![]() Richard Perry

Richard Perry

Independent Analyst

Market Overview

Risk appetite continues to improve as the cycle of the trade dispute has decisively entered a pleasant phase. Instead of escalating the dispute, the US and China are exchanging concessions rather than tariffs right now as the two sides look towards the latest round of talks. China has talked about purchase of US agricultural goods, whilst President Trump has delayed his latest tariffs by a couple of weeks at the request of China. Although these are not game changing concessions, and are effectively just window dressing, at least they set the two sides in good spirit for the negotiations in October. This is helping a continued improved risk appetite which has pulled bond yields higher in the past couple of weeks. Traders continue to move out of assets at the safer end of the spectrum (such as the yen) and more towards higher risk (such as the Aussie and equities). Focus will be on monetary policy again today with attention on just how easy the ECB will be in their latest policy decision.

With the Eurozone economy once more seemingly on a lurch lower, all eyes will be on whether Mario Draghi can pull one final rabbit out of the hat. There is a broad expectation that the ECB will ease monetary policy today through a variety of measures. So this means that the ECB have a lot to live up to for any dovish surprise. However, there have been a number of prominent (even if likely minority) hawkish voices on the Governing Council opposing any resumption of QE. Jens Weidmann (Bundesbank) and Klaas Knot (Dutch central bank) are notably against using the big bazooka of bond purchases (restarting the Asset Purchase Program), so Mario Draghi has a significant job on his hands to win over the Governing Council on his last outing. A cut to the deposit rate is nailed on, but how much? Consensus suggests -10 basis points but -20 basis points would not be a huge surprise either. However the policy package could easily include tiering of the deposit rate to mitigate the impact on Eurozone banks (positive for the sector). Forward guidance is also to be watched for any changes to the current “expects the key ECB interest rates to remain at their present or lower at least through the first half of 2020”. Finally what about QE? Markets are priced for a resumption of asset purchases, but how significant? Anything around or more than €50bn per month would be considerable and a dovish surprise. However, given that markets have been pricing for a significant dovish package from the ECB since the last meeting on 25th July and that Mario Draghi is unlikely to be able to say this would have been a “unanimous” decision, a relatively small QE announcement would be a dovish disappointment.

Wall Street closed decisively higher again, with the S&P 500 closing at 3001 and +0.7% on the session, whilst US futures are once more pointing higher +0.2% in early moves today. This has helped a good session for the bulls in Asia, with the Nikkei +0.8% and Shanghai Composite +0.7%. In Europe, futures are looking higher once more with the FTSE futures +0.4% and DAX Futures +0.5%. In forex trading, the risk positive line continues as JPY underperforms once more, whilst AUD and NZD are again stronger. EUR is flat ahead of the ECB. In commodities, there is consolidation on gold and silver after finding support yesterday, with oil bouncing half a percent after falling sharply yesterday.

The ECB is the key event today on the economic calendar, but US inflation is not far behind. After a quiet morning, the ECB interest rates and its likely policy package are announced at 1245BST. Consensus expects a -10bps cut on the deposit rate to -0.50% (from -0.40% in July) with the main refinancing rate held once more at 0.0%. However, also keep an eye out for details of other measures, including potential tiering of deposit rates, changes to forward guidance and also potentially a new asset purchase program. Mario Draghi’s final press conference as ECB President is at 1330BST. At the same time, the US CPI numbers are released for August at 1330BST, with expectations that headline CPI would hold at +1.8% (+1.8% in July) with core CPI a tick higher at +2.3% (from +2.2% in July). Weekly Jobless Claims at 1330BST are expected to continue around recent levels at 215,000 (a shade below 217,000 last week).

