Watching the Federal Reserve is a strange and esoteric pursuit. Observers are reduced to endless parsing of adjectives and adverbs, sorting hawks from doves and trying to identify the dots in scatter plots of Fed forecasts. Years ago, we even attempted to correlate the size of the chairman’s briefcase with decisions to raise interest rates. Pretty sad, if you ask me.

Nonetheless, this cottage industry is unlikely to recede anytime soon. Central bank policy in the United States has ripple effects for economies and markets throughout the world. And it is being monitored more closely than ever now as the Fed contemplates rolling back six years of extraordinary accommodation.

The Federal Open Market Committee (FOMC) will conduct its final meeting of 2014 next week. We expect it to drop the pledge “to maintain the 0 to 1/4 percent target range for the federal funds rate for a considerable time.” Here are some factors that will contribute to the upcoming discussion.

The Inflation Outlook

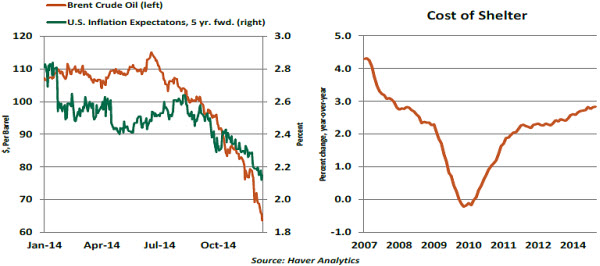

The U.S. price level certainly hasn’t endured the intense disinflationary pressure experienced in Europe. But inflation is below the Fed’s 2% target, and there are concerns that falling energy prices and the strong dollar – both of which eventually will serve to reduce import prices – will widen this gap.

It is challenging for forecasters and policymakers to put the recent decline in oil prices into proper perspective. Because energy markets can be volatile, care must be taken not to overreact to sudden movements. That is why the Fed focuses on core measures of inflation.

Nonetheless, few are predicting a sudden reversion to $90 per barrel, given the state of global supply and demand. The impact of cheaper oil on transportation costs will bring core inflation down somewhat over the next few months. And inflation expectations show a very close association with oil prices and should remain very much muted.

On the other side of the ledger, though, the cost of shelter (which carries the largest weight in the major American price indices) has risen by nearly 3% over the last year. And with unemployment declining, wages may finally be poised to rise a little more rapidly, which could put upward pressure on the prices of a range of goods and services. To some on the FOMC, the gap between current levels of U.S. inflation and the official goal is unacceptably large. Because inflation has run well below its target for a long time, this group further believes that it should be allowed to exceed 2% for a time, at least until the security of the expansion is clear. If the price level begins to grow too rapidly, they contend, it can be addressed in real time.

To some on the FOMC, the gap between current levels of U.S. inflation and the official goal is unacceptably large. Because inflation has run well below its target for a long time, this group further believes that it should be allowed to exceed 2% for a time, at least until the security of the expansion is clear. If the price level begins to grow too rapidly, they contend, it can be addressed in real time.

But to others, recent increases in U.S. gross domestic product (GDP) provide a strong sense of confidence in the growth outlook. The pace of gains has exceeded long-term potential and reduced resource gaps. While there may be no need to act aggressively to head off unwanted inflation, taking the first steps toward normalizing monetary policy sometime next year makes sense.

Labor Markets

The United States has made significant progress on the employment front over the last year, with the data filling in the Fed’s dashboard remarkably well.

Unemployment has fallen to 5.8% from 7% in the past 12 months. A broader measure, which includes those working part-time for economic reasons and those marginally attached to the labor force, has fallen by 1.7% over the past year. Monthly job creation has averaged better than 235,000 positions over that span; as we discussed in October, a gain of 100,000 can be considered a good reading.

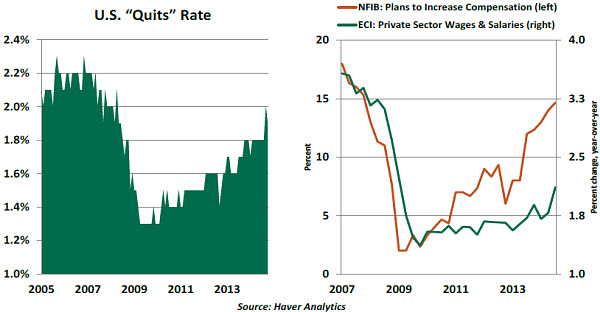

There is one labor market goal that remains unfulfilled. Wages have not progressed as they had during past expansions, suggesting the presence of continued slack. There are several theories why wages have been stuck: workers settling for suboptimal jobs; the presence and threat of automation; and competition from labor markets in other countries.

Recent signs are encouraging on this front. Hourly wages showed a nice gain last month, and more workers are voluntarily quitting their jobs to seek better ones. Surveys suggest that employers are expecting to raise wages, and their anticipations have historically correlated well with actual gains in pay packages.

We’re not at full employment yet. But we’re well on our way.

Other Influences

Aside from progress on its dual mandate, the Fed’s decisions in the months ahead will have to respect a couple of other factors.

- While the Federal Reserve is not responsible for managing the level of the U.S. dollar, its actions clearly influence currency markets. Steps in the direction of raising interest rates, even subtle ones, will tend to further strengthen the U.S. dollar, which has been increasing steadily since the summer.

