![]() Carl R. Tannenbaum

Carl R. Tannenbaum

Northern Trust

Since 2008, Europe has lurched from one crisis to another. One country emerged as the figurehead for Europe during this time, leading international discussions and fighting to keep the single currency area united. But with popular support for the European project falling, Germany and its leader Angela Merkel face an ever-increasing burden as de-facto leaders of the continent.

France and Germany have historically been the pillars of the region. Part of this was due to events of the early 1900s. In order to avoid further tensions leading to another war, it was decided the best course of action was to align the countries’ interests economically, through trade deals that ultimately became the European Union (EU), and militarily through NATO.

Since its first unification in 1871, Germany has been the most dynamic economy in Europe, with a strong manufacturing and export sector. Post World War II, the Germans led the way economically but, for obvious reasons, had less say in foreign-policy issues. As the EU has evolved, Germany proved adept at both (whether by design or accident) and under the reins of Chancellor Merkel is now indisputably the continent’s powerhouse on whom others rely to lead the way.

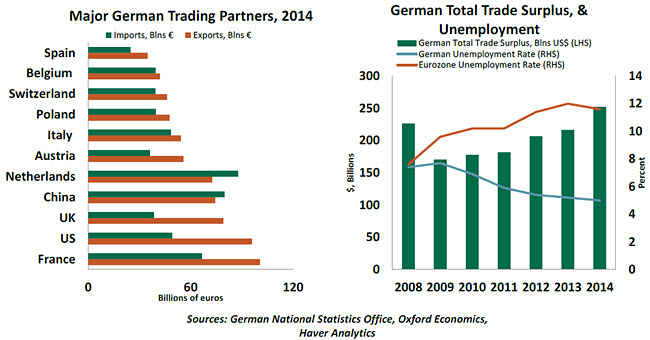

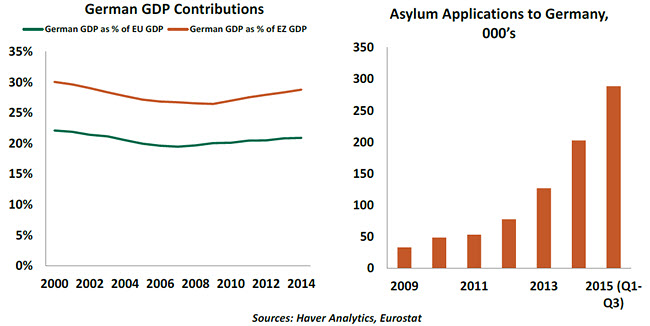

Germany’s economic importance to the bloc is huge, but the country also relies on fellow Europeans. Germany is the biggest economy and single largest exporter in Europe, running a sizeable current account and trade surplus. One of its main criticisms, however, is that it relies too heavily on external demand to ensure full employment at home. Promoting domestic consumption through imports could boost the fortunes of its neighbors. Indeed, unemployment rates in Germany are more than half the level of the eurozone (4.5% versus 10.8%). Despite this, German output contributes 21% to total EU gross domestic product – a sizeable chunk. Additionally, its manufacturing exports are key links in the production chain for many other countries. German attitudes toward fiscal responsibility, for better or worse, shaped responses to the European debt crisis and fashioned the spending restraints on numerous countries. The reach of influence is truly continent-wide.  Under Merkel’s stewardship, Germany now leads the way on the policy front, too. The Russia-Ukraine crisis is a case in point. Merkel led talks with Vladimir Putin and successfully persuaded other nations to impose economic sanctions against the Kremlin. During the various Greek episodes, she led bailout and reform negotiations. Most recently, she has stuck out her neck and been the most vocal leader on the refugee crisis, vociferously protecting the EU’s “free movement of people” principle and reinforcing the message that Europe has an obligation to help those fleeing conflict zones.

Under Merkel’s stewardship, Germany now leads the way on the policy front, too. The Russia-Ukraine crisis is a case in point. Merkel led talks with Vladimir Putin and successfully persuaded other nations to impose economic sanctions against the Kremlin. During the various Greek episodes, she led bailout and reform negotiations. Most recently, she has stuck out her neck and been the most vocal leader on the refugee crisis, vociferously protecting the EU’s “free movement of people” principle and reinforcing the message that Europe has an obligation to help those fleeing conflict zones.

True, Merkel is probably the only leader with the ability to put herself on the line. She does not yet face the same degree of rising populism and for historical reasons is probably the most likely candidate willing to take that stand.

It is, however, this latest crisis facing Europe that could prove to be Merkel’s Achilles heel. Her perceived open-door migrant policy angered the public and politicians at home, not to mention elsewhere, despite the fact that the flow of people would almost certainly have come anyway. Merkel’s popularity has fallen, causing speculation about her future.

