With the Greek eurozone membership crisis on the back burner for now, we thought this would be a good time to take stock of the euro project. Given the events of the past year, can the shared currency still be called a success?

Writing in 1997, Milton Friedman warned that adoption of the euro would not set the stage for a “United States of Europe.” He wrote, “I believe that adoption of the euro would have the opposite effect. It would exacerbate political tensions by converting divergent shocks that could have been readily accommodated by exchange rate changes into divisive political issues…. Monetary unity imposed under unfavorable conditions will prove a barrier to the achievement of political unity.”

It is notable the extent to which the crisis around Greece mirrors these concerns. But the question of whether the euro was a good idea really depends on what one thinks the common currency was trying to achieve. And here the picture is not as clear cut.

The European push to create a common currency was founded in the belief that this would help to hasten fiscal and, ultimately, political union. It built on the foundations of the European common market, which intended to bind nations economically so that they would be less inclined to conflict with one another.

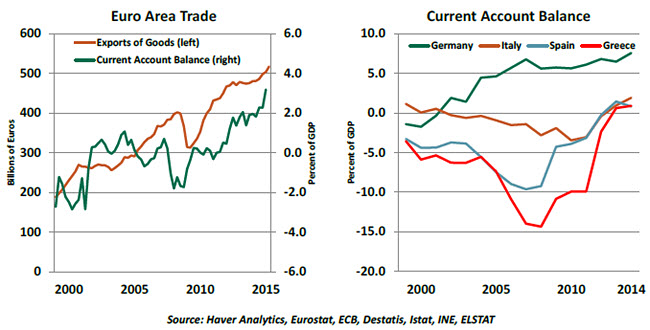

The euro today is shared by more than 330 million citizens across 19 countries and is second only to the U.S. dollar in its share of global foreign exchange reserves (24.4% to the U.S.’s 61.2%). The European Commission itself lauds the benefits of the euro in terms of making the single market more efficient, and the common currency has boosted trade for its members (although it is clear that not all members have benefited equally).

It is also a club that new members have been eager to join. From the initial crop of 11, membership has risen to 19. Some joined in part for geopolitical reasons; the smaller Baltic nations, looking over their shoulders at the looming threat that is Russia, were eager members. For smaller eastern European nations heavily dependent on exports to other members, the common currency was a significant trade boost. And even through the recent travails, Greeks have remained strong supporters – perhaps because the eurozone’s rules-based approach to monetary policy is appealing after years under corrupt elites.

But on a closer look, the claim of a “rules-based approach” falters. Indeed, “flexible” interpretations of the rules began with the founding of the eurozone, when Italy and Belgium were allowed in despite the fact that their public debt to gross domestic product (GDP) ratios were well over the 60% limit. In fact, since 1997 all but two of the members have been subject to an excessive deficit warning at least once, for having a public sector deficit in excess of 3% of GDP (the exceptions being Estonia and Luxembourg).  In the period 1999-2007, investors treated all members of the eurozone as one, without taking into account divergent economic and financial risks. Powerhouse Germany had enacted policies to restrain wage growth and generate jobs, leading to a decline in domestic consumption along with a build-up in the nation’s savings. German banks essentially exported that excess capital to the eurozone “periphery.” Credit flooded into some countries and sectors without taking into account their underlying productivity or competitiveness.

In the period 1999-2007, investors treated all members of the eurozone as one, without taking into account divergent economic and financial risks. Powerhouse Germany had enacted policies to restrain wage growth and generate jobs, leading to a decline in domestic consumption along with a build-up in the nation’s savings. German banks essentially exported that excess capital to the eurozone “periphery.” Credit flooded into some countries and sectors without taking into account their underlying productivity or competitiveness.

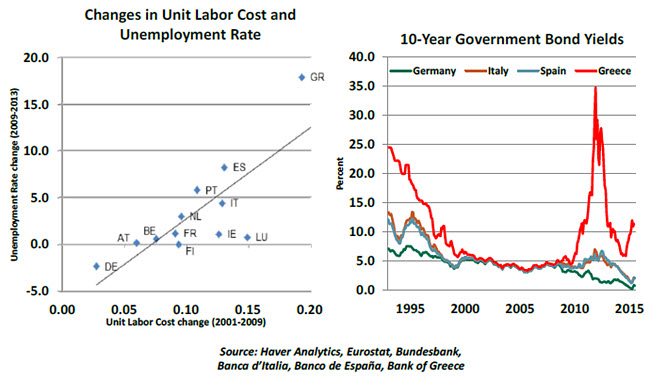

Most countries did not use this period of strong growth to implement fiscal reform or to tackle rigid labor and product markets. As a result, the cost of labor grew significantly in some countries, reducing their competitiveness. When crisis hit, it was glaringly obvious that the currency union had not brought about equal levels of prosperity to all its members. Instead, countries that could no longer devalue their way back to competitiveness had to inflict internal devaluations to bring down costs. And this heightened political discontent.