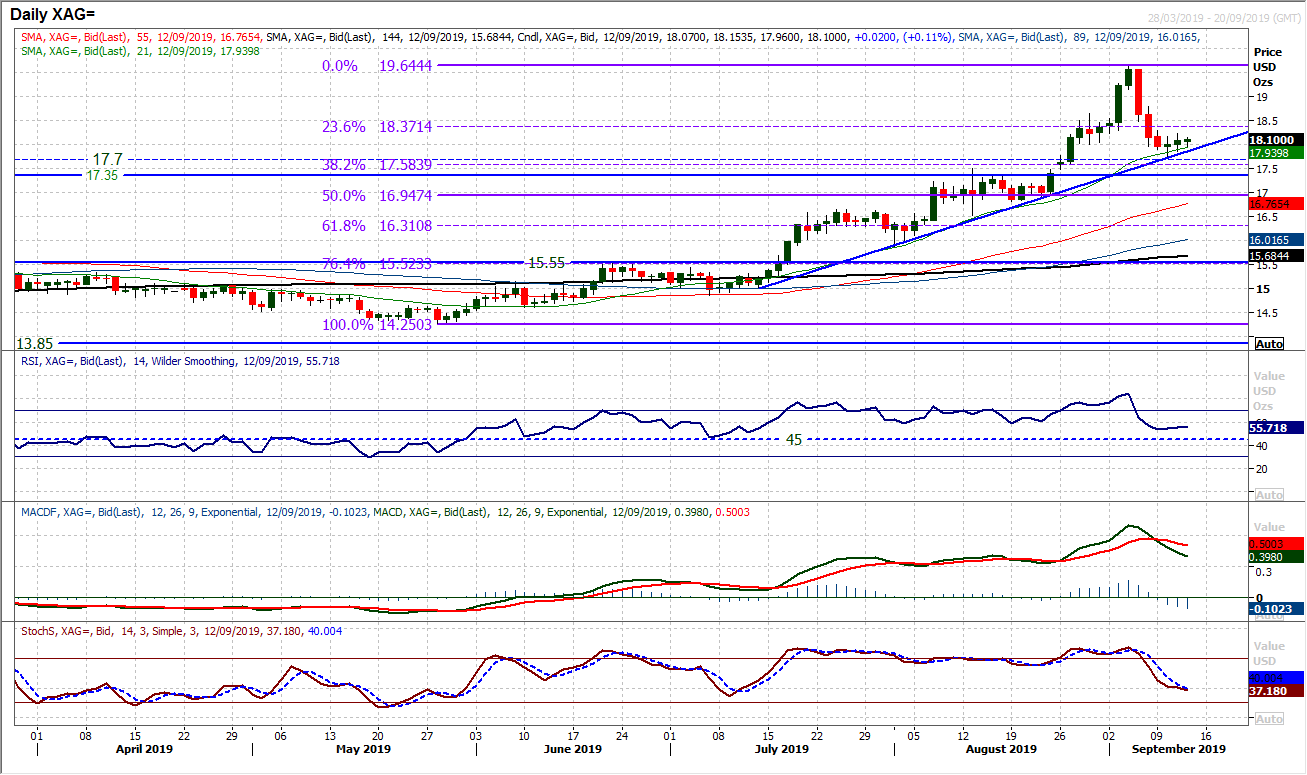

Chart of the Day – Silver

The precious metals are sitting at a crossroads ahead of the ECB meeting. Silver has corrected sharply in the past week, but the move has unwound the market into a clutch of technical support. The two month uptrend has held up the last two completed sessions captured and rises around $17.86 today. The rising 21 day moving average which has also been an excellent basis of support in the past two months and continues to flank the market at $17.94. Finally, the unwinding move has been back to find support at $177.74 which was all but bang on the $17.70 old key breakout of the 2018 high. A couple of rather neutral and arguably indecisive (at least relative to recent trading) daily candlesticks in the past two sessions around this technical support area suggests the traders are contemplating how to negotiate this crossroads now. A deterioration in momentum indicators has been a drag recently, but RSI remains above 50 (and holding), whilst Stochastics have unwound to 40 (around where the July buy signal kicked in). So it seems likely that traders are waiting for the ECB decision for whether this is a bull market unwind, or a continued correction. A close below $17.74 would be a catalyst for continued correction for $17.40. Above the 236% Fib of the big rally at $18.37 would resume the bull momentum.

