![]() Monica Kingsley

Monica Kingsley

Monicakingsley

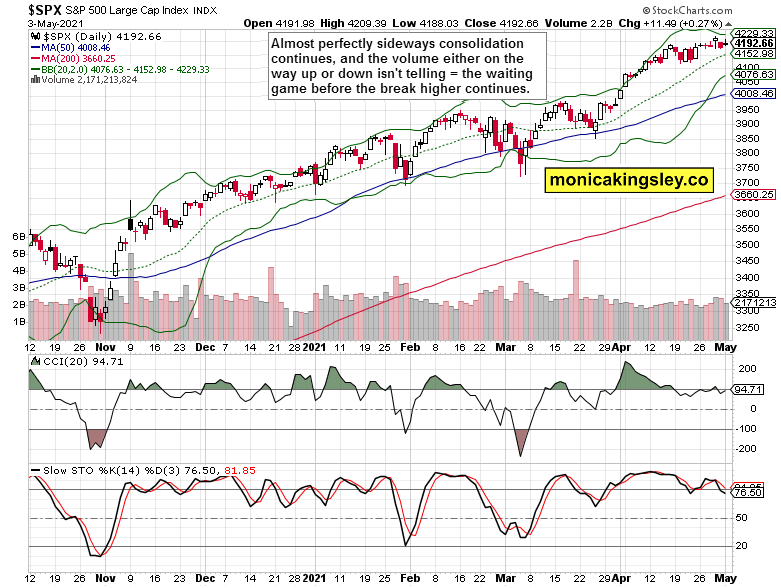

One more day of upside rejection in S&P 500, in what is now quite a long stretch of prices going mostly sideways. As unsteady as VIX seems at the moment, it doesn‘t flash danger of spiking in this data-light week, and neither does the put/call ratio. As I wrote yesterday about the selling pressure, these tight range days accompanied by 30-ish point corrections is as good as it gets when the Fed still has its foot on the accelerate pedal.

Yes, you can ignore the Kaplan trial baloon (have you checked when he gets to vote on the FOMC?) that spiked the dollar on Friday but didn‘t put all that a solid floor before long- dated Treasuries as seen in their intraday reversal.

Highlighting the key Treasury, inflation and reflation thoughts of yesterday, as these are still here to power stocks higher:

(…) the 10-year yield has been quite well behaved lately, closing at 1.65% only on Friday. The April calm seems to be over, and I‘m looking for the instrument to trade at 1.80% at least at the onset of summer. Then, let‘s see how the September price increases telegraphed by Procter & Gamble influence the offtake – will the price leader be followed by its competitors? That‘s one of the key pieces of the inflation stickiness puzzle – and I think others will follow, and P&G sales and profitability won‘t suffer. The company is on par with Coca Cola when it comes to dividends really.

Once there, we would progress further in the reflation cycle when inflation is no longer benign and anchored. We‘re though still quite a way from when the Fed tries to sell rising rates as proof of strengthening economic recovery – once the bond market would get to doubt this story though, it would be game over for its recent tame behavior.

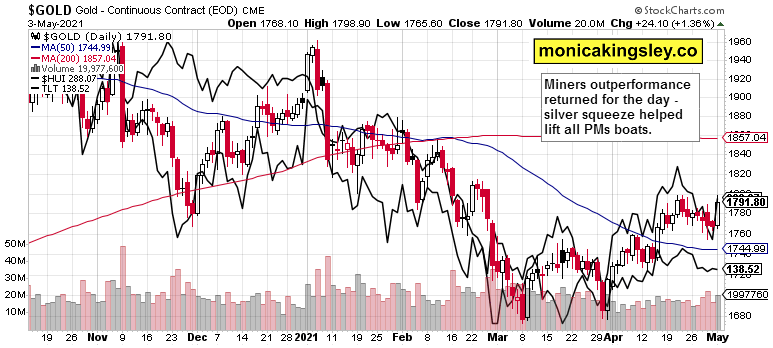

Gold market enjoyed its fireworks, aided mightily by the silver squeeze run. The inflation theme is getting rightfully increasing attention, and commodities are on the run across the board. Just check yesterday‘s oil analysis or the bullish copper calls of mine. I could just as easily say that copper is the new gold – it has been certainly acting as one over the past many months, yet the yellow metal‘s time in the limelight is about here now. And don‘t forget about silver bring you the best of two worlds – the monetary and industrial applications ones.

When it comes to USD/JPY support for the unfolding precious metals upswing, we indeed got the reversal of Friday‘s USD upside:

(…) The taper story being revealed for a trial baloon that it is, would quickly reverse Friday‘s sharp USDX gains, where particularly the USDJPY segment is worth watching.

Let‘s move right into the charts.

S&P 500 outlook

The declining volume tells a story of not enough conviction to go higher or lower – the market remains vulnerable to brief spikes either way such as those seen and covered in both today‘s intraday Stock Trading Signals.

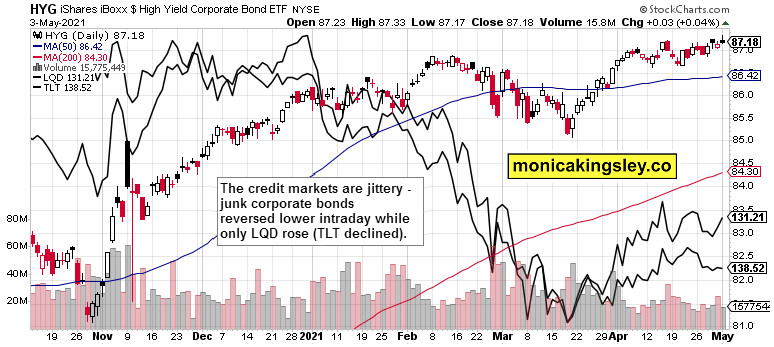

Credit markets

As inconclusive intraday the corporate credit markets may seem, the pressure to go up is there, regardless of the high yield corporate bonds reversal. Long-dated Treasuries aren‘t standing in the way but it must be noted that these have given up their intraday upswing completely, and opened with no bullish gap.

