![]() Carl R. Tannenbaum

Carl R. Tannenbaum

Northern Trust

Last weekend, I cooked Thanksgiving dinner for “The Supper Club,” a group of friends in Melbourne that allows me to join with them once a year for good food, good wine and good conversation. Club members were sent on a veritable scavenger hunt for all the traditional ingredients, many of which are not readily available Down Under. The most common form of pumpkin is actually blue on the outside, and special arrangements were needed to secure a turkey.

The group was bemused by my coddling of the bird: an overnight bath in brine, followed by the addition of performance-enhancing substances with a poultry injector. After a backrub of fresh herbs and olive oil, our formerly feathered friend was basted lovingly until reaching an internal temperature of 74°C. Tender and juicy every time.

The food turned out great, but what my friends enjoyed most were the stories about the holiday, including my mother’s lament that I ruined her Thanksgiving the year I was born. I announced my readiness to arrive after she had put the holiday dinner in the oven. “I knew from the start that he’d be a real turkey,” she’s fond of saying.

The business side of the visit included more than 20 conversations with financial managers and partners. Some interesting themes emerged, some of which have relevance far beyond the antipodes.

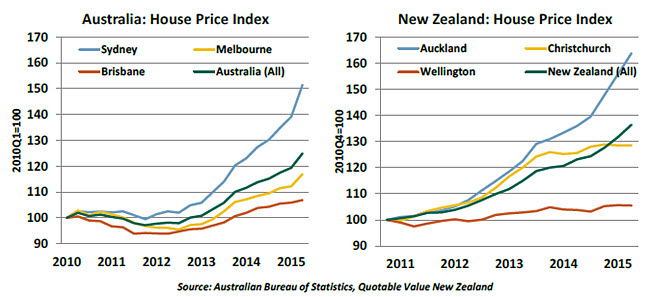

- The arc traced by Australian and New Zealand home prices is a source of broad concern. Property values in Sydney, in particular, have risen by 50% over the past 5 years. Observers from near and far fret that the line between fair value and market excess was crossed some time ago.

Low interest rates are among the many contributors to the property price escalation. The central banks in both Australia and New Zealand have not brought rates all the way down to zero, but they stand near historic lows in both places. These steps were taken to stimulate economic activity and to improve terms of trade by reducing the value of the Aussie and New Zealand dollars.

Low rates make leverage less expensive, and they prompt asset reallocation from bonds to riskier sectors. These elements can be the foundation for market excess. To combat this, Australian bank regulators have raised capital requirements on mortgages and mandated higher down payments. But as is the case with many major world cities, the marginal buyer of property is foreign (often Chinese) and paying cash. The only way to curtail this latter source of demand is through the tax system.  Collectively, these ingredients form what we have come to know as “macroprudential” policies. The effectiveness of these measures relies on close coordination among the central bank, financial supervisors and the legislature. This can sometimes be difficult to secure, especially when legislators are lobbied by construction firms noting the benefits that building has on employment.

Collectively, these ingredients form what we have come to know as “macroprudential” policies. The effectiveness of these measures relies on close coordination among the central bank, financial supervisors and the legislature. This can sometimes be difficult to secure, especially when legislators are lobbied by construction firms noting the benefits that building has on employment.

The longer that developed countries keep interest rates at zero, the more likely it is that bubbles could form. Piercing them gradually is a delicate operation, one that has never been performed successfully. The world will be watching the dynamic in Australia and New Zealand closely, as other countries may soon have to travel a similar path to arrest increases in property prices.

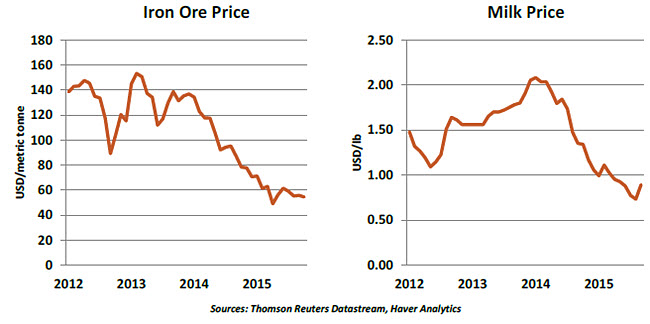

- Concern over China is felt more acutely in Australia and New Zealand, both of which rely on trade with China to a much greater degree than Europe and the United States. In Australia, the mining sector in the western part of the country has slowed considerably, while falling milk prices have impaired New Zealand’s dairy sector.