EUR/USD

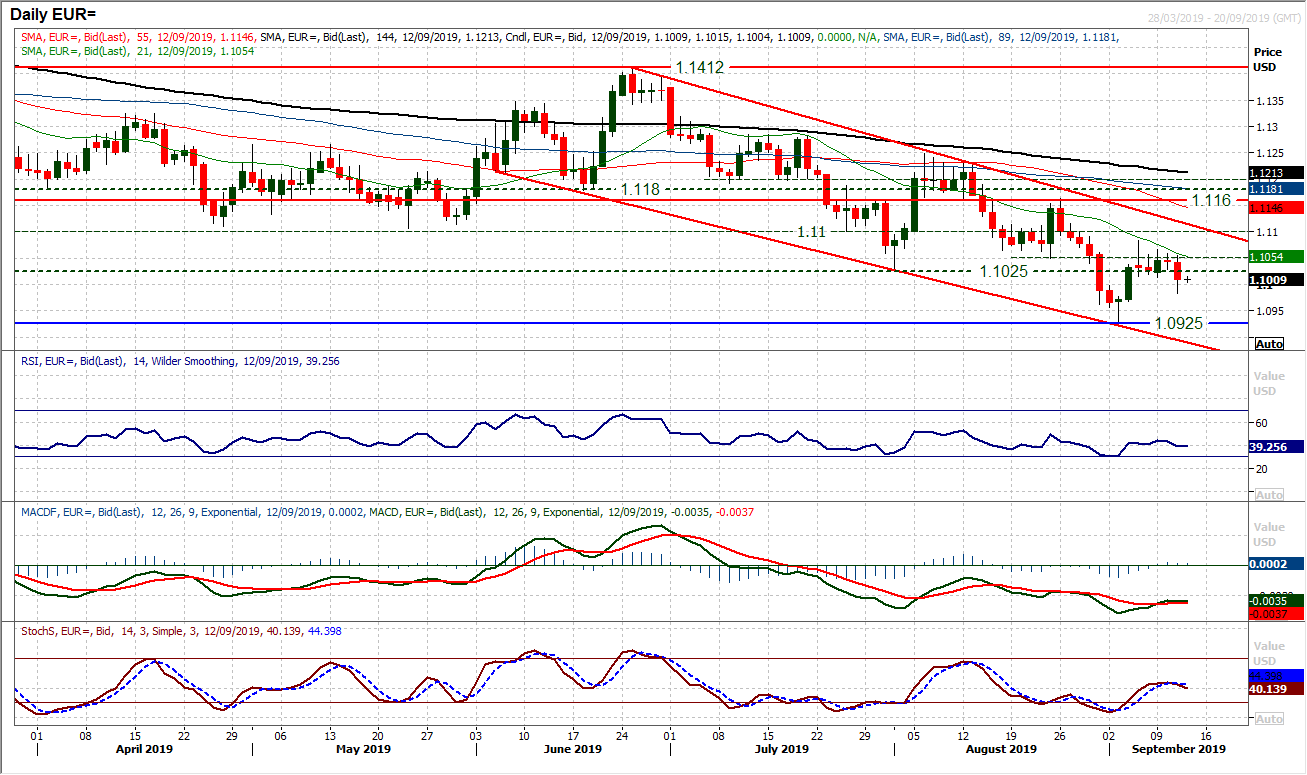

With a minor bout of dollar strength yesterday, the pair was dragged back below $1.1000 (albeit briefly). Given the uncertainty of the ECB meeting today, we continue to believe direction will not be decisive until the market knows more of the Governing Council’s intentions on monetary policy. Technically we continue to see a medium term downtrend channel and negative medium term momentum configuration. Subsequently, on a technical basis rallies are a chance to sell. With the RSI stuttering around 40 and Stochastics bear crossing around 50, technical traders will be set up for renewed weakness today. However, we need to be more cautious in light of the wide variety of options the ECB has with which to ease policy. The euro closed at a one week low yesterday, leaving resistance building up overhead between $1.1050/$1.1085. This will be the main barrier to recovery if the ECB fails to live up to dovish expectations. Initial support is yesterday’s low at $1.0985 but a close under $1.1000 (if the ECB can hit expectations or more) would re-open $1.0925 and possibly below.