Interestingly, recent trauma may bring the eurozone closer at some levels. Since 2008, the eurozone has created new mutual support programs; set up a banking union with a single supervisory mechanism and new resolution rules; and taken steps toward a closer fiscal union.

So back to our original question: has the euro been a success? For individual countries, the answer is mixed. Germany’s exporters clearly have benefited, but Berlin wears the mantle of leadership uneasily. France’s dream of a political union underpinned by French notions of solidarity has instead led to a German-dominated union in which France’s economy is losing competitiveness. Italy and Spain are suffering through a period of wrenching macroeconomic reform, but they also benefit from a very low cost of borrowing in the global markets.

In February 2015, Jean-Claude Juncker wrote in an Analytical Note to the European Council that “The euro is more than a currency. It is also a political project … [that has] … created a “community of destiny” between the 19 Member States.” This is the real basis on which the euro should be judged: has it helped to bring “Europe” closer together in the sense of a shared political destiny?  For a while, it seemed this larger goal had been jeopardized by anger at Greece’s political leadership, and that country’s woes could yet endanger the principle of an irrevocable monetary union. It is also true that there’s nothing like a crisis to help renew the commitment to a shared political destiny. The creation of the euro was done for political reasons; as long as it is politically less costly for its members than the alternatives, the euro is here to stay.

For a while, it seemed this larger goal had been jeopardized by anger at Greece’s political leadership, and that country’s woes could yet endanger the principle of an irrevocable monetary union. It is also true that there’s nothing like a crisis to help renew the commitment to a shared political destiny. The creation of the euro was done for political reasons; as long as it is politically less costly for its members than the alternatives, the euro is here to stay.

Disarming the Bond Markets

James Carville, the pugnacious aide to former President Bill Clinton, once wished to be reincarnated as the bond market so that he could intimidate everybody. Long-term interest rates were marching upward at the time, out of concern for what some investors viewed as reckless federal spending. These “bond vigilantes” were very influential at the time, and policymakers ignored them at their own peril.

So as the Federal Reserve contemplates an interest rate increase next month, it is keeping a watchful eye on how long-term interest rates behave. For the moment, however, it appears that the vigilantes have put down their pitchforks.

The Fed would like the bond market to remain reasonably settled as monetary policy changes. Market volatility might tend to diminish the appetite for taking risk, which can grow the economy. And the housing industry, still working its way slowly back from the 2008 crisis, would like mortgage rates to remain low.

There are many factors that bear on long-term yields. Expectations surrounding monetary policy are certainly important, not just in the levels that short-term rates might reach but in the uncertainty surrounding this path. Investors purchasing an instrument with a long duration require a term premium to compensate for this.

This term premium has historically hovered between 1% and 2%. But even though there seems to be considerable uncertainty about the long-term course of Fed policy, the term premium is right around zero at the moment.

Issuance patterns are another element. If the Treasury is selling more long-term securities to finance spending, then the increased supply will tend to raise long-term interest rates. The U.S. budget deficit has been steadily shrinking, but it remains near 3% of GDP. And the Treasury has been issuing an increasing share of long-term instruments to finance the nation’s debt.

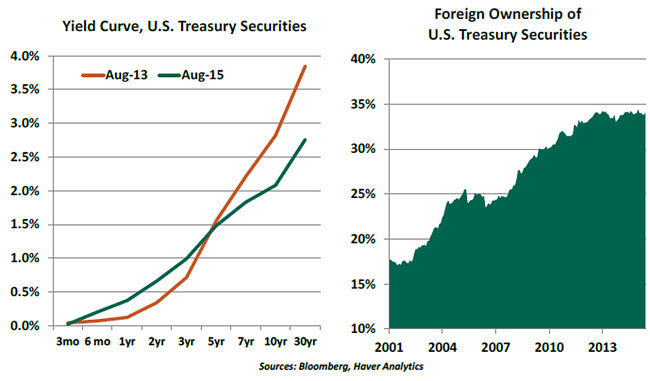

In spite of all this, the 10-year U.S. Treasury yield is a little over 2% as of this writing. And the yield curve is considerably flatter than it was two years ago, when Ben Bernanke unexpectedly sounded the alarm about tapering the Fed’s quantitative easing program.

Recent statements from the Fed have been quite a bit more measured than they were in 2013, so some of today’s benign conditions may be due to careful communication. But there is something more significant at play.  The American government bond is a global asset class; foreigners own more than a third of the debt held by the public. It is a safe haven in times of international unrest and an instrument of currency diversification for global investors (especially from emerging markets). The Treasury market is arguably the deepest fixed-income market in the world. And while 2% may not seem like much, the U.S. 10-year yield is higher than one will find in most other developed markets.

