- Initial claims forecast to fall to 1.8 million from 2.123 million.

- Continuing claims expected to drop to 20.05 million from 21.052.

- Almost41 million unemployment claims have been filed in 10 weeks.

- ADP payrolls decreases much less than predicted in May.

- Markets have clear signs the worst has passed.

- Dollar pandemic risk-premium eliminated from all major pairs.

The tempo of destruction wrought by the shutdown of the US economy has begun to abate as job losses decline and a few indicators point to improvement if not yet recovery.

Labor market statistics

Initial jobless claims are forecast to fall to 1.8 million in the May 29 week their lowest level since the viral crisis began almost three months ago.

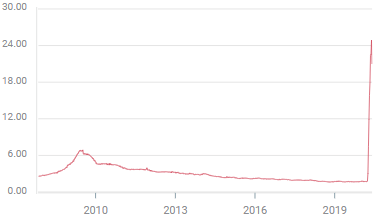

Continuing claims which unexpectedly plunged 3.86 million in the week of May 15 to 21.052 million are forecast to fall to 20.050 million.

Continuing claims

Private payrolls from ADP, the precursor to this Friday’s NFP report, fell 2.76 million in May, less than a third of the 9 million forecast and the April loss was revised down to 19.557 million from 20.236 million.

Business surveys from the Institute for Supply Management have lifted from their April lows. The manufacturing purchasing managers’ index registered 43.1 up from 41.5. The new orders index rose to 31.8 from 27.1 and the employment index edged to 32.1 from 27.5.

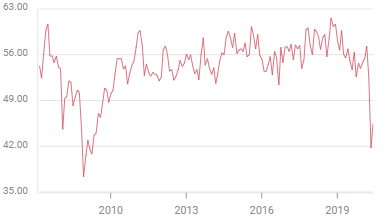

Services showed greater life with the overall PMI rising to 45.4 in May from 41.8, and new order jumping to 41.9 from 32.9. Employment inched to 31.8 from 30 in April.

Services PMI

FXStreet

FXStreet

Hiring is normally the last indicator to move in a recovery as firms like to be sure an improvement in conditions is underway before increasing payroll costs.

The fall in unemployment insurance filings and the sharp reverse in continuing claims suggest that the end of business restrictions in many states has returned some workers to their jobs. This movement can only intensify in the weeks ahead and will build on itself as reemployed workers regain income and deferred spending by the remaining 75% of the labor force revives consumer spending.

Conclusion: Market conditions

Equity and currency markets have priced in a sure and perhaps rapid return from the closures that have ravaged the US economy.

The Dow and S&P 500 were ahead 2.15% and 1.48% on Wednesday afternoon and are down just 7.89% and 3.2% respectively on the year. The dollar has surrendered all of its risk-aversion premium with all of the major pairs at or close to their pre-crisis levels.

Yields in the Treasury market have jumped with the 10-year up eight points to 0.757%, its highest level since late March and the 2-year higher by three points to 0.196% its best since May 2.

If the statistical forerunners of the past two weeks are accurate the trends in equities, bonds and the dollar will continue for the immediate future.

Markets have pondered the resumption of economic activity for weeks debating the letters of recovery, whether a V, L, W, U or some permutation would describe the trajectory.

It seems that that history may be our best guide after all. The bigger the drop, the higher the bounce. .

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

AUD/USD risks a deeper drop in the short term

AUD/USD rapidly left behind Wednesday’s decent advance and resumed its downward trend on the back of the intense buying pressure in the greenback, while mixed results from the domestic labour market report failed to lend support to AUD.

EUR/USD leaves the door open to a decline to 1.0600

A decent comeback in the Greenback lured sellers back into the market, motivating EUR/USD to give away the earlier advance to weekly tops around 1.0690 and shift its attention to a potential revisit of the 1.0600 neighbourhood instead.

Gold is closely monitoring geopolitics

Gold trades in positive territory above $2,380 on Thursday. Although the benchmark 10-year US Treasury bond yield holds steady following upbeat US data, XAU/USD continues to stretch higher on growing fears over a deepening conflict in the Middle East.

Bitcoin price shows strength as IMF attests to spread and intensity of BTC transactions ahead of halving

Bitcoin (BTC) price is borderline strong and weak with the brunt of the weakness being felt by altcoins. Regarding strength, it continues to close above the $60,000 threshold for seven weeks in a row.

Is the Biden administration trying to destroy the Dollar?

Confidence in Western financial markets has already been shaken enough by the 20% devaluation of the dollar over the last few years. But now the European Commission wants to hand Ukraine $300 billion seized from Russia.