![]() Carl R. Tannenbaum

Carl R. Tannenbaum

Northern Trust

I know this must sound terribly old-fashioned, but our family still likes to do jigsaw puzzles. We’ll spread the pieces across a table and dive in, chatting as we go along. The reward is an Irish landscape, or a montage of Walt Disney characters, or a vintage movie poster. There’s nothing like it for low-tech amusement.

Economic discussions in Washington this week centered on a series of puzzles that are confounding the outlook. We have some pieces, but they don’t fit together very well. And we have no idea what image they will ultimately depict once assembled. Following is a series of enigmas that we are presently struggling with.

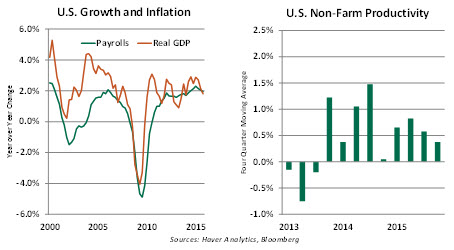

1. Why is job growth so much stronger than economic growth?

U.S. payrolls have grown impressively over the past six months, rising by 1%. Over that same interval, however, U.S. real gross domestic product (GDP) has grown by only 0.7%. There are only a few periods in the last 15 years where job gains have exceeded real GDP gains, leading some to wonder which of the two will have to come back into alignment.

The more favorable reconciliation would be an acceleration of growth. Perhaps the sluggishness of recent quarters is temporary, or maybe GDP has just been understated.

The less-encouraging possibility is that the pace of activity may be slowing, and companies may find themselves overstaffed. If there is a headcount rationalization at hand, it would diminish what has arguably been the brightest theme in the global economic picture.

Whichever interpretation proves true, the juxtaposition of moderate growth and strong employment results suggests that American productivity is very weak. Output per hour declined by 3% in the fourth quarter, one of the worst readings in the last 30 years. Productivity and living standards are closely associated, so this is discouraging result.

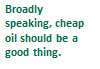

2. Why are oil prices and equity prices moving in tandem?

Petroleum prices have been falling since the middle of 2014, but acutely so since last fall. Of late, daily movements in oil prices have been closely associated with stock market outcomes: if the energy markets are down, equity markets are down. That is not the norm.

It is certainly true that cheap fuel is not good for those companies who produce it. But for a wide range of other industries and for consumers, this should be a boon. If one agrees with this logic, then downward trends in oil prices should be positive for the world’s major equity indexes.

It is certainly true that cheap fuel is not good for those companies who produce it. But for a wide range of other industries and for consumers, this should be a boon. If one agrees with this logic, then downward trends in oil prices should be positive for the world’s major equity indexes.

Attempts to make sense of the situation typically suggest that energy prices reflect perceptions of economic health in emerging markets. Faltering growth, the theory goes, could reduce demand for oil and also create discomfort for world stock markets.

This sounds reasonable on the surface, but unfortunately, it doesn’t seem to square with the data. Global sales of oil increased nicely last year; falling prices are almost certainly due to a supply glut.

Of course, perception is not always deeply rooted in fact. But over time, one might hope that investors realize that low oil prices are broadly beneficial. When that happens, the link that has bound commodities and equity markets together this year will finally break.

3. Can the U.S. expansion survive if manufacturing is in recession?

The world’s heavy industries are struggling to grow and may be in outright decline. As Asha highlighted last week, the U.S. Purchasing Manager’s Index for manufacturing is in contractionary territory. U.S. industrial production has declined for four months in a row.

Major developed economies, though, are heavily service-oriented. In theory (there’s that term again), expansion could continue in these regions even if manufacturing is in retreat. But what we may be missing are linkages between the manufacturing and service sectors that lead them to influence one another. These associations may be fundamental (when attorneys are thriving, they buy more motor vehicles) or psychological. Lighter industries may not be a diversification against heavier ones, and may ultimately get weighted down.

4. Can the U.S. continue forward if others are in retreat?

America isn’t the only country expanding at the moment, but its fortunes and policies do seem to be diverging from many others. Cumulative progress since the end of the last recession has been strongest in the United States, and prospects for the year ahead remain solid (if unspectacular). Reacting to this, the Federal Reserve took a first step away from its zero interest-rate policy last December.

