Market tension re-North Korea continues to sap global equity markets, with Euro bourses following their Asian counterparts into the red ahead of the U.S open as the saber rattling continues and investors remain on edge.

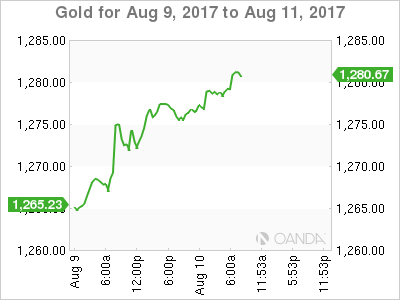

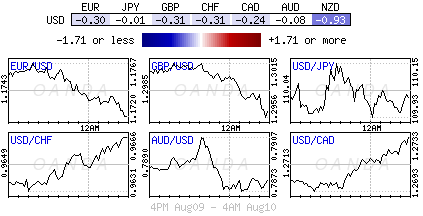

Capital Markets are on the defence as a risk-off tone dominates proceedings, with gold ($1,278.34) and the Japanese yen (¥109.810) advancing and sovereign bond prices edging higher as tension grows between the U.S and North Korea. The ‘mighty’ dollar remains better bid against G10 currency pairs ahead of tomorrow’s U.S inflation data (08:30 am EDT), while oil prices advance.

Expect Fed speak this morning to shape a portion of the U.S dollars direction. The Fed’s William Dudley (dove, FOMC voter) delivers opening remarks at the Economic Press Briefing on Wage Inequality in the Region in New York City, followed by a question and answer session (10:00 am EDT).

1. Stocks Sea of red

Asian stocks largely finished well off their session lows, but still dropped again following yesterday’s geopolitics-fuelled declines.

In Japan, Nikkei edged down -0.2% ahead of Friday’s holiday as investors eye North Korea. The broader Topix shed -0.1%.

In Hong Kong, profit taking hit regional bourses. The Hang Seng index ended down -1.1%, while the China Enterprises Index lost -1.7%.

Down-under, Australia’s S&P/ASX 200 Index lost -0.1%, while in China, shares followed regional peers lower, led by materials stocks. The blue-chip CSI300 index fell -0.4%, while the Shanghai Composite Index also lost -0.4%.

In Europe, regional indexes opened lower and continue to underperform as geo-political concerns still weigh on risk sentiment, Commodity prices are trading higher, but again fail to support materials stocks.

U.S equities are expected to open deep in the red (-0.4%).

Indices: Stoxx50 -0.7% at 3,444, FTSE -1.1% at 7,410, DAX -0.7% at 12.065, CAC-40 -0.5% at 5,119, IBEX-35 -0.7% at 10,525, FTSE MIB -0.4% at 21,764, SMI -0.3% at 9,003, S&P 500 Futures -0.4%.

2. Oil rises as inventory overhang erodes, gold higher

Ahead of the U.S open, oil prices remain better bid, lifted by a sustained decline in inventories and as Saudi Arabia prepared to cut crude supplies to its Asian accounts.

Note: Crude is down -7% year-to-date, on concerns that OPEC may not be able to force global oil inventories to drop by cutting production.

The Saudi’s this week indicated that they are prepared to cut supplies to most buyers in Asia by up to +10% next month.

Brent crude futures are up +29c at +$52.99 a barrel, while U.S West Texas Intermediate (WTI) crude is up +17c at +$49.73.

Yesterday’s weekly EIA numbers saw U.S inventories (-6.5m vs. -1.5m barrels) at their lowest since October, having fallen for 10 of the last 12 weeks.

Gold prices (up +0.1% to +$1,278.51 per ounce) linger atop of its two-month high print overnight, as rising tensions on the Korean peninsula continue to support safe-haven demand.

Platinum prices fell -0.3% to +$968.20 per ounce. In yesterday’s session, it marked its highest print since April at +$980.60.

3. Yields lower on risk aversion

Europe’s bond yields trade atop of their six-week lows as North Korea outlined detailed plans for a missile strike near the U.S territory of Guam.

