If you’re late to the party, you’d better make a grand entrance. The European Central Bank (ECB) tried to keep this in mind as it formulated the aggressive quantitative easing (QE) program that was announced yesterday. The question now is whether it is too little, too late.

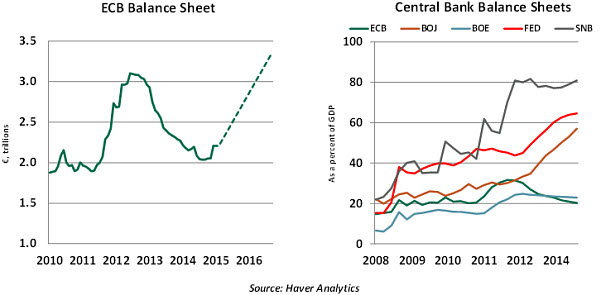

As widely expected, the ECB finally moved to purchase the sovereign debt of its members on a large scale. Starting in March, the ECB will buy a total of €60 billion in public and private assets every month. The program will run at least through September 2016, at which point the ECB’s balance sheet will have grown by €1.14 trillion.

Purchases will continue until there is a sustained adjustment in the path of inflation, consistent with the ECB’s sole mandate of inflation rates “below, but close to, 2% over the medium term.” This was an important statement – not only does it effectively make the program open-ended, it also ties “success” specifically to the rate of inflation. This underlines the primacy of the ECB’s independent inflation mandate and represents a major step in its evolution as a central bank.

While some are concerned about an open-ended program (the Federal Reserve’s version was derisively called “QE infinity” by some), the design has advantages. First, it will restore the ECB’s balance sheet to its 2012 level, and likely go beyond that. When a central bank’s balance sheet is shrinking, it restrains economic activity; by allowing its balance sheet to contract over the past two years, the ECB may have contributed to the eurozone’s current malaise.

According to the plan, the ECB’s balance sheet will stand at 34% of eurozone gross domestic product (GDP) next September. This would exceed the Bank of England’s QE program (about 22% of GDP) or the Federal Reserve’s (25% of GDP). But because conditions have been allowed to deteriorate for so long, Japan’s QE goal of 60% of GDP might be a more relevant benchmark.

To listen to ECB President Mario Draghi, the devil really was in the details. The purchases will be executed by the ECB and its member national central banks. The amounts purchased will be in proportion to each country’s share of the ECB’s capital, meaning that German bonds will comprise the largest share even though Germany’s economy needs the least assistance.  Assets eligible for purchase must be investment grade unless the country has an international aid program in place. Some saw this as an important message to Greece as it goes to the polls on Sunday; if a country is unable to keep its external creditors comfortable, it falls out of the QE program.

Assets eligible for purchase must be investment grade unless the country has an international aid program in place. Some saw this as an important message to Greece as it goes to the polls on Sunday; if a country is unable to keep its external creditors comfortable, it falls out of the QE program.

The program’s construction was influenced by a tricky discussion of who might bear losses if anything goes wrong. Having the national central banks buy their country’s bonds addresses some of the concern, but any losses on bonds owned by the ECB would be shared. It appears that some on the ECB Governing Council lobbied hard to minimize this element. This exasperated Draghi, who was more focused on doing the right thing for the eurozone economy.

But the ECB’s Governing Council will retain “full control” of the program’s design and will coordinate purchases. The eurozone’s 19 national central banks are part of a wider euro-system that includes the ECB – and yesterday the Governing Council reminded them all that it is the final source of authority in the system. This is another major step in the ECB’s maturation.

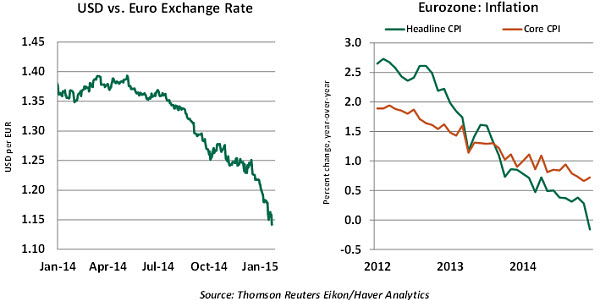

But it is not clear just how effective the program will be in meeting its key aim of restoring normal levels of inflation. The euro fell further against other world currencies after the announcement, which will have the tangible benefit of improving the eurozone’s terms of trade. It will also raise the cost of imported goods (including oil), aiding in the fight against deflation.

