![]() Carl R. Tannenbaum

Carl R. Tannenbaum

Northern Trust

I look forward to the change of seasons. Yes, it’s a little chillier, but that beats sweating through your suit during the morning commute. Grilling winds down, but “slow-food” season rises in compensation. My daughter is refusing to rake the fallen leaves, but I no longer have to worry about her refusal to mow the grass.

There is one aspect of the seasonal transition that fills many of us with dread, and that is the onset of a new U.S. federal fiscal year each October 1. The budget battles that rage at this point on the calendar illustrate the myopia and dysfunction of the American legislative process. This year’s wrangling has been heightened by the resignation of House Speaker John Boehner, the beginning of next year’s election campaign and the upcoming need to raise the federal debt ceiling.

Late Wednesday evening, Congress passed legislation that will keep the government running through mid-December. But battle lines are being drawn for the next round of debate, which will commence as that date approaches. The struggle of lawmakers to concur on modest proposals suggests that more-significant issues will not be addressed. And failure to think beyond the next election cycle may be very costly to the country in the long term.

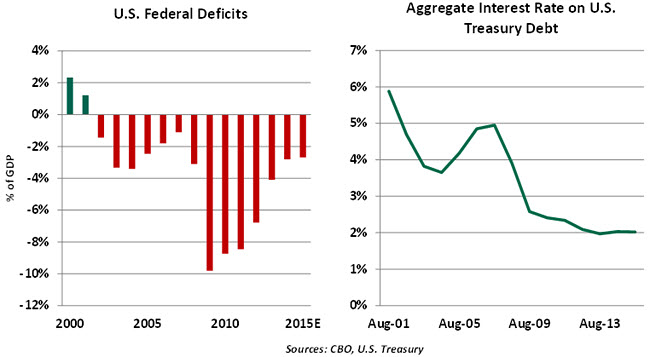

One irony surrounding this year’s budget tension is that discussions are occurring against a strong backdrop. The American fiscal position has improved quite a bit over the past five years, as solid economic growth and spending restraints have combined to bring the annual deficit down to just 2.4% of gross domestic product (GDP). Despite debt that is at twice the level of GDP as it was just seven years ago, the cost of carrying that debt has continued to decline.

Instead of pursing broad strategies to extend recent success, lawmakers have focused on two items that have small costs but cast large shadows. One is Planned Parenthood, which gets about $60 million per year in discretionary funding from the federal budget and another $390 million from “mandatory” programs like Medicaid. There are certainly political issues surrounding the program, but its total cost is an infinitesimal part of the $3.5 trillion that the federal government spends annually.

The second is the Export-Import (Ex-Im) Bank, an 80- year-old agency that supports the export of U.S. goods and services. Congress declined to reauthorize the Ex-Im Bank last June, which prevents the agency from entering new deals. Opponents of the Bank suggest that the services it offers can be provided by the private sector, while proponents note that 60 foreign countries have similar agencies to promote export competitiveness. At an annual tab of about $1 billion, though, the Ex-Im Bank is also a very small part of a very large budget.  Of far greater significance in the near term is the trajectory of defense spending, which has been held in check by sequestration. As the world becomes a more unsettled place, there seems to be bipartisan support for additional funding in this area. On the domestic front, there is broad support for additional investments in infrastructure, as embodied by the need to replenish the Highway Trust Fund.

Of far greater significance in the near term is the trajectory of defense spending, which has been held in check by sequestration. As the world becomes a more unsettled place, there seems to be bipartisan support for additional funding in this area. On the domestic front, there is broad support for additional investments in infrastructure, as embodied by the need to replenish the Highway Trust Fund.

Even if spending authorizations are not increased, the U.S. Treasury is likely to run into its debt ceiling sometime late this year. Whatever one thinks about the appropriate level or composition of federal spending, the debt ceiling is an awkward device. The United States is the only major developed country to have such a limit; in passing appropriations that are in excess of tax revenue, the Congress is implicitly endorsing the need for additional borrowing. The debt ceiling has been raised 14 times in the past 15 years, so it hasn’t been much of a constraint.

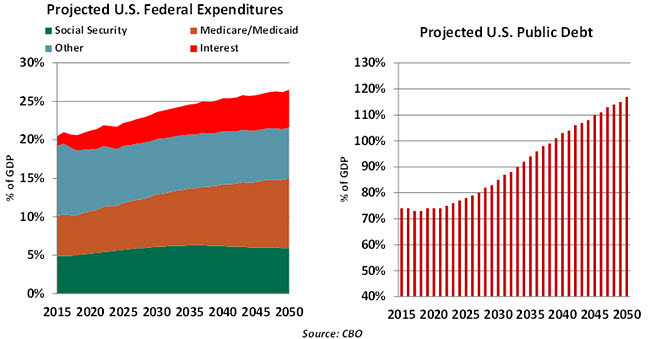

And all of this ignores the elephant in the room, which are the long-term spending obligations that promise to bust the U.S. budget if not addressed soon. The costs of Social Security and Medicare are projected to march ahead mercilessly in the coming decades, placing a significant burden on federal finances.

