Market News Today – Gilt yields closed higher after stronger than expected US inflation numbers, while Eurozone bonds, in particular BTPs, got a boost from the ECB announcement, which affirmed the commitment to keep monthly PEPP purchases “significantly” higher than at the start of the year. The ECB is essentially in wait and see mode and seems to be focusing very much on the outlook for the travel and tourism sector against the background of new virus variants. Central banks successfully convinced markets that the spike in inflation is transitory and after the spike in US inflation yesterday, the Eurozone May inflation round will likely look tame by comparison.

In Asia, Australia and New Zealand bonds found buyers, but in South Korea bonds extended losses after comments from the central bank’s chief economist on normalizing policy. For now the factors driving the jump look transitory, but there are some lingering concerns that it could become entrenched and there was talk that central bankers will discuss tapering at the Jackson Hole meeting over the summer.

In Europe, the bunch of data releases out of the UK at the start of the session was largely bond friendly, despite monthly GDP being a tad weaker than expected at 2.3% and industrial and manufacturing production unexpectedly dropping -0.3% and -1.3% respectively. The visible trade deficit meanwhile remains sizeable at around GBP 11 bln.

In FX markets the Yen struggled and USDJPY lifted to 109.42, while the EUR strengthened and EURUSD is at 1.2192, while Cable is little changed at 1.4182. Stock markets mostly managed slight gains as markets continued to digest the uptick in US inflation. JPN225 is up 0.04%, GER30 and UK100 futures are still up 0.1% and 0.2% respectively and US futures are also higher, led by a 0.11% rise in the USA100. USOIL is at $70.14 per barrel.

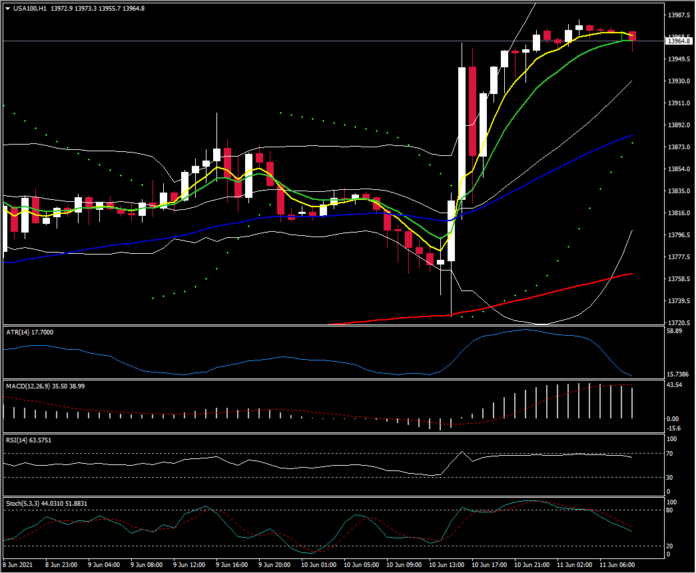

Biggest FX Mover – USA100 just a breath below 14k. Currently the rally has stalled, with fast MAs flattened along with RSI at 63 while Stochastic is sloping lower pointing to 20 barrier. ATR (H1) at 17.70 and ATR (D) at 142.70.

Disclaimer: Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of purchase or sale of any financial instrument.

Recommended Content

Editors’ Picks

EUR/USD extends gains above 1.0700, focus on key US data

EUR/USD meets fresh demand and rises toward 1.0750 in the European session on Thursday. Renewed US Dollar weakness offsets the risk-off market environment, supporting the pair ahead of the key US GDP and PCE inflation data.

GBP/USD extends recovery above 1.2500, awaits US GDP data

GBP/USD is catching a fresh bid wave, rising above 1.2500 in European trading on Thursday. The US Dollar resumes its corrective downside, as traders resort to repositioning ahead of the high-impact US advance GDP data for the first quarter.

Gold price edges higher amid weaker USD and softer risk tone, focus remains on US GDP

Gold price (XAU/USD) attracts some dip-buying in the vicinity of the $2,300 mark on Thursday and for now, seems to have snapped a three-day losing streak, though the upside potential seems limited.

Injective price weakness persists despite over 5.9 million INJ tokens burned

Injective price is trading with a bearish bias, stuck in the lower section of the market range. The bearish outlook abounds despite the network's deflationary efforts to pump the price.

US Q1 GDP Preview: Economic growth set to remain firm in, albeit easing from Q4

The United States Gross Domestic Product (GDP) is seen expanding at an annualized rate of 2.5% in Q1. The current resilience of the US economy bolsters the case for a soft landing.