- RBNZ expected to cut the official cash rate to 0.75%, a record low

- Weak inflation and expectations could prompt cut

- Slowing economy, rising unemployment, lower New Zealand Dollar additional factors

The Reserve Bank of New Zealand (RBNZ) will announce its decision on the official cash rate at 1:00 GMT Wednesday November 13th, 20:00 EST on Tuesday November 12th.

Forecast

The RBNZ is predicted to reduce the official cash rate by 25 basis points to 0.75%. If completed it would be the third cut this year and bring the reductions to 1.0% since the bank began in May.

RBNZ balancing inflation and growth and economic stabilization

New Zealand’s central bank may take its main interest rate to new low but the case for reductions is less clear than it was six months ago when it began this rate cycle.

Economists in the Reuters Survey expect the RBNZ to cut the official cash rate by 0.25% on Wednesday to 0.75% a record low for modern New Zealand. The futures markets was pricing a 76% chance for a reduction on Monday, up from 60% earlier.

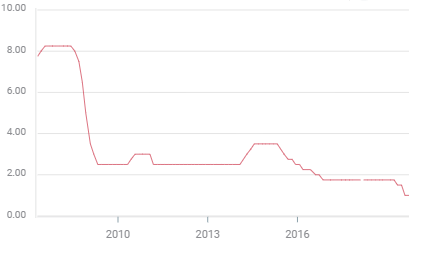

RBNZ Official Cash Rate

The RBNZ has been the most aggressive of the central banks reducing rates this year. It was the first to take steps to combat what it saw as weak inflation and slowing global and domestic growth. Governor Adrian Orr started with a 0.25% decrease in May, followed by a 0.5% cut in August.

At the last decision the bank’s economic review stated that there was room for further stimulus “if necessary” but developments since have somewhat undermined the case for another 0.25% cut.

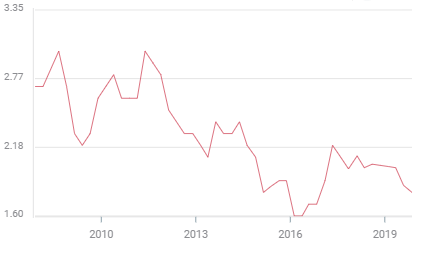

Consumer Price Index

Consumer prices in the third quarter rose at a 1.5% annual rate, slightly better than the 1.4% expectation though down from the second quarter’s 1.7% rate. Inflation has been stable this year averaging 1.57% through the third quarter with a range of 1.5% to 1.7%.

CPI

FXStreet

From 2015 through 2018 the range was much wider, extending from 0.1% in the first quarter of 2015 and again in the fourth quarter of 2016 to 2.2% in the first three months of 2017 followed by a dip to 1.1% in the first quarter of 2018. The relative stability this year may be something the bank is reluctant to disturb.

Inflation expectations however in the fourth quarter dropped to 1.8% their lowest in three years, missing the 1.86% forecast and they have fallen from 2.11% in the first quarter of 2018.

Inflation Expectations

FXStreet

Unemployment, GDP and business confidence

Unemployment climbed to 4.2% in the third quarter from 3.9% in the prior three months. But as the last quarter had the lowest rate since the financial crisis and the average in 2018 was 4.3% it is not necessarily sign of fatigue in the labor market. The economy grew at 2.1% pace in the first half down from 3.2% a year earlier.

Unemployment Rate

FXStreet

Business confidence in October rose from an 11-year low perhaps prompted by the seeming trade detente between China and the United States. The threat of their trade war and the dependence on the New Zealand economy on exports to the Asian market and China in particular had been one of the main reason behind the initial rate cut in May.