Yet other central banks will be in no hurry to help the euro get weaker. The Bank of Canada unexpectedly cut its main policy rates this week and the Bank of England looks set to delay interest rate hikes until 2016. And if the initial eurozone stock market rally continues, the resulting inflow of investment funds could actually boost the euro.

Sovereign bond yields in the eurozone are already at record lows, and lowering them further through the QE program will not produce much additional economic activity. Europe gets most of its credit from banks rather than the capital markets, so this translation would be an indirect one in any event. And as we’ve written before, the eurozone banking system is still in need of some reinforcement, and the ECB would do well to turn its attention in this direction.  Beyond the scope of the ECB, the slow pace of structural reform remains an economic impediment for the eurozone. And fiscal austerity is still firmly in place in many countries. These two factors will continue to limit progress.

Beyond the scope of the ECB, the slow pace of structural reform remains an economic impediment for the eurozone. And fiscal austerity is still firmly in place in many countries. These two factors will continue to limit progress.

But fundamentally and symbolically, the ECB has set an important tone, which one can only hope that other European leaders will follow. Draghi may not be able to do whatever it takes, but he does seem to be doing everything he possibly can.

U.S. Federal Budget – Putting Things in Perspective

The federal budget of the United States has improved significantly as a result of a recovery that is more than five years old. But it is well known that the current favorable situation is temporary, and a significant widening of the deficit in the years ahead is nearly certain. Congress and the administration should attempt to address this problem now, not later.

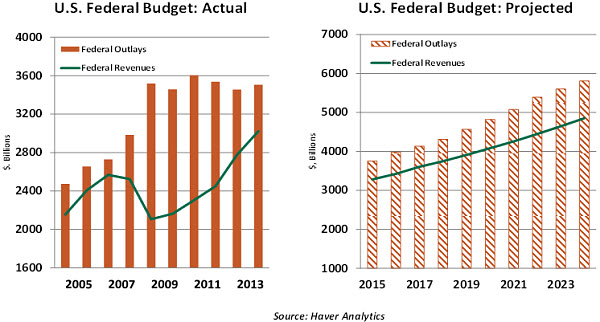

Recent U.S. budget data are useful to frame this discussion. Federal government revenues increased roughly $900 billion in the five years ended 2014 because of the upswing in economic activity. New taxes under the American Taxpayer Relief Act and the Affordable Care Act also helped to increase federal receipts.

At the same time, the federal government’s total outlays held nearly steady during the past five years. This positive confluence of events resulted in a sharp reduction of the federal budget deficit to $483 billion in fiscal year 2014, down from an outsized $1.4 trillion shortfall in 2009. The federal budget deficit as a percent of GDP stands at 2.8% versus a high of 9.9% in 2009 and a pre-recession mark of 1.1%.

Looking ahead, the Congressional Budget Office (CBO) projects a nearly steady budget deficit as a percent of GDP until 2018, followed by a consistent widening for an extended period.

Of the numerous outlays contributing to this looming challenge, mandatory federal government expenditures (Medicare, Medicaid and Social Security) and interest obligations are the most major, as they are projected to accelerate rapidly in the decade ahead.  The Social Security expense tab is less burdensome because feasible options exist to contain its growth. Modest alterations to benefit calculations, retirement ages and other parameters have been used in the past when the system has been threatened. These likely can be employed again.

The Social Security expense tab is less burdensome because feasible options exist to contain its growth. Modest alterations to benefit calculations, retirement ages and other parameters have been used in the past when the system has been threatened. These likely can be employed again.

Medicare expenses are projected to grow partly due to demographic reasons and partly due to inflation in treatment costs. The good news is that Medicare expenses have moderated, but there is no guarantee this will prevail in the years ahead. Hence, it is crucial to ensure that benefits are funded within the limits of fiscal prudence.

The Fed is predicted to commence normalization on interest rates later this year. Current interest costs will increase as the Treasury issues new bonds at higher interest rates to replace bonds that mature. The CBO projects that interest costs will reach nearly 14% of federal outlays by 2024, up from a little over 6% today, as interest rates increase. In addition to this cost, the potential crowding out of private investment is a significant setback if federal budget challenges remain neglected.