Technology and financials

Technology lost the advantage of higher open, and wasn‘t helped by the poor daily $NYFANG performance. At the same time, value stocks continued higher but gave away a portion of intraday gains. The markets are on edge, and a bigger move this or more likely next week, shouldn‘t come as a surprise.

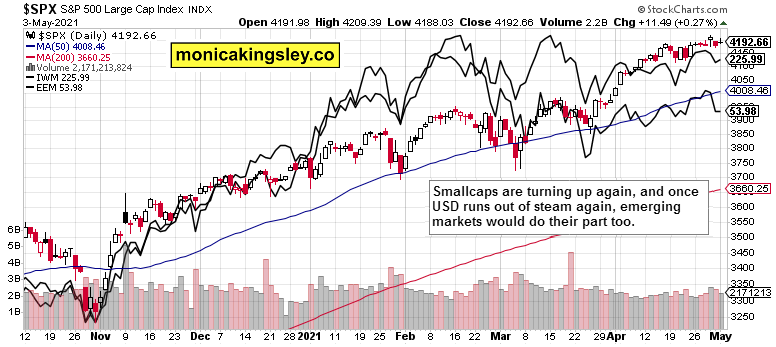

Smallcaps and emerging markets

The Russell 2000 turned higher on Monday, and emerging markets seem waiting for more signs of dollar weakness. Overall, the U.S. indices still continue outperforming the international markets.

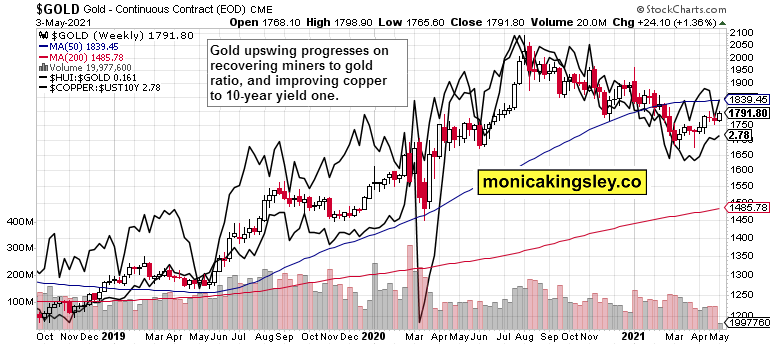

Gold and miners short-term

Volume returned into the gold market, and so did miners‘ outperformance. While these didn‘t close anywhere near their mid-Apr highs unlike gold, they had extremely undeperformed on Friday – what happens over the next few sessions would provide clue as to whether strength genuinely returned yesterday.

Gold and miners long-term

The copper to 10-year Treasury yield is edging higher again, and the miners to gold ratio strongly rebounded, proving my yesterday‘s point that the real parallels are the 2018 and 2019 gyrations, not the uniquely deflationary corona crash.

Summary

The S&P 500 remains vulnerable to short-term spikes in both directions, but the medium- term picture remains positive – the strong gains since late Mar are being worked off here before another upswing.

Gold and miners proved themselves yesterday, and scored strong gains in a universally supportive array of signals across commodities, Treasuries, and also the USD/JPY daily move. Well worth not retiring the benefit of the doubt given to the precious metals bulls – more gains are in sight.

All essays, research and information represent analyses and opinions of Monica Kingsley that are based on available and latest data. Despite careful research and best efforts, it may prove wrong and be subject to change with or without notice. Monica Kingsley does not guarantee the accuracy or thoroughness of the data or information reported. Her content serves educational purposes and should not be relied upon as advice or construed as providing recommendations of any kind. Futures, stocks and options are financial instruments not suitable for every investor. Please be advised that you invest at your own risk. Monica Kingsley is not a Registered Securities Advisor. By reading her writings, you agree that she will not be held responsible or liable for any decisions you make. Investing, trading and speculating in financial markets may involve high risk of loss. Monica Kingsley may have a short or long position in any securities, including those mentioned in her writings, and may make additional purchases and/or sales of those securities without notice.

Recommended Content

Editors’ Picks

AUD/USD remained bid above 0.6500

AUD/USD extended further its bullish performance, advancing for the fourth session in a row on Thursday, although a sustainable breakout of the key 200-day SMA at 0.6526 still remain elusive.

EUR/USD faces a minor resistance near at 1.0750

EUR/USD quickly left behind Wednesday’s small downtick and resumed its uptrend north of 1.0700 the figure, always on the back of the persistent sell-off in the US Dollar ahead of key PCE data on Friday.

Gold holds around $2,330 after dismal US data

Gold fell below $2,320 in the early American session as US yields shot higher after the data showed a significant increase in the US GDP price deflator in Q1. With safe-haven flows dominating the markets, however, XAU/USD reversed its direction and rose above $2,340.

Bitcoin price continues to get rejected from $65K resistance as SEC delays decision on spot BTC ETF options

Bitcoin (BTC) price has markets in disarray, provoking a broader market crash as it slumped to the $62,000 range on Thursday. Meanwhile, reverberations from spot BTC exchange-traded funds (ETFs) continue to influence the market.

US economy: slower growth with stronger inflation

The dollar strengthened, and stocks fell after statistical data from the US. The focus was on the preliminary estimate of GDP for the first quarter. Annualised quarterly growth came in at just 1.6%, down from the 2.5% and 3.4% previously forecast.