Economically, Germany is also facing challenges. Troubles in emerging markets, where 29% of German exports go, are reducing demand. Exports fell in August by the most on a monthly basis since 2009; manufacturing orders from outside the eurozone fell by 13% in July and August; and industrial production contracted 1.1% in September. Slowing demand from China, where 6.6% of exports go, is a source of concern. Coupled with souring sentiment toward the migrant issue, there is a risk of rising nationalism. Indeed, in recent weeks Merkel’s migration stance has toughened, probably an attempt to appease anti-immigrant voters’ concerns.

What would happen to Europe if both issues escalated, jeopardizing Germany’s dominant position? Merkel’s coalition partner, the Christian Social Union Party, is anti-immigration, so shifting public sentiment could benefit them in the longer term. Some may start calling for a greater degree of separation from the EU, as those in the United Kingdom have done and which could threaten European unity. If German growth slows drastically, European growth would certainly suffer, although by how much cannot be certain. A greater concern might be the loss of confidence across the continent should perceptions spread that the linchpin is in trouble.  However, for now the risk of a dramatic shift is limited. The majority of Germans are overwhelmingly in favor of EU and eurozone membership and realize the importance the union holds for their economy, jobs and well-being. Nationalistic swings should be minimal, and it is anticipated that political leaders will continue working to keep the eurozone together. Economically, the Chinese slowdown may not be enough on its own to seriously dampen potential growth in Germany. And it should be offset by continued signs of strength in the United States, United Kingdom and rest of the eurozone, which together account for 48.6% of exports.

However, for now the risk of a dramatic shift is limited. The majority of Germans are overwhelmingly in favor of EU and eurozone membership and realize the importance the union holds for their economy, jobs and well-being. Nationalistic swings should be minimal, and it is anticipated that political leaders will continue working to keep the eurozone together. Economically, the Chinese slowdown may not be enough on its own to seriously dampen potential growth in Germany. And it should be offset by continued signs of strength in the United States, United Kingdom and rest of the eurozone, which together account for 48.6% of exports.

Additionally, Merkel has few political opponents. Recent polls suggest 82% of her party approve of her leadership and 81% would like her to run again in 2017. Merkel knows how important her position in Europe has become. If she were to go, who would fill the void? It is hard to pick a potential individual (let alone a country) who could be as effective. Let’s just hope she stays the course.

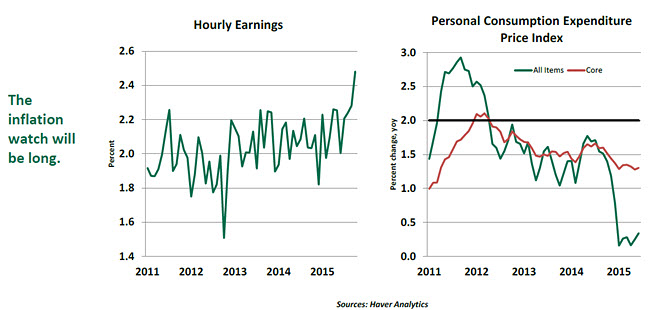

Does Wage Acceleration Lead to Higher Inflation?

The Federal Reserve’s performance is measured by whether it has fulfilled the dual mandate of full employment and price stability. After nearly seven years of growth, there is good news as labor market indicators point to significant progress in satisfying the full-employment mandate. But inflation is stuck stubbornly below the Fed’s target. Markets are looking for indicators that will provide clues about future inflation. The information content of wage trends was useful in the past to assess the likely trend of inflation. However, recent experience points to a transformed landscape.

Employment compensation has been subdued for an extended period. Hourly earnings, the Employment Compensation Index and other wage measures have hovered at low levels. The downward trend of the unemployment rate raised expectations of higher wage gains, but actual data failed to validate it until the latest employment report.

The 2.5% jump in hourly earnings during October, the largest increase since 2009, was the prominent news in this report. In mature expansions, wages typically show year-to-year increases of around 3.5%. Although the October increase in hourly earnings is only one data point, the logical question is if an acceleration of wage growth will translate into higher inflation in the near term.

Intuitively speaking, the link between wages and inflation is understandable as labor costs, on average, account for two-thirds of total production costs. Economic theory notes that an increase in labor costs that exceeds productivity gains should exert upward pressure on prices.  In the past, higher wage growth led to price increases. There is a large body of empirical literature that examines how useful wage inflation is for predicting higher prices. Research shows that the pass through of labor costs to inflation was meaningful until the early 1980s.

In the past, higher wage growth led to price increases. There is a large body of empirical literature that examines how useful wage inflation is for predicting higher prices. Research shows that the pass through of labor costs to inflation was meaningful until the early 1980s.

Fast forwarding to the present time, the main conclusion of studies is that wages do not offer significant information about future price movements.