The American government bond is a global asset class; foreigners own more than a third of the debt held by the public. It is a safe haven in times of international unrest and an instrument of currency diversification for global investors (especially from emerging markets). The Treasury market is arguably the deepest fixed-income market in the world. And while 2% may not seem like much, the U.S. 10-year yield is higher than one will find in most other developed markets.

Foreign demand has also been very active in the Treasury Inflation Protected Securities market and may be one reason the inflation expectations that market implies are so low. This source suggests that inflation will average a little more than 1.5% over the next 10 years, down from 1.9% two months ago. This influence creates a distortion that diminishes the utility of this reading as a true guide to future inflation.

So while it is dangerous to suggest that fundamentals don’t matter in asset pricing, it might be fair to say that a different set of factors drives some incremental purchasers . Unlike 2013, suggestions of Fed tightening do not seem to have scared investors away from U.S. Treasuries. And so, at least for now, the Fed should not be scared of the bond vigilantes.

The View from Jackson Hole

Each August, the Federal Reserve Bank of Kansas hosts a gathering of economists, central bankers, finance ministers and financial market participants from around the world at Jackson Hole, Wyoming. The theme of this year’s meeting, which commences on August 27, is “Inflation Dynamics and Monetary Policy.” Here are some angles that may be discussed.

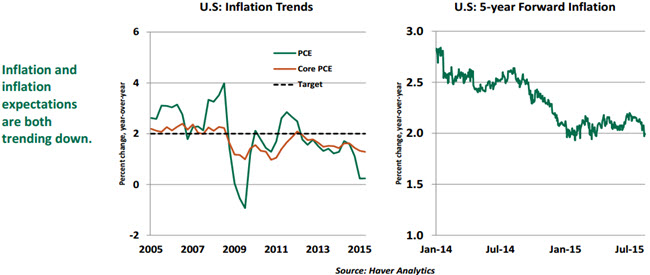

The Federal Reserve’s Federal Open Market Committee (FOMC) has set a long-run objective for consumer price inflation of 2.0%. Since early 2012, the Fed’s preferred measures of inflation have hovered below this target. In June, the year-over-year change in the personal consumption expenditures (PCE) price index was 0.3%. The year-over-year change in the core PCE price index, which excludes food and energy, was 1.3% in June.

Against this backdrop, given that inflation lags the business cycle, the key question is whether the Fed is likely to act pre-emptively at the September FOMC meeting. The Fed has stressed that it only needs to be confident about price gauges moving back toward the inflation target (rather than actually hitting it) to implement a higher policy rate, which suggests that a pre-emptive move is consistent with the Fed’s rhetoric.

There are other questions about inflation dynamics and monetary policy that should be addressed at this year’s gathering:

- Are the disinflationary forces from around the globe so strong that central banks cannot independently reach their inflation targets?

- Is nominal wage rigidity still an important factor behind the benign inflation picture?

- How transitory will trends in energy and commodity prices prove to be? Does it remain wise to focus solely on core measures of inflation?

The symposium’s discussions will hopefully shed some light on these issues as we approach the critical September 2015 FOMC meeting. We’ll scan the papers being discussed when they are released and report any insights that emerge.

Recommended Content

Editors’ Picks

AUD/USD favours extra retracements in the short term

AUD/USD kept the negative stance well in place and briefly broke below the key 0.6400 support to clinch a new low for the year on the back of the strong dollar and mixed results from the Chinese docket.

EUR/USD now shifts its attention to 1.0500

The ongoing upward momentum of the Greenback prompted EUR/USD to lose more ground, hitting new lows for 2024 around 1.0600, driven by the significant divergence in monetary policy between the Fed and the ECB.

Gold aiming to re-conquer the $2,400 level

Gold stages a correction on Tuesday and fluctuates in negative territory near $2,370 following Monday's upsurge. The benchmark 10-year US Treasury bond yield continues to push higher above 4.6% and makes it difficult for XAU/USD to gain traction.

Bitcoin price defends $60K as whales hold onto their BTC despite market dip

Bitcoin (BTC) price still has traders and investors at the edge of their seats as it slides further away from its all-time high (ATH) of $73,777. Some call it a shakeout meant to dispel the weak hands, while others see it as a buying opportunity.

Friday's Silver selloff may have actually been great news for silver bulls!

Silver endured a significant selloff last Friday. Was this another step forward in the bull market? This may seem counterintuitive, but GoldMoney founder James Turk thinks it was a positive sign for silver bulls.