In other markets, sluggish conditions have prompted central banks to go in the opposite direction. Rates that are more negative, larger quantitative easing programs and currency devaluations have all been employed to keep things from slipping further.

In other markets, sluggish conditions have prompted central banks to go in the opposite direction. Rates that are more negative, larger quantitative easing programs and currency devaluations have all been employed to keep things from slipping further.

In the midst of the 1998 Asian financial crisis, Alan Greenspan stated, “It is just not credible that the United States can remain an oasis of prosperity unaffected by a world that is experiencing greatly increased stress.” Fortunately, the knock-on effects were limited back then, and the U.S. economy expanded for a further three years.

Nonetheless, Greenspan’s observation is relevant today. While America is not overly dependent on sales to other regions (exports are only 13% of GDP, low relative to levels seen elsewhere), commerce and capital flows to emerging markets have expanded considerably in the past 18 years. The risk that the former Fed Chair may be right in this instance may cause the current Fed leadership to pause for several months.

The reconciliation of these four apparent misalignments will go a long way toward determining whether 2016 will be a success or a disappointment. We’ll certainly be hoping that they all break the right way.

Today, you can get a jigsaw puzzle app for your mobile phone or tablet which allows you to select from a broad range of images. If I could only figure out how to hard-wire that program to our economic model, we’d have solutions to today’s conundrums in no time.

U.S. Fiscal Challenges: Will the Elephant in the Room Get Noticed?

Polling reports indicate public concern about the “deficit” and “debt” has waned steadily during the past five years. Although the presidential hopefuls have formal fiscal plans, there is scant mention of the federal budget in the election campaign now underway.

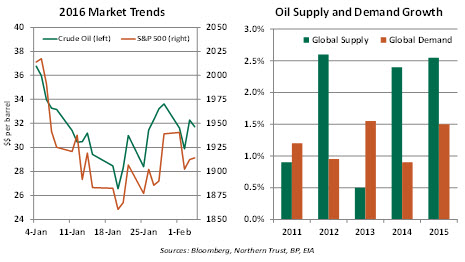

Unfortunately, the latest report from the Congressional Budget Office (CBO) highlights some hard fiscal choices waiting around the corner. At 2.5% of GDP, last year’s deficit was lower than the historical median (2.8%) of the last 50 years. This rosy picture is set to change as the CBO projects the deficit to grow and nearly double as percent of GDP by 2026.

National debt (accumulated borrowing over time) held by the public is projected to rise from $13.1 trillion in 2015 to $23.8 trillion in 10 short years. This sharp increase would put debt as a percent of GDP at 86% a decade from now, up from 74% today. The key here is that debt (numerator) is estimated to grow faster than GDP (the denominator).

Underlying these stark numbers is a growing trajectory of federal government spending and an almost steady trend of revenue as a share of the economy. Aging of the population, health care expenses and interest costs are the well-known culprits behind the upward trend of future federal government spending.

The nearly unchanged trend of revenues reflects offsetting changes in the four main sources of revenue. Individual income tax receipts are projected to move higher, while payroll taxes are estimated to decline, and remittances from the Federal Reserve are expected to drop.

The CBO estimates that revenue from corporate income taxes will fall slightly in 2016 due an extension of expired tax provisions. Looking ahead, an increase in strategies of corporations to reduce their tax liabilities is another reason for a reduction in future tax revenues.

U.S firms pay taxes on worldwide income, unlike many others who pay taxes only on domestic income. One way to get around this is to create or buy a foreign parent to escape worldwide income tax. The Pfizer and Allergen deal and the Johnson Controls and Tyco merger were two of 13 such “inversions” in the last 16 months. For now, there is no Congressional will to change the law to prevent such developments, but this could be an early item of discussion after this November’s elections.

U.S firms pay taxes on worldwide income, unlike many others who pay taxes only on domestic income. One way to get around this is to create or buy a foreign parent to escape worldwide income tax. The Pfizer and Allergen deal and the Johnson Controls and Tyco merger were two of 13 such “inversions” in the last 16 months. For now, there is no Congressional will to change the law to prevent such developments, but this could be an early item of discussion after this November’s elections.