GBP/USD

It is interesting to see that the wind has just been lost from the sails of sterling recovery since the UK Parliament has been suspended (or prorogued). Cable is now stuttering under the resistance at $1.2380. However, equally, the breakout above $1.2305 (the old August high) is being maintained. Momentum remains on its path of improvement though, with RSI solid above 50, Stochastics strong and MACD lines ever closer to rising above neutral. Whilst the higher low at $1.2230 remains intact, the bulls will be relatively content, leaving a support band $1.2230/$1.2305. To resume the recovery the bulls need a close above $1.2380 to really open the way towards a test of the $1.2580 resistance again. A period of contemplation, but we are now buyers into weakness.

USD/JPY

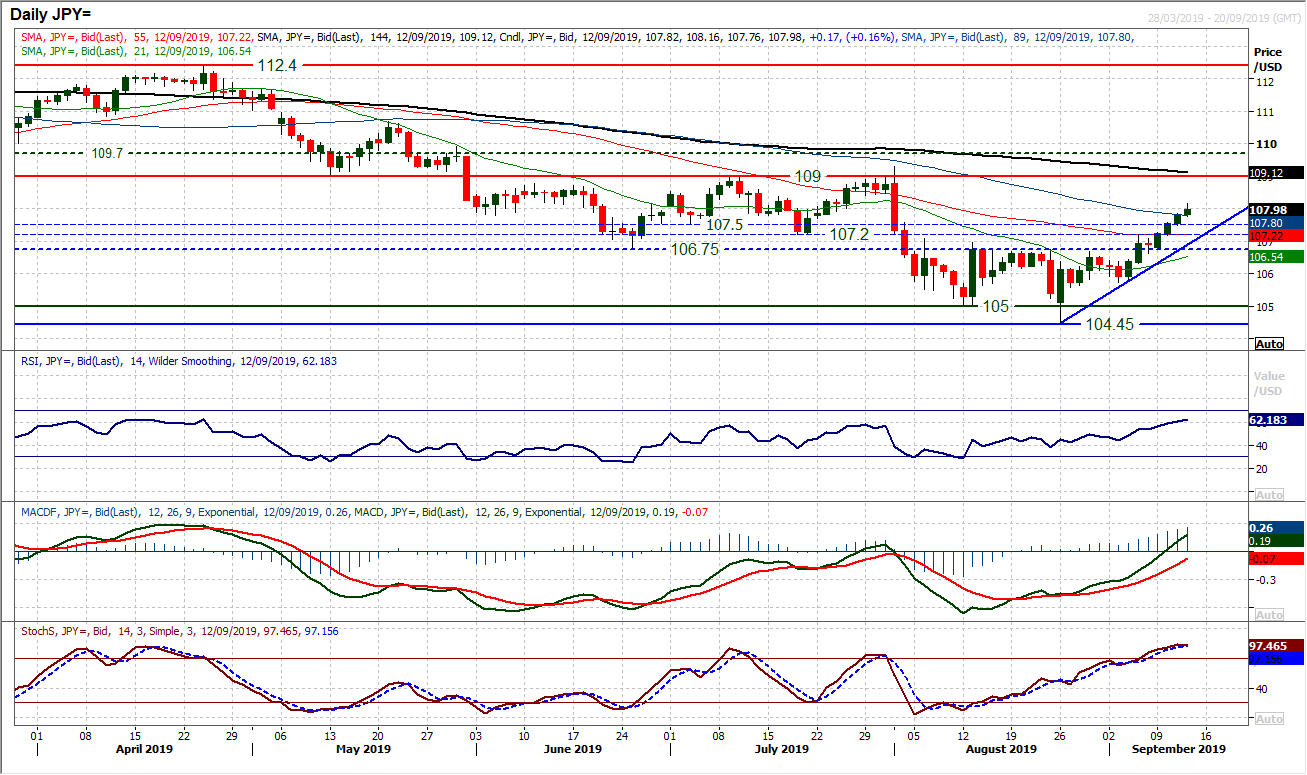

The bulls continue to run higher as the pair has used what is now a pivot at 107.50 as a basis of support for yesterday’s latest bull candle. Another positive candlestick pulling clear of the 106.75/107.50 pivot band now leaves this as a band of support to build from. The breakout above 107.50 also comes with the RSI moving into the 60s which is a five month high, whilst the Stochastics are bullishly configured at five month highs, and the MACD lines are accelerating strongly towards neutral. With a near term uptrend supportive at 106.90 today, corrections finding support in the 106.75/107.50 band are now a chance to buy. The next real resistance is not until 109.00. Another positive candle today is already setting up and if this can be sustained through the ECB meeting, we like the look of continued gains.

