both benchmarks gained +2% in yesterday’s session.

Aside from global trade optimism, crude oil prices have been receiving support from supply cuts that started at the end of last year by OPEC+.

Theses cuts are intended to rein in a supply overhang, caused mostly by U.S crude oil output – EIA data shows U.S output surged by around +2M bpd in 2018, to a record +11.7M bpd.

Dealers are expected to take their cue from today’s official U.S fuel storage data from the EIA (10:30 am EDT).

Ahead of the U.S open, gold prices have edged lower on stronger risk sentiment. Spot gold is down -0.3% at +$1,282.75 per ounce, while U.S gold futures are -0.2% lower at +$1,283.8 per ounce.

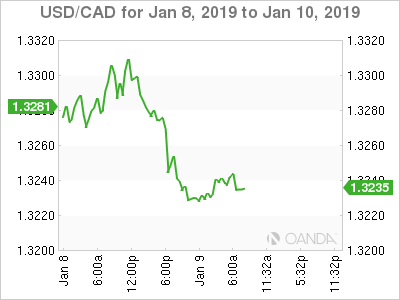

3. Bank of Canada (BoC) rate decision in focus

CAD’s OIS curve (overnight index swap) currently paints a ‘dovish’ view of Canadian interest rates (+1.75%). Nevertheless, there are a few dealers who do not prescribe to a ‘no-rate’ change decision by the BoC later this morning; in fact, they are looking for +25 bps hike.

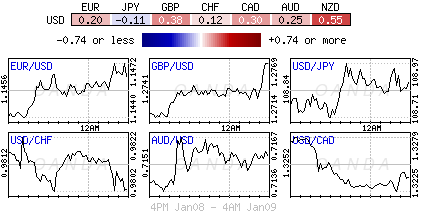

Even without pricing in a hike today, the CAD (C$1.3240) remains the best-performing G10 currency over the past week – the loonie has found support from higher oil prices and a positive surprise from Canadian PMI data. If Governor Poloz gets the urge to tighten matters, USD/CAD could see itself take on C$1.3080 rather quickly.

Elsewhere, the Fed releases the minutes of its Dec. 18-19 meeting this afternoon (2 pm EST). It should provide more details about how policy makers viewed the risks to economic growth when they raised interest rates during a period of heightened market volatility.

They voted unanimously to hike fed-funds to a range between +2.25% and +2.5% at the meeting, their fourth increase of the year. They also made a significant change to their policy forecast by projecting two rate increases in 2019, down from the three they anticipated in September, despite modest changes to their growth expectations.

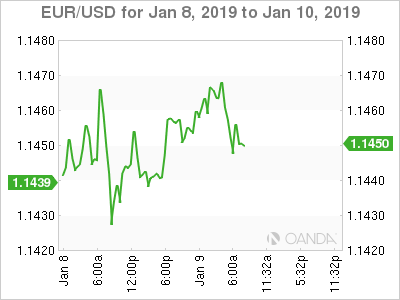

4. EUR trapped in a range

For now, EUR/USD (€1.1450) is trapped within a range as weak German and eurozone economic data will not allow the ‘single’ currency to rally and close above €1.15 despite the ‘big’ dollar weakness. However, if the Sino-US trade talks do happen to show some concrete progress, then the EUR bulls should expect that key resistance of €1.15 to give way rather quickly.

GBP/USD is higher by +0.2% at £1.2735 area as PM May seeks EU assurances on the backstop provision. Last night, the UK government lost a vote on funding a “no-deal” Brexit – this certainly complicates matters for PM May as Parliament tries to stop a “no-deal” Brexit.

Note: The U.K parliament is due to vote on the Brexit withdrawal bill on Jan 15, until then, the pound remains driven by any Brexit developments.

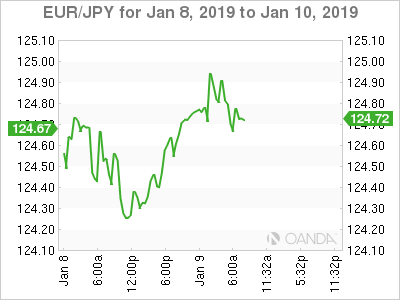

USD/JPY (¥108.90) is higher for a fourth consecutive session as investor risk appetite improves on speculation that U.S-China is making progress in their trade talks.

5. German trade balance

Data this morning showed that German exports declined in November, supporting market fears that trade tensions are impeding Germany’s economic upswing.

Exports from the eurozone’s largest economy fell -0.4% on the month to +€110.6B in November, while imports dropped -1.6% to +€91.6B from October. The adjusted trade surplus amounted to +€19.0B in November, surpassing a market forecast of +€18.0B.

Note: The German economy contracted in Q3 2018, for the first-time in three-years, knocked mostly by weaker exports.

The drop in exports coincides with other downbeat data released this week – German new manufacturing orders fell -1% on the month in November, more than the -0.4% decline that the street was expecting.

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities.

Opinions are the authors — not necessarily OANDA’s, its officers or directors. OANDA’s Terms of Use and Privacy Policy apply. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Recommended Content

Editors’ Picks

AUD/USD stands firm above 0.6500 with markets bracing for Aussie PPI, US inflation

The Aussie Dollar begins Friday’s Asian session on the right foot against the Greenback after posting gains of 0.33% on Thursday. The AUD/USD advance was sponsored by a United States report showing the economy is growing below estimates while inflation picked up. The pair traded at 0.6518.

EUR/USD mired near 1.0730 after choppy Thursday market session

EUR/USD whipsawed somewhat on Thursday, and the pair is heading into Friday's early session near 1.0730 after a back-and-forth session and complicated US data that vexed rate cut hopes.

Gold soars as US economic woes and inflation fears grip investors

Gold prices advanced modestly during Thursday’s North American session, gaining more than 0.5% following the release of crucial economic data from the United States. GDP figures for the first quarter of 2024 missed estimates, increasing speculation that the US Fed could lower borrowing costs.

Bitcoin price continues to get rejected from $65K resistance as SEC delays decision on spot BTC ETF options

Bitcoin (BTC) price has markets in disarray, provoking a broader market crash as it slumped to the $62,000 range on Thursday. Meanwhile, reverberations from spot BTC exchange-traded funds (ETFs) continue to influence the market.

US economy: Slower growth with stronger inflation

The dollar strengthened, and stocks fell after statistical data from the US. The focus was on the preliminary estimate of GDP for the first quarter. Annualised quarterly growth came in at just 1.6%, down from the 2.5% and 3.4% previously forecast.