![]() Clint Sorenson, CFA, CMT

Clint Sorenson, CFA, CMT

WealthShield

Today, investors are faced with equity markets at all-time highs and trillions of dollars in fixed income generating negative yields. The expected return outlook for traditional asset classes is weak, and with volatility near alltime lows, the likelihood of an uptick is high. Historically, global macro has held up well in these types of markets, in part, because of a long volatility bias and active hedging. Amid concerns about potentially unsteady and down markets, we believe two of the strategies employed by global macro managers are particularly worthy of consideration today: long volatility and tail risk.

What is Global Macro?

Global macro is an investment style that is very diverse: Managers have the flexibility to take long or short positions in any global market using any liquid financial instrument. These strategies can be highly opportunistic and have the potential to generate strong risk-adjusted returns in challenging markets.

Designed to Behave Differently

Historical spikes in market volatility and major inflection points in central bank policy measures have shown us that correlations among asset classes are not stable. Indeed, during severe market dislocations, diversification benefits across asset classes can quickly evaporate as correlations spike. Historically, global macro has bucked this trend. For example, as illustrated in Display 1, correlations between global macro, as proxied by HFRI Macro (Total) Index, and U.S. equities actually decreased during the technology bubble and the credit crisis.

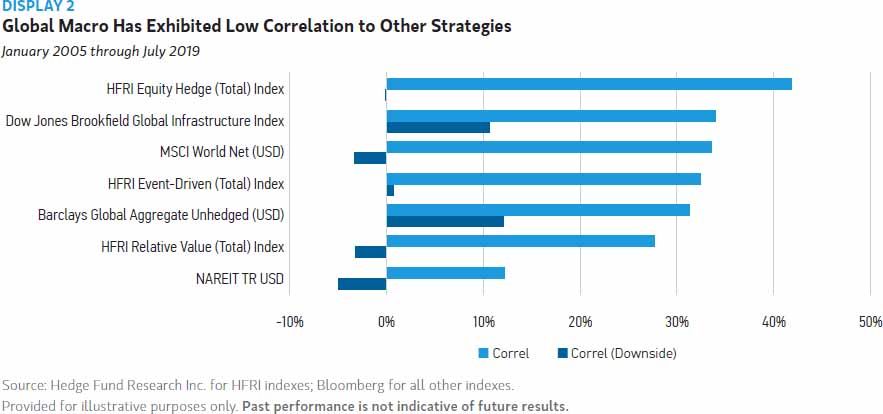

Looking across asset classes more broadly, global macro has historically exhibited relatively low correlation to bond markets as well as to other hedge fund strategies, particularly in crisis periods (Display 2).

Performance in Challenging Markets

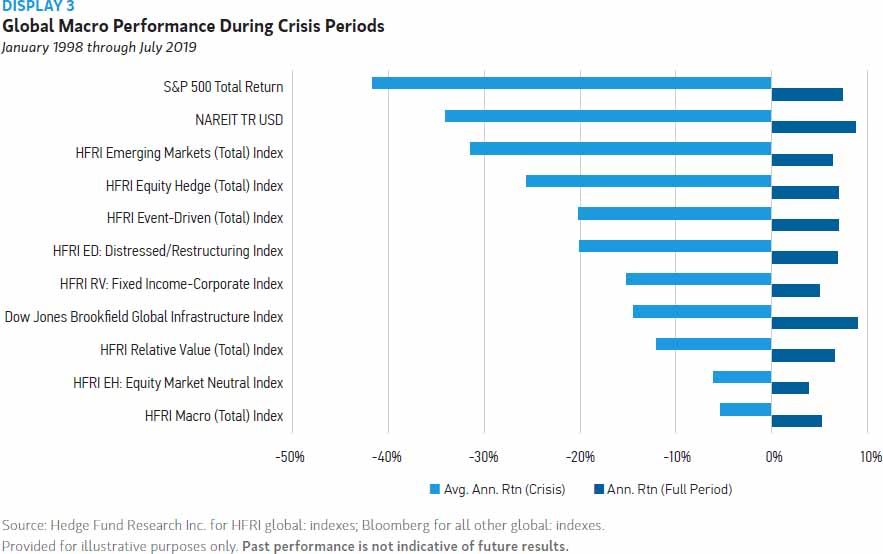

On an absolute return basis, global macro has tended to hold up well during market crises (Display 3) as such market conditions often give rise to attractive trading opportunities on which global macro managers can potentially capitalize.

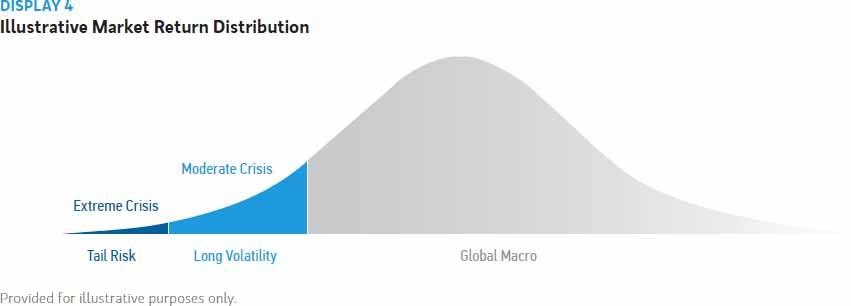

Indeed, certain global macro strategies are designed with the aim of outperforming in precisely these sorts of environments (Display 4). Among the most notable of these are dedicated long volatility and tail risk strategies.

