We’ve written about Greece a number of times since the start of this year, and in that time depressingly little has changed. Athens still faces both a near-term liquidity crunch and a fundamental solvency crisis. The liquidity crunch is about to end, one way or another.

The fact that we have arrived at the eleventh hour without an accord speaks volumes both about the dire state of the Greek economy and about the political considerations that drive the eurozone. Arguably, the last several months have seen the sides distance themselves from one another, and there may not be enough time left to close the fiscal and emotional gaps that have been created.

To recap, the current round of negotiations between Greece and its creditors aims to close out an aid program that was originally set to be completed in December 2014 – a deadline that has been extended twice and now stands at June 30. The program traded quarterly disbursements from the European Union (EU) and the International Monetary Fund (IMF) for Greek progress on structural and budget reforms. The contingent structure was designed to keep the pressure on Athens to implement change.

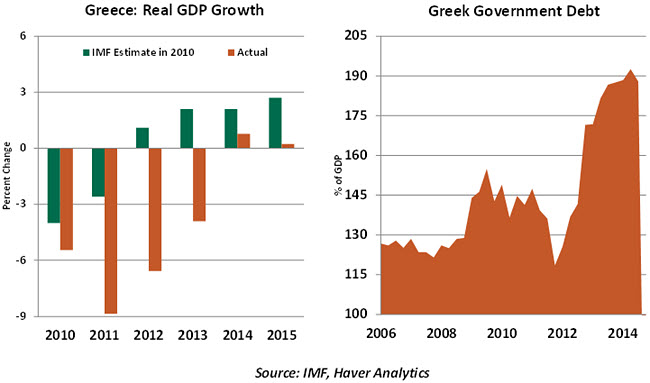

Greece had been doing a reasonably good job of managing its spending; the country had a primary surplus (the budget balance before interest costs are deducted) last year. But the Greek economy is 27% smaller than it was at the beginning of 2008, far underperforming the projections underlying the first IMF support program in 2010.

Poor economic performance has led Greece’s debt to new heights, in spite of the 2012 restructuring of private sector debt that reduced its value by about 75%. The crippling austerity led to a change of government early this year, and the new regime has demanded relief.

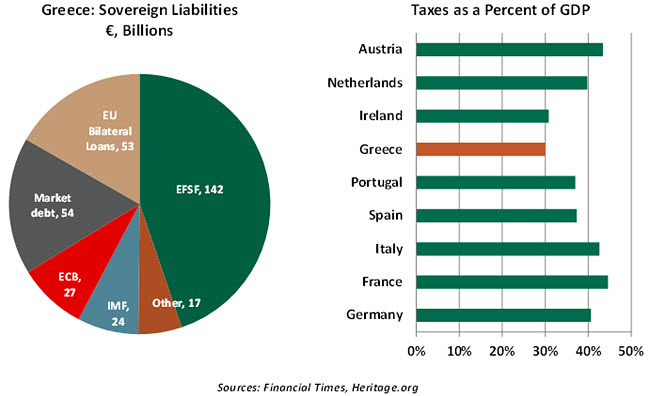

As a result of the private-sector debt restructuring, European institutions now hold almost 80% of Greek government debt. The single largest creditor is the European Financial Stability Fund (EFSF), which is jointly owned by all the eurozone countries.

Greece’s ruling Syriza party has hoped that the fear of loss would bring conciliation from the country’s creditors. The platform that got them elected leaves very little room for compromise; any agreement that includes backwards steps faces an uncertain fate in the Greek parliament and could cause the government to fall.  But at the same time, none of Greece’s creditors wants to be portrayed as “soft” on a serial debtor which (in their view) has dragged its feet on making needed changes to its pension and taxation systems. (Greece raises less tax revenue as a percentage of GDP than most other members of the eurozone, in part because of the structure of the Greek tax code and in part because tax collection has proven challenging.) With other debtor countries like Portugal and Spain watching the proceedings closely, lenders are anxious not to set a precedent that others could use to demand similar concessions.

But at the same time, none of Greece’s creditors wants to be portrayed as “soft” on a serial debtor which (in their view) has dragged its feet on making needed changes to its pension and taxation systems. (Greece raises less tax revenue as a percentage of GDP than most other members of the eurozone, in part because of the structure of the Greek tax code and in part because tax collection has proven challenging.) With other debtor countries like Portugal and Spain watching the proceedings closely, lenders are anxious not to set a precedent that others could use to demand similar concessions.

The most important voice in the debate is Germany’s, the eurozone’s wealthiest country. Unfortunately, Greek Prime Minister Alex Tsipras and his associates have gone out of their way to antagonize Berlin. At the beginning of this year, only a third of German voters wanted Greece to leave the eurozone, but according to a recent poll, that proportion has now risen to 51%.

Neither side wants to be responsible for triggering a Greek default that might prompt an exit from the eurozone and potential knock-on effects. The eurozone’s finance ministers have shown some willingness to “kick the can down the road” when it comes to tough decisions, but they have insisted on commitments to structural changes as a first step toward any conversation about another round of debt relief.

