![]() ING Global Economics Team

ING Global Economics Team

ING Economic and Financial Analysis

Appetite for high beta fixed income has allowed the ECB to reduce its overweight in peripheral bonds. There is no sign of US curve dis-inversion yet - we think this is most likely to occur with a long-end sell off.

ECB reduces its peripheral bond overweight

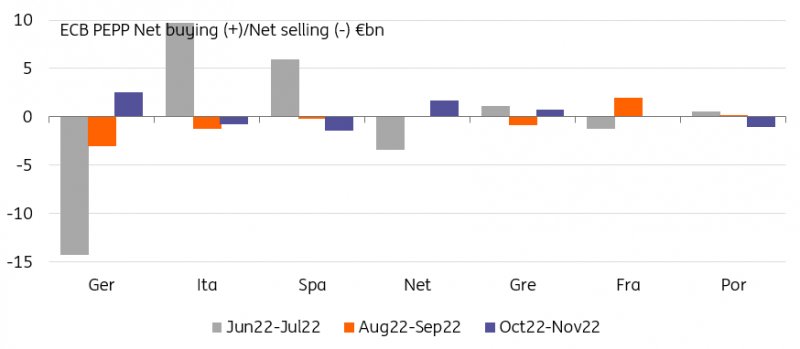

The ECB didn’t use the flexibility offered by the PEPP’s redemption to lean against wide sovereign spreads in the months of October and November. On the contrary, data show that it increased its holding of core (eg Netherlands and Germany) and reduced its holding of periphery (eg Spain, Portugal and Italy). The changes may be explained in part by different timing between redemption and reinvestment of the proceeds but there seems to be a trend here: the overweight in peripheral countries is at least being partially unwound.

Looking at market moves of late, this is understandable. Spreads have been on a tightening spree, suggesting the higher-beta sovereign bond markets require less of the ECB’s support. This is good news, until it isn’t anymore. As long as the ECB retains the flexibility to lean against volatility in the sovereign bond markets all should be well. The looming QT announcement is one key risk to this. So far, spreads have tightened alongside the improvement in global risk sentiment. That tightening cannot be entirely explained by the rally in core rates, and suggests instead genuine risk appetite for high beta fixed income.

The ECB has partially unwound its summer intervention in peripheral markets

Source: Refinitiv, ING

No sign of re-steepening yet

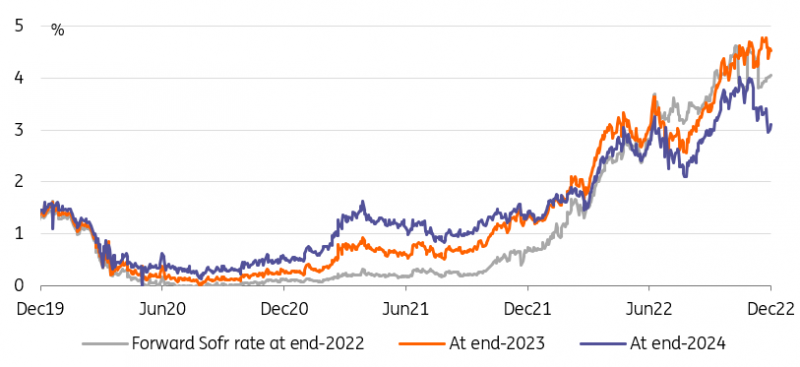

If the bond rally has stalled, which itself is still unsure, there is no sign yet of curve re-steepening. In the US in particular, where the Fed has presumably the most room to cut rates, the curve remains as inverted as ever. Dis-inversion can occur for two reasons. Firstly, front-end rates can drop on expectations of imminent Fed easing. In our view, this is only realistic once inflation is clearly on a path towards reaching the Fed’s target, and the economy is near a recession. We think these conditions will only be met by mid-2023.

The other reason for a curve dis-inversion is if long-end rates reverse some of their November rally. This looks a more realistic scenario in the near-term. Risk appetite, from stock to credit, has received a boost once it became clear that the Fed was easing off on the pace of hikes. This has also boosted demand for duration on the Treasury curve as investors look more kindly to any kind of investment risk. The problem is that it is not yet clear that the Fed is near the end of its cycle. Fed Funds forwards are steeply inverted from late 2023, implying the odds of a rate cut are rising. We think this is right but that pricing may be reversed soon if data doesn’t worsen quickly.

The rally in long-end bonds has come with Fed Funds forwards pricing rate cuts in 2024

Source: Refinitiv, ING

Read the original analysis: Rates Spark: without the stabilisers

Content disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/content-disclaimer/

Recommended Content

Editors’ Picks

EUR/USD regains traction, recovers above 1.0700

EUR/USD regained its traction and turned positive on the day above 1.0700 in the American session. The US Dollar struggles to preserve its strength after the data from the US showed that the economy grew at a softer pace than expected in Q1.

GBP/USD returns to 1.2500 area in volatile session

GBP/USD reversed its direction and recovered to 1.2500 after falling to the 1.2450 area earlier in the day. Although markets remain risk-averse, the US Dollar struggles to find demand following the disappointing GDP data.

Gold holds around $2,330 after dismal US data

Gold fell below $2,320 in the early American session as US yields shot higher after the data showed a significant increase in the US GDP price deflator in Q1. With safe-haven flows dominating the markets, however, XAU/USD reversed its direction and rose above $2,340.

XRP extends its decline, crypto experts comment on Ripple stablecoin and benefits for XRP Ledger

Ripple extends decline to $0.52 on Thursday, wipes out weekly gains. Crypto expert asks Ripple CTO how the stablecoin will benefit the XRP Ledger and native token XRP.

After the US close, it’s the Tokyo CPI

After the US close, it’s the Tokyo CPI, a reliable indicator of the national number and then the BoJ policy announcement. Tokyo CPI ex food and energy in Japan was a rise to 2.90% in March from 2.50%.