There are reasons for this change. Nominal wages are rigid in a low-inflation environment. Firms do not cut nominal wages but expect inflation to do the job of reducing real wages. In a low-inflation environment, pent-up wage reductions have held back wage growth. Under these circumstances the explanatory power of wages in the inflation process is diminished.

Another line of research notes that an anchoring of inflation expectations has led to nearly constant long-run levels of not only inflation but also labor costs. Inflation in the United States averaged 2.5% during the 20 years ended 2005, down about 200 basis points from the previous 20-year period. Increased credibility of monetary policy management has resulted in the public anchoring inflation expectations.

Fed Chair Janet Yellen’s September 25, 2015, speech about inflation dynamics notes that the so-called wage-price spiral is no longer a good representation of the inflation process in the United States.

These findings do not suggest that wage trends are no longer a source of useful information. Wage growth is a reliable indicator of labor market slack. Therefore, actual movements in employment compensation are a solid indicator of how far or how close the economy is from full employment.

Demand growth, a stability of energy prices and higher commodity prices will help the Fed’s mission to reach the inflation target. At present, low global demand is restraining global inflation. For the Fed to be “reasonably confident” that inflation will return to 2.0% in the quarters ahead, solid economic growth is the key.

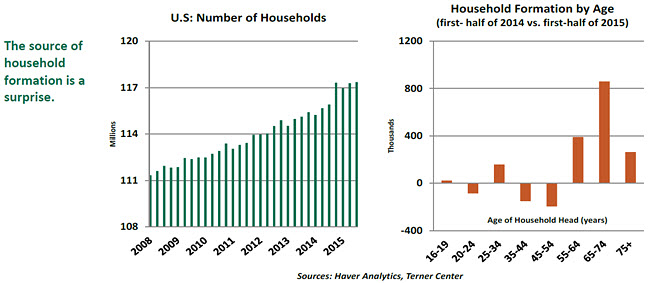

Household Formation Could Spur Housing Activity

There are various factors that influence the pace of housing market activity. Household formation is one of the important drivers, in addition to employment conditions, credit availability, mortgage rates and home prices. The Great Recession’s impact held back the rate of household formation long after its end. Of late, the number of households is increasing, and that should have a positive influence on housing market conditions.

The latest census tally shows there are 117.3 million households in the United States, up from 2014. Methodological changes gave a boost to the count of households at the end of 2014. Even after discounting for this adjustment, there is a visible increase in household formation.

Young adults moving out of parents’ homes and forming new households is usually expected to lift household formation. Surprisingly, research shows that baby boomers are driving the increase in household formation. The contribution of young adults is mixed.

Aging of the U.S. population and the fact that older adults live in smaller households than younger adults results in a larger number of households at the older age group. The small increase in household formation among 25-34 year-olds is due to an increase in population, while the fact that more young adults are living with parents offsets a part of the population impact.

The net increase in household formation is a plus for the home construction industry, irrespective of the age group where it is occurring. Employment prospects have vastly improved, inclusive of a significantly higher employment-population ratio for 25-54 year-olds. Surveys show that millennials, projected to be the largest cohort that will soon surpass baby boomers, do cherish the dream of homeownership, albeit a smaller percentage than one would expect.

The type of homes that will be constructed will be driven by the cohort forming new households. There is more of the housing market recovery in store.

The information herein is based on sources which The Northern Trust Company believes to be reliable, but we cannot warrant its accuracy or completeness. Such information is subject to change and is not intended to influence your investment decisions.

Recommended Content

Editors’ Picks

EUR/USD clings to daily gains above 1.0650

EUR/USD gained traction and turned positive on the day above 1.0650. The improvement seen in risk mood following the earlier flight to safety weighs on the US Dollar ahead of the weekend and helps the pair push higher.

GBP/USD recovers toward 1.2450 after UK Retail Sales data

GBP/USD reversed its direction and advanced to the 1.2450 area after touching a fresh multi-month low below 1.2400 in the Asian session. The positive shift seen in risk mood on easing fears over a deepening Iran-Israel conflict supports the pair.

Gold holds steady at around $2,380 following earlier spike

Gold stabilized near $2,380 after spiking above $2,400 with the immediate reaction to reports of Israel striking Iran. Meanwhile, the pullback seen in the US Treasury bond yields helps XAU/USD hold its ground.

Bitcoin Weekly Forecast: BTC post-halving rally could be partially priced in Premium

Bitcoin price shows no signs of directional bias while it holds above $60,000. The fourth BTC halving is partially priced in, according to Deutsche Bank’s research.

Week ahead – US GDP and BoJ decision on top of next week’s agenda

US GDP, core PCE and PMIs the next tests for the Dollar. Investors await BoJ for guidance about next rate hike. EU and UK PMIs, as well as Australian CPIs also on tap.