A Closer Look at Long Volatility Strategies

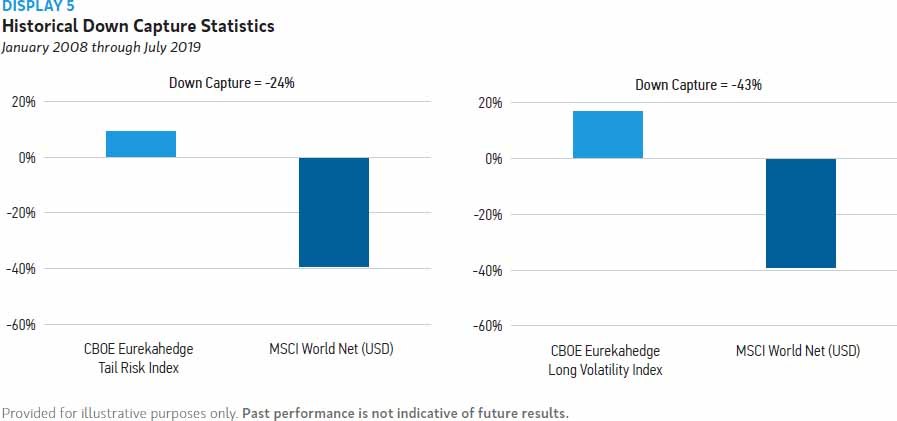

A closer look at the historical performance of long volatility and tail risk strategies reveals dramatic downside risk mitigating characteristics (Display 5).

Long volatility strategies have a high degree of exposure to, or a long bias to, the level of market volatility. They tend to exhibit positive correlation to market volatility and negative correlation to equities over most time horizons. In other words, they are designed to seek to deliver positive returns during periods of market turbulence. Historically, they have delivered.

"Tail risk" strategies comprise a subset of the long volatility universe that exhibits a high degree of convexity, a level of payout that is outsized in comparison to the change in an underlying variable, to large increases in market volatility or declines in equity prices. They are characterized by opportunistic and hedging positions that are intended to deliver positive returns during dramatic market declines. As shown in Display 5, they too have historically proven successful over time.

The Cost

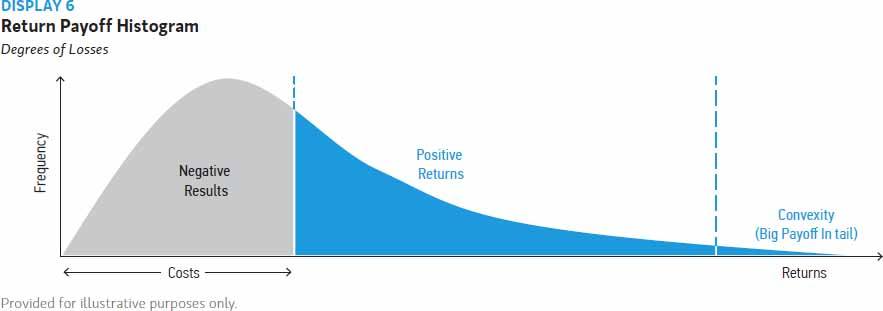

Of course, no investment strategy is without risk or cost. Long volatility strategies tend to be structured with options and other insurance-like products. Options are highly liquid derivative instruments that allow investors to target very specific exposures—for instance, a specific commodity, currency or index— but the cost of holding them in benign markets is not insignificant (Display 6).

Tail-risk strategies tend to be less costly to carry. Benefiting from greater convexity profiles, their potential payoffs can be considerably larger than long volatility exposures. However, those payoffs would only occur during more extreme market conditions.

While the potential benefits of these strategies are clear, it is important to determine the appropriate size of an allocation. Investors will want to be sure that the peace of mind and potential payoff provided by these strategies make sense in the context of associated costs and the portfolio's overall target return and volatility level.

Conclusion

Over time, global macro has demonstrated its ability to perform differently from other asset classes and to weather difficult market conditions, making it, in our opinion, a valuable component of any well-diversified portfolio.1 In addition, we believe that long volatility strategies, including tail risk strategies, have the potential to reduce drawdowns in investor portfolios during volatility shocks and market downturns by seeking to generate positive returns amidst market dislocations.

WealthShield is a division of Emerald Investment Partners, an SEC Registered Investment Advisor. Advisory services are only offered to clients or prospective clients where WealthShield and it’s representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by WealthShield unless a client service agreement is in place. Before investing, consider your investment objectives and WealthShield’s charges and expenses.

Recommended Content

Editors’ Picks

EUR/USD fluctuates near 1.0700 after US data

EUR/USD stays in a consolidation phase at around 1.0700 in the American session on Wednesday. The data from the US showed a strong increase in Durable Goods Orders, supporting the USD and making it difficult for the pair to gain traction.

USD/JPY refreshes 34-year high, attacks 155.00 as intervention risks loom

USD/JPY is renewing a multi-decade high, closing in on 155.00. Traders turn cautious on heightened risks of Japan's FX intervention. Broad US Dollar rebound aids the upside in the major. US Durable Goods data are next on tap.

Gold keeps consolidating ahead of US first-tier figures

Gold finds it difficult to stage a rebound midweek following Monday's sharp decline but manages to hold above $2,300. The benchmark 10-year US Treasury bond yield stays in the green above 4.6% after US data, not allowing the pair to turn north.

Worldcoin looks set for comeback despite Nvidia’s 22% crash Premium

Worldcoin price is in a better position than last week's and shows signs of a potential comeback. This development occurs amid the sharp decline in the valuation of the popular GPU manufacturer Nvidia.

Three fundamentals for the week: US GDP, BoJ and the Fed's favorite inflation gauge stand out Premium

While it is hard to predict when geopolitical news erupts, the level of tension is lower – allowing for key data to have its say. This week's US figures are set to shape the Federal Reserve's decision next week – and the Bank of Japan may struggle to halt the Yen's deterioration.