China trade outperforms amid tech boom and US rebound

China's trade data beat market expectations across the board in May, with shipments to the US seeing a strong base-effect-driven bounce. External demand continues to be one of China's key growth engines this year, but higher imports could cut into the trade surplus going forward.

Exports saw big boost from recovery of exports to US

China's exports rose by 19.3% year-on-year in May (market forecast 15.0%, ING 19.4%), which was up from 14.1% YoY in April. This is in line with our forecast, though stronger than market forecasts. The increase marked a 3-month high, and brought the year-to-date export growth to 15.5% YoY.

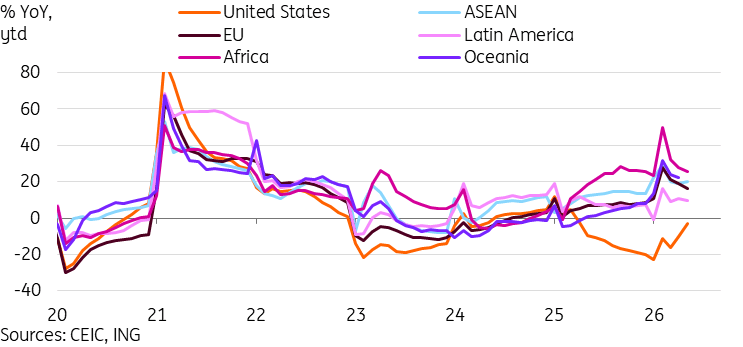

By export destination, the big story for May was a strong rebound of exports to the US, which rose to 35.4% YoY, the highest growth level since 2021. This recovery is primarily a base effect story rather than a reflection of Trump's visit to China. Recall that May 2025 marked the peak of the US-China trade war, when additional tariffs on China surged to 125%. This effect will likely weaken starting with next month's data. We'll start to get a more realistic look at trade in the months ahead under the current tariff environment. The recovery we have seen in the last two months brought year-to-date exports to the US to -2.7% YoY. If we see exports return to positive growth this year, it will remove the biggest drag on China's exports from last year. Tangible trade deliverables looked rather limited after Trump's visit to China. Announcements focused on restoring agricultural purchases to "normal" levels, but moves to establish a trade board and adopt a "constructive strategic stability" approach to bilateral relations could help both sides avoid major trade clashes like last year. There is hope that we'll see further trade breakthroughs before or after President Xi's possible visit to the US in September.

Looking at other areas, exports to South Korea were also very strong (42.1%) as tech trade has accelerated. We also saw strong export growth to ASEAN (24.3%) and Russia (35.8%). The key laggards were exports to the EU (7.6%) and Japan (10.9%).

By export product, the same trends from the past few years continued. China's exports of hi-tech products (50.9%), semiconductors (110.9%), automatic data processing machines (66.0%), mobile phones (44.3%), autos (39.3%), and ships (31.0%) continued to grow strongly in May. Export restrictions may have contributed to the YoY declines observed in March and April. We also saw China's refined petroleum exports rebound to 27.2% YoY in May.

We've written many times that external demand has been a key bright spot for China amid fairly lacklustre domestic activity data. It looks like this gap is widening.

Drag on exports from the US trade war is fading

Tech demand keeps imports strong, with the energy story potentially a factor ahead

Imports rose 27.4% YoY in May (market forecast 26.0%, ING 36.4%), up from 25.3% YoY in April. This came in broadly in line with consensus forecasts but weaker than our forecast.

By import origination, we also saw a recovery in imports from the US (20.4%). The main drivers, though, remain in Asia. Imports from Korea (83.6%), Japan (29.2%), ASEAN (28.2) all outpaced headline import growth in May.

For now, China's import growth remains mainly a tech story rather than an energy story, as evidenced by the surge in imports from Korea. China's hi-tech imports rose 46.8% YoY in May, with semiconductor imports surging 68.0% and automatic data processing machine imports also rising 80.1%.

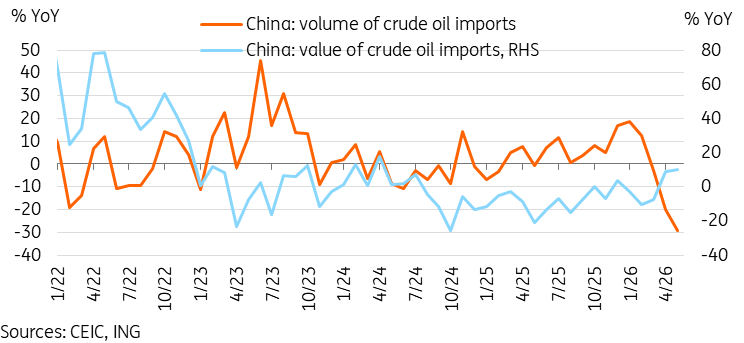

China is the world's largest crude oil importer. How have things changed since the Iran war broke out? Starting with the April data, we've seen import volumes drop sharply, while import values rose modestly due to higher prices. In May, we saw crude oil import volumes drop to -29% YoY while import values rose 10.0% YoY. China's large oil reserves afford it more flexibility to adjust imports strategically. But if no resolution is reached in the Middle East and supply disruptions and higher energy prices persist, it’s reasonable to expect Chinese importers to return to the market at more regular levels. Policymakers would likely be loath to allow strategic reserves to be depleted past a certain point for energy security reasons.

China's slower Oil imports unlikely to last if supply disruptions persist

Trade surplus beat forecasts in May

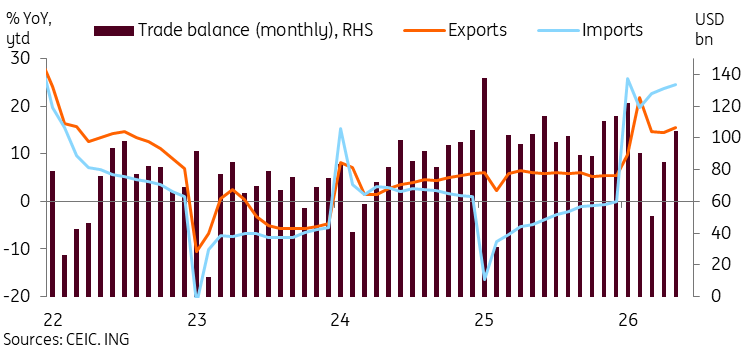

With export growth beating market forecasts by more than imports, we also saw China's May trade surplus beat forecasts at $105.4bn. This marked the highest monthly level since January.

A higher-than-expected surplus could help support growth in 2Q26, but year-to-date the surplus is still down around -3.8% YoY. The strong recovery in imports has offset exports so far this year in the customs data. China continues to run a services trade deficit. China expressed its intention to promote more balanced trade by ramping up imports, cutting tariffs at the start of the year, and strengthening the CNY, which have helped support this effort. China could further ramp up imports, including agricultural imports from the US, and potentially energy imports later in the year.

Could potential tariff hikes on China from the EU derail this stance? Possibly. China has vowed retaliation against discriminatory measures such as tariffs, but as we saw with the US case last year, the friction is likely to remain isolated.

While the trade surplus might not eclipse last year's record $1.18tn this year, the external demand engine remains one of China's key drivers. Domestic demand, though, continues to lag behind. Next week's data will show whether this divide is set to widen.

Trade balance reached a 4-month high in May

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.