The CBO’s baseline projections assume “existing” laws remain in place. The recent tax-extender package passed in December 2015 altered existing laws and added $680 billion to deficits. If such actions are taken in the years ahead, the current baseline forecast is inaccurate.

Like voters, investors don’t seem overly troubled by any of this. Despite the dire deficit outlook shared by the CBO, U.S. Treasury yields remain close to generational lows and auctions are well- subscribed.

Without pressure from the markets, policymakers are unlikely to display any urgency. But a lack of political will to lower spending and raise revenues will be costly in the long run. After the balloting is over, let’s hope Congress gets serious about the budget.

January’s Job Report Does Not Disappoint

After five weeks of disappointing market outcomes, the world could use some good news. While it may not be obvious on the surface, the January U.S. job report could provide a lift to flagging financial spirits.

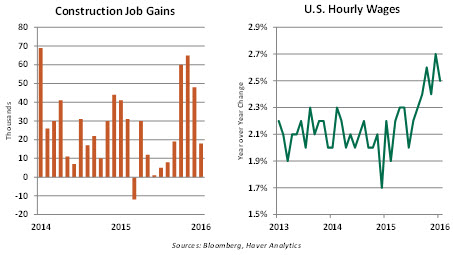

Establishments added 151,000 jobs last month. The gains are smaller than we had seen in recent reports, but construction payrolls grew by 30,000 less in January than they did in December. This is attributable to mild weather in December, which likely confused the seasonal adjustments applied to the sector. Adjusting for this, January’s progress is closer to December’s.

Establishments added 151,000 jobs last month. The gains are smaller than we had seen in recent reports, but construction payrolls grew by 30,000 less in January than they did in December. This is attributable to mild weather in December, which likely confused the seasonal adjustments applied to the sector. Adjusting for this, January’s progress is closer to December’s.

Further, U.S. retirement trends suggest that it only takes payroll gains of 80,000 per month to keep the unemployment rate stable. Our conception of what constitutes a “good” job report needs to factor this in. By that measure, January’s outcome is hardly disappointing.

Wages are a clear highlight of today’s report. Stuck in the 2% range for several years, gains have been improving steadily since the middle of last year. More pay means more consumption, which supports continued expansion. And rising labor costs provide the Fed an increment of additional confidence that their 2% inflation target can be reached in the medium term.

The unemployment rate dipped below 5% for the first time since early 2008. The household survey showed very strong employment gains and rising labor force participation, which is the desired combination.

Today’s update does not likely change the likely trajectory of U.S. monetary policy. International uncertainty has clouded the outlook and taken a March interest-rate increase off the table. But continued gains in jobs and wages should reduce the likelihood of a worst-case outcome and allow the Federal Reserve to continue normalizing conditions later this year.

The information herein is based on sources which The Northern Trust Company believes to be reliable, but we cannot warrant its accuracy or completeness. Such information is subject to change and is not intended to influence your investment decisions.

Recommended Content

Editors’ Picks

EUR/USD clings to daily gains above 1.0650

EUR/USD gained traction and turned positive on the day above 1.0650. The improvement seen in risk mood following the earlier flight to safety weighs on the US Dollar ahead of the weekend and helps the pair push higher.

GBP/USD recovers toward 1.2450 after UK Retail Sales data

GBP/USD reversed its direction and advanced to the 1.2450 area after touching a fresh multi-month low below 1.2400 in the Asian session. The positive shift seen in risk mood on easing fears over a deepening Iran-Israel conflict supports the pair.

Gold holds steady at around $2,380 following earlier spike

Gold stabilized near $2,380 after spiking above $2,400 with the immediate reaction to reports of Israel striking Iran. Meanwhile, the pullback seen in the US Treasury bond yields helps XAU/USD hold its ground.

Bitcoin Weekly Forecast: BTC post-halving rally could be partially priced in Premium

Bitcoin price shows no signs of directional bias while it holds above $60,000. The fourth BTC halving is partially priced in, according to Deutsche Bank’s research.

Week ahead – US GDP and BoJ decision on top of next week’s agenda

US GDP, core PCE and PMIs the next tests for the Dollar. Investors await BoJ for guidance about next rate hike. EU and UK PMIs, as well as Australian CPIs also on tap.