Earlier this week Mr. Tsipras proposed a “final” reform package to the creditors that amounted to about €7.9 billion in new tax hikes and pension cuts. This kicked off a storm of protest at home and a lukewarm reception from creditors, who found the outline too long on growth-limiting tax increases and too short on direct cuts to transfer payments.  The two sides are fast approaching a June 30 deadline to renew Greece’s assistance program and allow it to make a €1.6 billion payment due that day. The IMF has said that not making that payment will leave Greece formally in default. Negotiations are scheduled to continue through the weekend; even if a stopgap agreement is reached, it would require a series of approvals in European capitals where success is by no means assured.

The two sides are fast approaching a June 30 deadline to renew Greece’s assistance program and allow it to make a €1.6 billion payment due that day. The IMF has said that not making that payment will leave Greece formally in default. Negotiations are scheduled to continue through the weekend; even if a stopgap agreement is reached, it would require a series of approvals in European capitals where success is by no means assured.

And the can cannot be kicked down the road much further. €6.9 billion is due from Greece to the European Central Bank (ECB) in July and August and another large IMF debt repayment is due in September. As things stand, Athens has no way to meet those obligations. The ECB earlier this year ruled out any form of debt swap; the IMF is fretting about debt sustainability; and it is hard to see how much more eurozone creditors can extend maturities or lower interest rates.

Hard realities and hardened positions are combining to create a dangerous game of financial chicken between Greece and its creditors. We can only hope they avoid a headlong collision that could create a lot of collateral damage.

Going the Wrong Way?

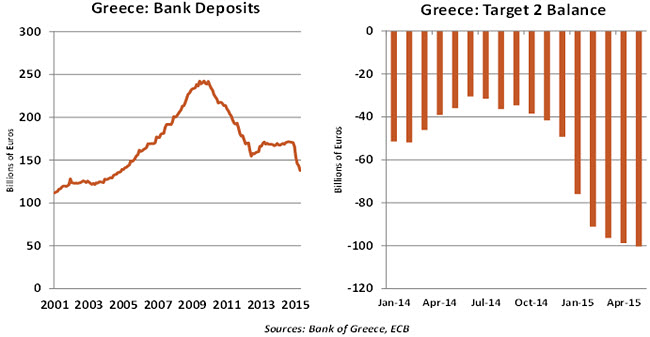

The parallels between the European Central Bank and the Federal Reserve are growing deeper. Early this year, the ECB ventured into the realm of quantitative easing, promising to add significant volumes of government securities to its balance sheet. Over the past couple of months, the ECB has followed another path cleared by the Fed in 2008. The ECB is using its balance sheet aggressively to keep the Greek banking system upright, buying time for the country and its creditors to reach an accord.

Rising anxiety has led depositors to flee Greek institutions, and the ECB has been forced to replace the lost funding through its Emergency Liquidity Assistance (ELA) program. This support is reflected in a growing Greek liability to the Target 2 system, the platform that processes interbank payments for the eurozone.  Essentially, the ECB has been deepening its exposure to Greece just as others have been reducing it. Because Greek government bonds serve as collateral for ELA borrowings, the ECB is vulnerable to “wrong way risk,” a situation where the security against loan default deteriorates at the same time the credit does. Should a worst-case outcome occur, the ECB (and by inference, its component shareholders) would be vulnerable to a sizeable loss.

Essentially, the ECB has been deepening its exposure to Greece just as others have been reducing it. Because Greek government bonds serve as collateral for ELA borrowings, the ECB is vulnerable to “wrong way risk,” a situation where the security against loan default deteriorates at the same time the credit does. Should a worst-case outcome occur, the ECB (and by inference, its component shareholders) would be vulnerable to a sizeable loss.

Serving as a lender of last resort is a core responsibility of central banks. However, the lending typically requires solid collateral and should ideally be used to meet liquidity needs that are temporary. The Fed stretched the boundaries of its Discount Window in 2008, acquiring assets from struggling institutions and offering support to financial companies that it did not regulate. This was all done in the name of preserving financial stability, and the success of the effort ameliorated those who had expressed concern.

The ECB is clearly stretching in its support for Greece, hoping to preserve financial stability. But if a resolution is not reached, the ECB could lose a lot of money and potentially some of its credibility.

Budget Benefits

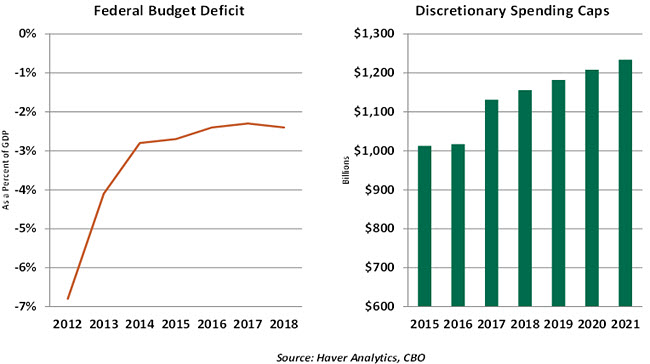

The Congressional Budget Office’s (CBO) March update on the U.S. federal budget estimated the deficit for FY2015 to be $486 billion or 2.7% of gross domestic product (GDP). A stronger revenue stream visible in year-to-date federal budget data suggests the deficit is likely to be lower than the CBO’s prediction.