Gold

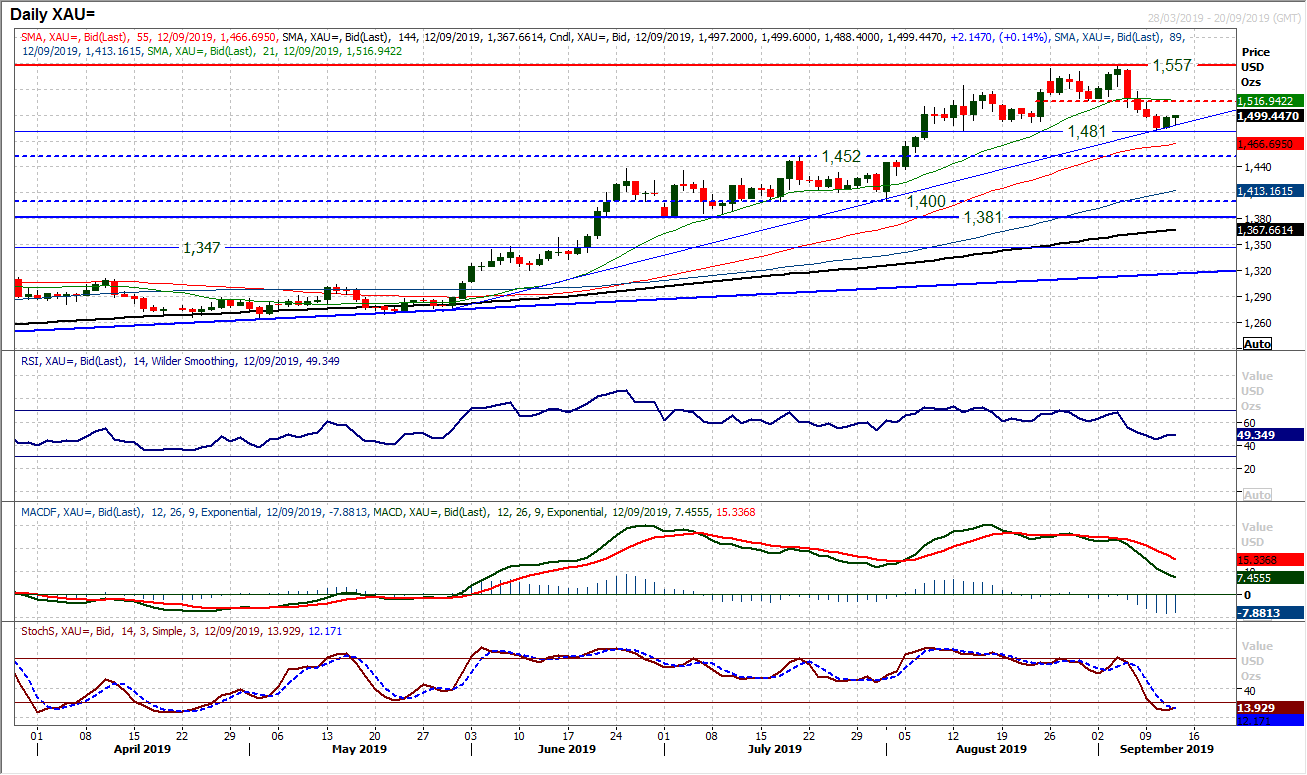

A tentative uptrend of four months formed yesterday as the gold correction finally found a basis of support from $1484. This also maintained the $1481 key support of the August trading range. How the market responds now to these technical supports will be key. We are concerned that the 21 day moving average which has been such a good basis of support for several months, has now turned lower at $1517 and this could begin to restrict any potential renewed buying pressure. Given the deterioration in momentum indicators (RSI under 50, Stochastics bearishly configured below 20 and MACD lines accelerating lower), the pressure on $1481 is likely to continue. The market is consolidating early today (ahead of the ECB) and the hourly chart shows a broken mini downtrend along with flattening moving averages. However a failed rally under $1502 would maintain bear pressure.

WTI Oil

A second successive (decisive) negative candlestick is seriously questioning whether the bulls have it in them for a recovery. Losing almost 3% in the session is a concern but an early rebound today, from the 38.2% Fib retracement which is supportive around $55.55 is a level that needs to hold. How the bulls respond into the close will be key now. Maintaining this run of recent higher lows (latest at $54.85) is necessary for the bulls to retain any degree of recovery potential. The bulls will also need to quickly reclaim the breakout above the resistance band $56.90/$57.75. Momentum retains an edge of positivity even though the immediate tick lower has dragged on the Stochastics.

Dow Jones Industrial Average

Wall Street continues its merry way higher. There have now been two consecutive decisive bull candlesticks in a row on the daily chart where we have seen the buyers strong through to the end of a session which has closed at the day high. Continuing the breakout to five week highs, and closing decisively above 27,000 the Dow is well on course now for a retest of the all-time high at 27,399. Momentum is increasingly strong but with further upside potential too. The RSI is rising decisively now into the low 60s now, whilst MACD lines are now accelerating above neutral and Stochastics very strongly configured. Intraday weakness is consistently being bought into, with the market now having closed higher on six straight sessions. The support at the old pivot of 26,965 is now key, with yesterday’s low at 26,885 initially supportive. There is minor resistance at 27,280 but we expect 27,399 to be tested in due course.