Both economies remain heavily service-driven, and both rely substantially on domestic consumption. So there is a considerable buffer of economic activity that is not dependent on trade. But both countries have worked hard to tie their economies more with the Pacific Rim and somewhat less with the Commonwealth; recent experience illustrates the downside of that new association.

Like other observers, portfolio managers in the subcontinent are struggling to understand how slow China might be. The data suggest that Chinese heavy industry could be receding at the moment; global demand is soft, and China has plenty of competition from its manufacturing neighbors. In addition, the Chinese currency has strengthened over the past year, as authorities there maintain something of a peg against the U.S. dollar. This puts China’s exports at a disadvantage.

As we discussed a few weeks ago, the Chinese service sector will have to take up the slack. Official statistics suggest strong growth on that side, but external observers remain somewhat skeptical. If Chinese growth is much slower than they are letting on, that would be very bad news for emerging and developed markets alike. This remains the top global economic risk going into 2016.

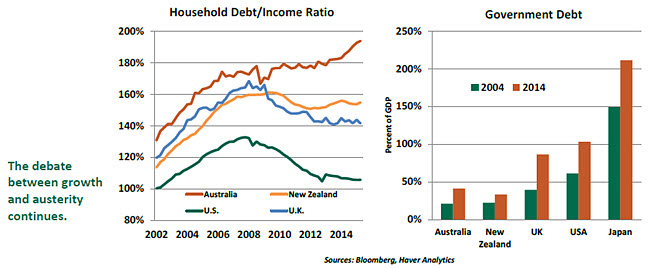

- Australia and New Zealand are both fretting over the debt they have accumulated over the past decade. Ratios of household borrowing to household income in the two countries are among the highest in the world. While it is sometimes difficult to compare these measures across markets (calculation methods are not entirely uniform), the trend remains worrisome.

Government debt ratios have also grown in Australia and New Zealand over the past decade, but levels are nowhere near those of other major developed nations.

The anxiety over leverage has led to calls for spending restraint at home and in parliament. But belt-tightening at either level would almost certainly impair economic growth, which would diminish national income and make debt more difficult to service. And the lack of fiscal stimulus places pressure on central banks to adopt monetary policy that is unnaturally accommodative.

Since the financial crisis, many nations have struggled to balance growth with austerity. Most have adopted a half-way solution that has limited the growth of both the economy and of debt. If taken too far, though, austerity can have detrimental impacts on debt.

Australia has been a bit of a charmed nation, at least economically. It has not had a recession since the early 1990s. But observers there are fretting that this long winning streak may be at risk in the coming years, and they are concerned about how businesses and policymakers will respond. If there is a silver lining for nations that experience more regular turns of the business cycle, it is that they have deeper experience managing through boom and bust. Australia lacks that perspective and may be at risk of overreacting when the time comes.

- Visitors to major cities in Australia and New Zealand quickly notice how diverse they are. There are faces from all over the world, and (much to my delight) cuisines from all over the world. When you combine the great local ingredients with international tastes, you have outstanding restaurants.

The diversity has a broader benefit, which is economic vitality. Population growth in Australia and New Zealand is among the best in the developed world, giving them demographic profiles that are favorable. As we have discussed, young cultures innovate more, take more risks and provide balance to pension and health systems.

The diversity has a broader benefit, which is economic vitality. Population growth in Australia and New Zealand is among the best in the developed world, giving them demographic profiles that are favorable. As we have discussed, young cultures innovate more, take more risks and provide balance to pension and health systems.

Immigration has been a very significant theme in 2015, and the awful attacks in Paris will make the issue an even tougher one in 2016. That said, countries that are good at welcoming and assimilating newcomers will be favored with better economic performance over time.

It is a true pity that I only visit Australia and New Zealand once per year. The people are bright and engaging, and both places are absolutely beautiful. I’ll look forward to next year’s journey; The Supper Club is already at work on the menu.

The Emerging Market Debt Challenge

The International Monetary Fund projects stronger business momentum in emerging markets (EMs) during 2016. The positive outlook appears optimistic, as EMs have accumulated a significant amount of non-financial sector debt in recent years. It is widely accepted that rapid debt accumulation relative to gross domestic product (GDP) is unfavorable for economic growth.