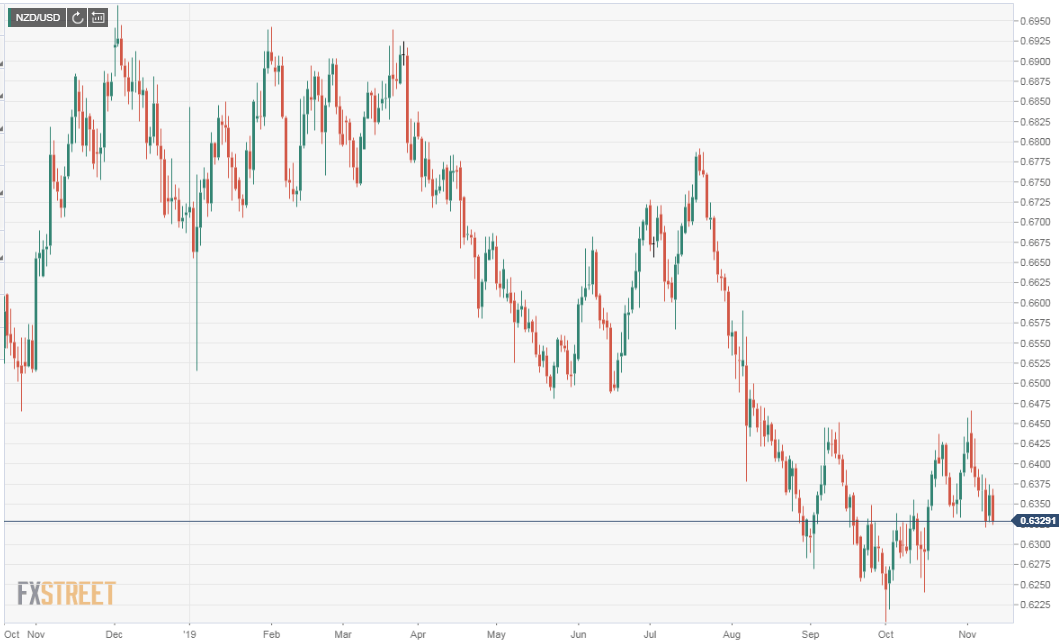

The New Zealand Dollar

The New Zealand Dollar also known as the Kiwi for the national bird, has been one of the weakest currencies against the US dollar this year.

From its January high on the 31st of 0.6912 it lost 9.7% to the low this year of 0.6244 on October 1st. Since then the recovery has been limited, closing at 0.6361 on November 11th, down 7.9% from the January top. In comparison the Australian Dollar has lost 5.9% versus the US currency in the same period.

Conclusion

The RBNZ’s early move to economic support will receive a final installment this month. The changing background, particularly the incipient trade deal between the US and China and the Federal Reserve halt, will likely induce a pause down under as well.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

EUR/USD holds gains above 1.0600, focus on ECB/ Fed speeches

EUR/USD is holding gains above 1.0600 in European trading on Wednesday. The US Dollar has entered a consolidative mode, allowing the Euro to heal its wounds. The EUR/USD rebound appears limited amid Fed-ECB policy divergence. ECB and Fed speeches awaited.

GBP/USD rises through 1.2450 after UK inflation data

GBP/USD gains traction and rises above 1.2450 in the European morning on Wednesday. The UK's ONS reported that the annual inflation edged lower to 3.2% in March. This reading came in above the market expectation of 3.1% and helped Pound Sterling find demand.

Gold pauses before the next push higher, Fedspeak awaited

Gold price is battling it out just below $2,400 early Wednesday after witnessing a muted close a day ago. Gold makes another attempt to recapture the $2,400 level, as the US Dollar follows a minor pullback in the US Treasury bond yields, awaiting a fresh bunch of US Federal Reserve speakers.

XRP tests $0.50 resistance after Ripple CLO clarifies that no pretrial conference took place with SEC

XRP is stuck below $0.50 resistance after failing to close above this level since Monday. Ripple CLO Stuart Alderoty said late Tuesday there was no pretrial conference since the SEC dropped charges against executives.

World economy: To cut or not to cut (simultaneously)?

US inflation March figure, again higher than expected, put an end to the scenario of a simultaneous first rate cut by the Fed, the ECB, and the BoE in June.