The three main sources of federal tax revenue are individual income taxes, payroll taxes and corporate income taxes. Year-to-date, tax receipts from each of these sources exceeds readings of FY2014. On the spending side, defense spending is running lower in FY2015 compared with the prior year, while Medicare and Medicaid outlays are higher. Interest spending is lower than in 2014 largely due to lower interest rates.

Based on the CBO’s estimates, the federal budget deficit should be stable during the next three years. With a deadlocked Congress and the upcoming presidential election in 2016, major changes in fiscal policy (or tax reform) should not be expected. However, there are near-term issues related to the federal budget that are worth examining.

Firstly, the U.S. Treasury is using “extraordinary measures” to remain under the debt ceiling, which became binding again in March 2015. Given the strength of revenue growth, the ceiling may not need to be raised until very late this year. There will be political pressure to attach other policy changes to the legislation addressing the debt ceiling limit, and those conversations might be difficult. However, the commitment of both parties to prevent another debt ceiling drama (and avoid the anger of the electorate heading into 2016) is strong.

Secondly, the appropriations process is underway for the upcoming fiscal year. The Budget Control Act of 2011 set caps on discretionary spending through 2021. The Bipartisan Budget Act of 2013 raised spending caps in 2014 and 2015 but the trajectory enacted for years beyond that was left unchanged.

The current cap calls for almost flat discretionary spending in 2016 versus 2015. Both Republicans and Democrats have talked about lifting the spending caps for FY2016, albeit in different areas. Because this would imply a greater risk of a wider deficit, markets will be sensitive to how these discussions proceed.  The Supreme Court ruled this week in favor of insurance subsidies provided under the Affordable Care Act irrespective of whether they are purchased through the state or federally run exchanges. The CBO estimates that subsidies provided through the exchanges will amount to $855 billion during the 10 years from 2015 to 2024. The ruling has lifted the near-term uncertainty about the program but uncertainty about healthcare spending, despite recent improvements, will continue to be an important factor in the budget outlook.

The Supreme Court ruled this week in favor of insurance subsidies provided under the Affordable Care Act irrespective of whether they are purchased through the state or federally run exchanges. The CBO estimates that subsidies provided through the exchanges will amount to $855 billion during the 10 years from 2015 to 2024. The ruling has lifted the near-term uncertainty about the program but uncertainty about healthcare spending, despite recent improvements, will continue to be an important factor in the budget outlook.

Other budgetary considerations that are on the radar screen are smaller in size but nonetheless important. Bonus depreciation, the research and development tax credit, and the highway transportation program need immediate decisions.

Bonus depreciation allows firms to deduct 50% of capital investment immediately, which is viewed as a means of boost investment spending. Given the lackluster pace of investment outlays, there is a good case to extend this provision. Another temporary fix is expected for the highway program, which we have noted is in desperate need of long-term attention.

Although the near-term issues related to the federal deficit are modest, the medium- and long-term challenges are still problematic and need to be addressed. Unfortunately, these may not get much attention until the new President and the new Congress are seated in early 2017. By that time, interest rates may well be on the rise, ending our string of budgetary good news.

Recommended Content

Editors’ Picks

EUR/USD clings to daily gains above 1.0650

EUR/USD gained traction and turned positive on the day above 1.0650. The improvement seen in risk mood following the earlier flight to safety weighs on the US Dollar ahead of the weekend and helps the pair push higher.

GBP/USD recovers toward 1.2450 after UK Retail Sales data

GBP/USD reversed its direction and advanced to the 1.2450 area after touching a fresh multi-month low below 1.2400 in the Asian session. The positive shift seen in risk mood on easing fears over a deepening Iran-Israel conflict supports the pair.

Gold price defends gains below $2,400 as geopolitical risks linger

Gold price is trading below $2,400 in European trading on Friday, holding its retreat from a fresh five-day high of $2,418. Despite the pullback, Gold price remains on track to book the fifth weekly gain in a row, supported by lingering Middle East geopolitical risks.

Bitcoin Weekly Forecast: BTC post-halving rally could be partially priced in Premium

Bitcoin price shows no signs of directional bias while it holds above $60,000. The fourth BTC halving is partially priced in, according to Deutsche Bank’s research.

Geopolitics once again take centre stage, as UK Retail Sales wither

Nearly a week to the day when Iran sent drones and missiles into Israel, Israel has retaliated and sent a missile into Iran. The initial reports caused a large uptick in the oil price.