The continuing resolution passed this week will run out at about the same time as the debt ceiling will become binding, creating high stress right around the holidays. (Not to mention the critical Federal Reserve meeting on December 15 - 16.)

Members of Congress will be preparing for the primary election season, which begins early next year. Candidates from both parties tend to lean a little more to the extremes during that phase, and staking out a strong position on budget levels and priorities may make a mark with primary voters. That does not bode well for reaching resolution.  On the other hand, frustration with Washington is already at a high level. Another impasse may reflect negatively on those hoping for a renewal of the public trust. The electorate must realize that the short-term motivations of getting re-elected are at odds with solving the long-term issues surrounding the U.S. budget. That mismatch of time horizons is potentially very costly.

On the other hand, frustration with Washington is already at a high level. Another impasse may reflect negatively on those hoping for a renewal of the public trust. The electorate must realize that the short-term motivations of getting re-elected are at odds with solving the long-term issues surrounding the U.S. budget. That mismatch of time horizons is potentially very costly.

Some have postulated that John Boehner’s meeting with the pope during the pontiff’s recent visit to Washington may have contributed to his decision to retire. There are higher purposes we should aspire to, and higher authorities to answer to. But if the rest of the Congress doesn’t get fiscal religion soon, our country could be risking time in purgatory.

How Far Will Brazil Fall?

Brazil has been making headlines lately for all the wrong reasons. Last month, Standard and Poor’s downgraded the sovereign’s bond rating to junk status. As doubts over local politics and global demand grew last week, the Brazilian real depreciated to its all-time weakest against the dollar, bond yields spiked and local equities declined. Despite a modest currency rally caused by the threat of increased foreign exchange intervention from the Banco Central do Brasil (BCB), the central bank, the Latin American giant is hardly out of the woods. According to the latest polls, analysts expect the economy to contract some 2.5% in 2015 and another 0.5% - 1.0% in 2016. Rising unemployment will add to the frustration in the streets.

Furthermore, political risks are likely underestimated and add a large downside to the economic outlook. President Dilma Rousseff’s approval ratings remain in the single digits, and her lack of sway in Congress threatens to derail much-needed fiscal reform. The ongoing Lava Jato corruption probe, yet to directly implicate Rousseff, could give legal grounds for the president’s impeachment. Recent investigations into former President Luiz Ignacio “Lula” da Silva, Rousseff’s mentor and former boss, are not a good sign.

Yet a change in leadership in the Planalto presidential palace would usher in a period of greater political instability, with fierce opposition from far-left factions of Rousseff’s Workers Party. Increased uncertainty and policy gridlock would prolong the economic malaise.

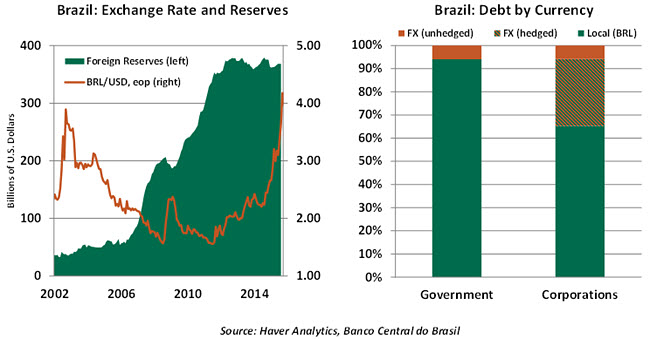

For now, Brazil’s external liquidity profile provides a floor to such an economic free-fall scenario. Over the past decade, foreign exchange reserves have ballooned to $368 billion, equivalent to 17% of GDP and more than five times the level in 2005. In a scenario where Brazil loses complete access to international financing, these international reserves would theoretically be enough to pay down the entirety of the country’s $350 billion external debt.

In addition, the country’s debt composition is quite favorable, with minimal direct foreign exchange exposure. Foreign currency debt accounts for just 6% of government obligations, the lowest in Latin America and among the lowest of all emerging markets. This is a major improvement from 2000, when 25% of public sector debt was denominated in foreign currency.

In addition, the country’s debt composition is quite favorable, with minimal direct foreign exchange exposure. Foreign currency debt accounts for just 6% of government obligations, the lowest in Latin America and among the lowest of all emerging markets. This is a major improvement from 2000, when 25% of public sector debt was denominated in foreign currency.

Brazilian corporations are more vulnerable, but estimates from the BCB show that most companies have some form of protection against currency fluctuations. Exporters representing 36% of external debt are partially protected, as their revenues are in foreign currency. Another 17% of external debt is hedged through local derivatives markets, while 30% is to companies that can draw on assets or head-office support from abroad. That leaves just 17% of external debt as completely unhedged, equivalent to 6% of all corporate debt.