The yield on Germany’s 10-year Bund is a tad higher ahead of the U.S open at +0.44%, just above its low of +0.42%print yesterday. U.S Treasuries (declined less than -1 bps to +2.24%) and U.K Gilts (+1.14%) are also trading a touch above Wednesday’s six-week lows.

Note: In the U.K, issuance of new Gilts is scheduled to resume Aug. 23. Until then, lack of supply should make it difficult for gilt yields to rise and this should also help gilts out-perform U.S treasuries in the near term.

The medium-term outlook depends on the BoE – Governor Carney and company is expected to find it difficult to hike policy rate given the downside risks to growth.

4. Dollar in demand, a tad

The markets continue to look for direction after yesterday’s sharp moves and geopolitical concerns will dominate investor thinking in the coming days.

Both the CHF and JPY managed to notch up impressive gains yesterday outright after President Trump warned North Korea that it would face “fire and fury” if it threatened the U.S.

Ahead of the U.S open, safe haven currencies, like the CHF ($0.9658) and JPY (¥109.81), are consolidating this weeks recent gains inspired by a deepening anxiety over tensions between Washington and Pyongyang.

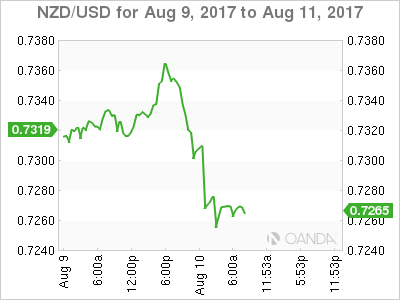

Elsewhere, the NZD (NZ$0.7268) is a good bit softer after Reserve Bank of New Zealand (RBNZ) Governor Wheeler indicated that the overnight cash rate (OCR) should stay steady for the foreseeable future. The futures market had been pricing in a Kiwi rate hike within 12-months, rather than a mid-2019 date indicated by the RBNZ overnight.

5. Reserve Bank of New Zealand (RBNZ) monetary policy

RBNZ Governor Wheeler delivered his last major policy statement yesterday before retiring next month, leaving interest rates unchanged (+1.75%) and keeping the guidance ‘neutral.’

Note: This will give the new governor maximum optionality should activity data disappoint, wages growth remain weak, and inflation continue to undershoot target.

In his press conference, Governor Wheeler did confirm that they monitor a “traffic light system” for currency intervention closely, but would not comment on whether currency strength is affecting the system. He believes that intervention in FX remains open to policy makers.

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities.

Opinions are the authors — not necessarily OANDA’s, its officers or directors. OANDA’s Terms of Use and Privacy Policy apply. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Recommended Content

Editors’ Picks

AUD/USD stands firm above 0.6500 with markets bracing for Aussie PPI, US inflation

The Aussie Dollar begins Friday’s Asian session on the right foot against the Greenback after posting gains of 0.33% on Thursday. The AUD/USD advance was sponsored by a United States report showing the economy is growing below estimates while inflation picked up. The pair traded at 0.6518.

EUR/USD faces a minor resistance near at 1.0750

EUR/USD quickly left behind Wednesday’s small downtick and resumed its uptrend north of 1.0700 the figure, always on the back of the persistent sell-off in the US Dollar ahead of key PCE data on Friday.

Gold soars as US economic woes and inflation fears grip investors

Gold prices advanced modestly during Thursday’s North American session, gaining more than 0.5% following the release of crucial economic data from the United States. GDP figures for the first quarter of 2024 missed estimates, increasing speculation that the US Fed could lower borrowing costs.

Bitcoin price continues to get rejected from $65K resistance as SEC delays decision on spot BTC ETF options

Bitcoin (BTC) price has markets in disarray, provoking a broader market crash as it slumped to the $62,000 range on Thursday. Meanwhile, reverberations from spot BTC exchange-traded funds (ETFs) continue to influence the market.

US economy: Slower growth with stronger inflation

The dollar strengthened, and stocks fell after statistical data from the US. The focus was on the preliminary estimate of GDP for the first quarter. Annualised quarterly growth came in at just 1.6%, down from the 2.5% and 3.4% previously forecast.