Note: All information on this page is subject to change. The use of this website constitutes acceptance of our user agreement. Please read our privacy policy and legal disclaimer. Opinions expressed at FXstreet.com are those of the individual authors and do not necessarily represent the opinion of FXstreet.com or its management. Risk Disclosure: Trading foreign exchange on margin carries a high level of risk, and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to invest in foreign exchange you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss of some or all of your initial investment and therefore you should not invest money that you cannot afford to lose. You should be aware of all the risks associated with foreign exchange trading, and seek advice from an independent financial advisor if you have any doubts.

Recommended Content

Editors’ Picks

EUR/USD fluctuates near 1.0700 after US data

EUR/USD stays in a consolidation phase at around 1.0700 in the American session on Wednesday. The data from the US showed a strong increase in Durable Goods Orders, supporting the USD and making it difficult for the pair to gain traction.

USD/JPY refreshes 34-year high, attacks 155.00 as intervention risks loom

USD/JPY is renewing a multi-decade high, closing in on 155.00. Traders turn cautious on heightened risks of Japan's FX intervention. Broad US Dollar rebound aids the upside in the major. US Durable Goods data are next on tap.

Gold stays in consolidation above $2,300

Gold finds it difficult to stage a rebound midweek following Monday's sharp decline but manages to hold above $2,300. The benchmark 10-year US Treasury bond yield stays in the green above 4.6% after US data, not allowing the pair to turn north.

Worldcoin looks set for comeback despite Nvidia’s 22% crash Premium

Worldcoin price is in a better position than last week's and shows signs of a potential comeback. This development occurs amid the sharp decline in the valuation of the popular GPU manufacturer Nvidia.

Three fundamentals for the week: US GDP, BoJ and the Fed's favorite inflation gauge stand out Premium

While it is hard to predict when geopolitical news erupts, the level of tension is lower – allowing for key data to have its say. This week's US figures are set to shape the Federal Reserve's decision next week – and the Bank of Japan may struggle to halt the Yen's deterioration.