Given the sanguine short-term fiscal situation and a growing economy, President Obama outlined proposals on the revenue side of the federal budget at the State of the Union address earlier in the week. The proposed corporate tax reform has bipartisan support and it is part of the strategy to fund infrastructure outlays.

Other revenue-raising measures included in the President’s proposals, such as higher capital gains taxes and dividend tax rates and a fee on liabilities of large financial institutions, are aimed at raising roughly $300 billion to fund different tax credits for low- and middle-class households. The higher taxes and new programs are unlikely to progress, though, as Republicans present their own tax-reform proposals.

Many suspect the recent volley of economic proposals and counterproposals is little more than posturing in advance of the 2016 presidential election. But unfortunately, two more years of stasis makes solving the country’s long-term fiscal problems more challenging. Eventually, the two parties will have to agree on a combination of revenue and cost measures that not only limit annual deficits, but also reduce the size of the nation’s debt.

The economy is in a stronger position today to address the trajectory of outlays and revenues than it was a few years ago. It would be a significant loss not to seize the opportunity to make the strength more permanent than transitory.

Risk Management Myopia

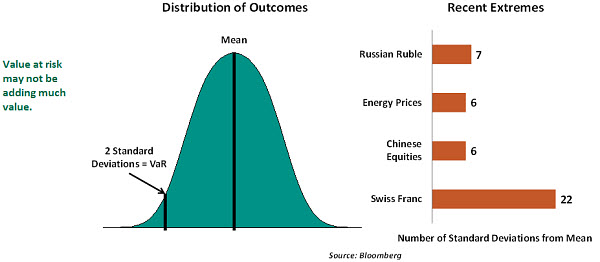

January isn’t over yet, and we’re already dealing with a series of events that few anticipated. Oil at $45 per barrel, the Shanghai stock index off 7% in a day, and the sudden change in Swiss monetary policy are the most prominent examples. When markets move to these kinds of extremes, they create problems for institutional risk management. And these problems can create even bigger problems for financial markets.

For many years, value at risk (VaR) has been a standard approach to gauging the vulnerability of positions and portfolios. VaR typically looks back at how assets would have performed over a trailing history, assembling a distribution of outcomes. As shown in the diagram below, the risk is quantified by looking at the worst of these, based on a number of standard deviations from the mean.

VaR has a certain appeal. It captures risk in a single number and it appears to be objectively derived. But it has a number of notable weaknesses. Among them:

- Many challenging market movements are a long way from average. Where VaR is based on two or three standard deviations from the mean, changes of many times that size happen with surprising frequency. VaR does not handle “black swans” very well.

- VaR is very pro-cyclical, meaning it will make positions look overly benign in settled markets and overly dangerous when there is an adverse shift. The signals VaR sends to traders can therefore accentuate market corrections.

- The parameters used to calculate VaR, including the time horizon used for the distributions and the number of standard deviations used to assess risk, are subjectively established. Changing these elements can have a big impact on the reported risk of a position, and have been used in the past to hide problems.

VaR performed very poorly during 2008, and has been the subject of some restructuring since. But its inherent limitations are a source of worry as institutions react to the recent series of unfortunate events.

Recommended Content

Editors’ Picks

EUR/USD clings to daily gains above 1.0650

EUR/USD gained traction and turned positive on the day above 1.0650. The improvement seen in risk mood following the earlier flight to safety weighs on the US Dollar ahead of the weekend and helps the pair push higher.

GBP/USD recovers toward 1.2450 after UK Retail Sales data

GBP/USD reversed its direction and advanced to the 1.2450 area after touching a fresh multi-month low below 1.2400 in the Asian session. The positive shift seen in risk mood on easing fears over a deepening Iran-Israel conflict supports the pair.

Gold holds steady at around $2,380 following earlier spike

Gold stabilized near $2,380 after spiking above $2,400 with the immediate reaction to reports of Israel striking Iran. Meanwhile, the pullback seen in the US Treasury bond yields helps XAU/USD hold its ground.

Bitcoin Weekly Forecast: BTC post-halving rally could be partially priced in Premium

Bitcoin price shows no signs of directional bias while it holds above $60,000. The fourth BTC halving is partially priced in, according to Deutsche Bank’s research.

Week ahead – US GDP and BoJ decision on top of next week’s agenda

US GDP, core PCE and PMIs the next tests for the Dollar. Investors await BoJ for guidance about next rate hike. EU and UK PMIs, as well as Australian CPIs also on tap.