This external liquidity strength greatly reduces the likelihood of a sovereign default, placing a credible floor under just how far the economy may fall. This is by no means an accident but was the result of intentional BCB policymaking. After currency and debt scares in 1999 and again in 2002, the central took advantage of a favorable economic environment to retire public-sector foreign currency debt through debt rollover procedures and also built substantial foreign reserves.

Brazil’s current crisis will be painful. Hopefully, Brazil and other emerging markets learn important lessons of the current crisis to soften the blow of the next one.

September Employment Report Casts a Temporary Shadow

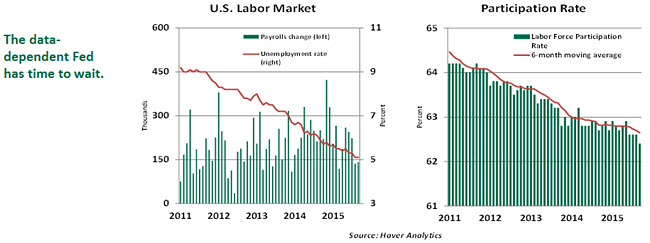

The U.S. unemployment rate held steady in September, payroll gains were on the soft side, and hourly earnings were unchanged – an unexpected combination of labor market data.

The unemployment rate was unchanged at 5.1% as both the labor force and the number unemployed fell. The 350,000 decline in the labor force resulted in a 62.4% labor force participation rate. This is a multi-decade low that the Fed was not expecting.

On the encouraging side, the broader measure of unemployment (U6) fell 3 percentage points to 10.0% and reflects the reduction in the number employed part-time for economic reasons. Chair Janet Yellen noted in her last speech that a reduction in part-time employment signals an improvement in labor market conditions. But we need more data points to confirm this trend, as part-time employees may have dropped out of the labor force.

Nonfarm payrolls increased only 142,000, and there were notable downward revisions to August and July estimates, all adding up to a loss of 59,000 jobs. Construction jobs increased 8,000, but factory employment declined (-9,000) partly related to China. The recent reduction in payrolls at Caterpillar is a case in point. Employment in the energy-related sector continues to show weakness, but the good news is that job losses are not accelerating on a quarterly basis.

Private-service sector employment advanced 131,000, slightly higher than the 122,000 increase of August. Health-care employment rose 34,000, consistent with the average of the last year. Employment in professional business services increased 31,000, putting the year-to-date average at 45,000. The retail and hospitality industry added to job growth. Government employment has risen for five consecutive months; a slowing is possible during the rest of the year.

Average hourly earnings were unchanged in September, which left the year-to-year growth steady at 2.2%. Wage growth has not budged from around 2.0% - 2.3% for six years, and it is under the 3.0% - 3.5% pace that is expected in an economy growing close to its potential. This subdued wage growth picture is a source of concern for the Fed.

It is quite safe to consider that an October policy rate hike is off the table. At the same time, the Federal Open Market Committee has time between now and December to assess the nature of incoming data. There is a weak global demand-and-energy story that explains a large part of the softness in employment during recent months. The Fed needs to see some strengthening of employment compensation, slightly higher inflation readings and convincing growth. A December policy move is still a possibility but the odds have diminished.

The information herein is based on sources which The Northern Trust Company believes to be reliable, but we cannot warrant its accuracy or completeness. Such information is subject to change and is not intended to influence your investment decisions.

Recommended Content

Editors’ Picks

EUR/USD clings to daily gains above 1.0650

EUR/USD gained traction and turned positive on the day above 1.0650. The improvement seen in risk mood following the earlier flight to safety weighs on the US Dollar ahead of the weekend and helps the pair push higher.

GBP/USD recovers toward 1.2450 after UK Retail Sales data

GBP/USD reversed its direction and advanced to the 1.2450 area after touching a fresh multi-month low below 1.2400 in the Asian session. The positive shift seen in risk mood on easing fears over a deepening Iran-Israel conflict supports the pair.

Gold holds steady at around $2,380 following earlier spike

Gold stabilized near $2,380 after spiking above $2,400 with the immediate reaction to reports of Israel striking Iran. Meanwhile, the pullback seen in the US Treasury bond yields helps XAU/USD hold its ground.

Bitcoin Weekly Forecast: BTC post-halving rally could be partially priced in Premium

Bitcoin price shows no signs of directional bias while it holds above $60,000. The fourth BTC halving is partially priced in, according to Deutsche Bank’s research.

Week ahead – US GDP and BoJ decision on top of next week’s agenda

US GDP, core PCE and PMIs the next tests for the Dollar. Investors await BoJ for guidance about next rate hike. EU and UK PMIs, as well as Australian CPIs also on tap.