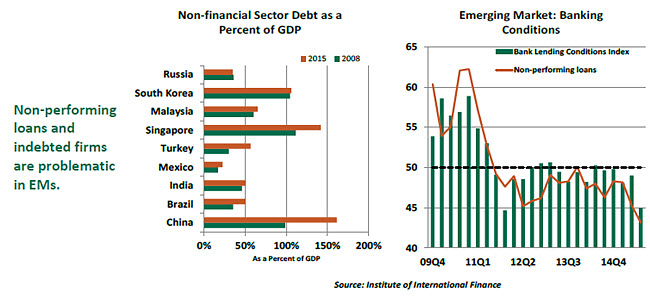

Total world debt has grown by about $50 trillion since 2009, inclusive of a larger increase in emerging market debt ($28 trillion) compared with mature economies. Breaking down debt by sectors (household, financial, non-financial and government), growth in non-financial sector debt is the main driver in EMs, while government debt tops the list in advanced economies. Household and non-financial sector debt as a percent of GDP in EMs has increased since the Global Financial Crisis (GFC) but declined in advanced economies.

The quantitative easing programs of major central banks are viewed as the root cause of the recent debt dynamic in EMs. The search for yield guided funds to EMs as interest rates plunged in the rich economies. Banks and companies in EMs have been the recipients of this reallocation.

To put these funds to use, banks and shadow banks extended loans to companies in EMs to fund projects such as steel mills, cement factories, bridges, mines and so forth. Consequently, it helped to boost business activity in EMs to the extent that growth was stronger than in advanced economies following the GFC.

The key is whether banks in EMs can sustain these lending programs. In this regard, the Institute of International Finance’s quarterly survey of bank lending conditions covering 119 EM banks is a useful guide. The latest survey indicates that bank lending conditions in the third quarter of 2015 tightened to the level last seen in the fourth quarter of 2011, when the eurozone debt crisis was unfolding. An index reading of 50 is neutral. Values below 50 indicate a tightening of bank lending conditions and vice versa. For non-performing loans, readings below 50 indicate an increase in non-performing loans and vice versa.

The index measuring loan demand dropped the most, and non-performing loans registered the largest increase since the survey began in 2009. All regions experienced tightening of bank lending conditions, with indexes representing EM Asia, Latin America and MENA showing the relatively more-severe tightening of lending conditions.

The growth of non-financial corporate debt in EMs promotes investment. However, the leveraged firms may be unable to service the debt if they are experiencing losses. Research indicates profits of EM firms are suffering. Political pressure in EMs can prevent banks from taking a tough stance toward firms incapable of meeting debt obligations, as shutting down delinquent firms will result in job losses. In other words, indebted and underperforming firms can unleash a chain of events that will ultimately trim overall growth.

As we have written in earlier commentaries, all EMs are not equal; the likely pain from a debt overhang will vary. In general, as the U.S. dollar strengthens, EM companies that have issued foreign currency bonds will have difficulty servicing leverage. EMs with large coffers, such as Singapore and China, can put out fires even though debt has piled up in these economies.

Corporate leverage in India has advanced at a gradual pace in the last seven years, but an IMF report indicates that 37% of corporate debt is “at risk.” Corporate debt in Turkey, Brazil, and Mexico has risen considerably since 2008. Malaysia’s problem is not corporate debt, but it has the largest household debt-to-GDP ratio (70%) among large EMs.

The size of EMs in the global economy exceeds that of mature economies. The knock-on effects on advanced economies can be large if growth suffers in EMs. It will serve investors well to examine the debt trajectory of EMs when evaluating the prospects of these economies. Debt is deceptive because the damage reveals itself only after the house of debt crumbles.

The information herein is based on sources which The Northern Trust Company believes to be reliable, but we cannot warrant its accuracy or completeness. Such information is subject to change and is not intended to influence your investment decisions.

Recommended Content

Editors’ Picks

EUR/USD clings to modest gains above 1.0650 ahead of US data

EUR/USD trades modestly higher on the day above 1.0650 in the early American session on Tuesday. The upbeat PMI reports from the Eurozone and Germany support the Euro as market focus shift to US PMI data.

GBP/USD extends rebound, tests 1.2400

GBP/USD preserves its recovery momentum and trades near 1.2400 in the second half of the day on Tuesday. The data from the UK showed that the private sector continued to grow at an accelerating pace in April, helping Pound Sterling gather strength against its rivals.

Gold flirts with $2,300 amid receding safe-haven demand

Gold (XAU/USD) remains under heavy selling pressure for the second straight day on Tuesday and languishes near its lowest level in over two weeks, around the $2,300 mark in the European session. Eyes on US PMI data.

Here’s why Ondo price hit new ATH amid bearish market outlook Premium

Ondo price shows no signs of slowing down after setting up an all-time high (ATH) at $1.05 on March 31. This development is likely to be followed by a correction and ATH but not necessarily in that order.

US S&P Global PMIs Preview: Economic expansion set to keep momentum in April

S&P Global Manufacturing PMI and Services PMI are both expected to come in at 52 in April’s flash estimate, highlighting an ongoing expansion in the private sector’s economic activity.