American exporters will not be happy, but exports represent only 13% of U.S. GDP. This is far below the level seen in Europe and Asia. So changes in the terms of trade will not be overly damaging to the American expansion. But higher interest rates here might tempt investors to move back in this direction, at the expense of emerging markets.

As we’ve written, the Fed cannot set its policy to optimize the world’s economic performance. Nonetheless, it certainly would like to avoid the kind of “taper tantrum” that occurred early last year and created abrupt increases in long-term Treasury rates and disruptive capital flows out of emerging markets. - The FOMC often shades its decision based on its assessment of risks to the outlook. In October, the Fed saw these risks as balanced. There are some possible upsides: recent consumption gains were achieved without much additional leverage; housing has room to grow faster; and business investment has not matched the gains seen in past expansions.

On the other side, though, the U.S. is among a small handful of markets that are doing well. Given struggles in Europe, moderation in China and uncertainty in some developing markets, it may be hard to remain what Alan Greenspan once called “an island of prosperity.”

Undoubtedly, the FOMC will replace the “considerable period” passage with new language that manages expectations. While some Fed officials have hinted at a six-month time window for tightening, the Fed remains data-driven and does not want to put itself on a stopwatch.

More importantly, markets will want to hear more about how U.S. monetary policy will proceed over a longer interval. The path that follows the initial move is perhaps more important for assessing future financial conditions.

The last time the Fed went on a campaign to raise interest rates, it hiked by 25 basis points at 17 consecutive meetings. Given current fragilities and uncertainties, the pace of advance this time around could be quite a bit more measured. And the ultimate destination may not be as high. Hopefully, Chair Janet Yellen will offer a bit more on this front during the press conference that will follow the meeting next Wednesday afternoon.

So while a change of tone is in the offing, we’re still a long way from any action. And it is important to note that the economy is not going to collapse when rates start rising; policy is likely to remain very accommodative for a long time to come. Hopefully, markets will keep these things in mind.

After next week’s meeting, analysts will scrutinize all that was said for additional clues. Non-traditional metrics may also factor into the assessment; my operatives in Washington will have their cameras trained on Janet Yellen’s briefcase.

Emerging Markets: Another Year of Challenges Ahead

As we close the curtain on 2014, a sharp correction of currency values has marked the emerging market (EM) landscape. Sagging oil prices are the culprits in some places, but EM currency movements reflect a deeper economic story. Sifting through the large and diverse EM universe in a short commentary would be unwieldy, but we can identify significant trends by narrowing the focus to a few major markets.  Russia’s dire economic situation is partly due to international sanctions that are unique to that country, so we excluded it from this discussion. We chose six major EMs – Brazil, India, China, Mexico, Turkey and South Africa – to highlight recent developments.

Russia’s dire economic situation is partly due to international sanctions that are unique to that country, so we excluded it from this discussion. We chose six major EMs – Brazil, India, China, Mexico, Turkey and South Africa – to highlight recent developments.

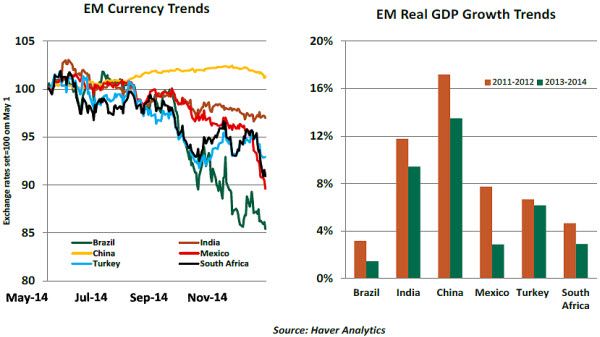

The JP Morgan Emerging Market Currency Index shows a nearly 10% drop since the high of May 2014. But the pace of depreciation across EM currencies vis-à-vis the U.S. dollar is not uniform. The Brazilian real suffered the largest correction (-13.9%), while the Indian rupee showed the smallest loss (-2.8%). The Chinese yuan’s gain (+1.2%) is the only exception in this group.

Economic fundamentals of these EMs shed light on the causes for the EM currency sell-off. Most importantly, there has been a noticeable deceleration of growth since the beginning of 2013. Without exception, real GDP growth has slowed in each of these six major EMs, and this kind of deceleration can put currencies under pressure.

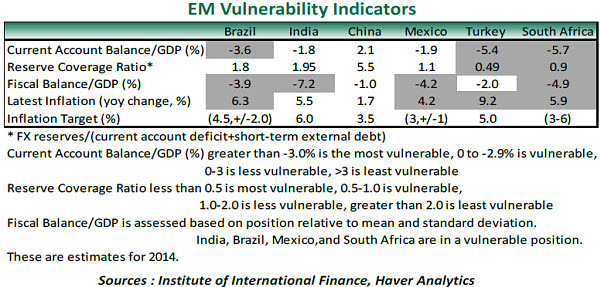

Looking beyond headline GDP, we compiled a small set of economic indicators (see table) to get a richer understanding of the reasons behind the depreciation of EM currencies. Here are four key takeaways.

First, EMs with problematic trade deficits and budget deficits are more vulnerable than others. Oil and commodity exporters feel a special pinch at the moment because they rely on energy revenues to finance government programs.

EMs with foreign exchange reserves that adequately cover the current account deficit are in a stronger position than others with lean foreign exchange reserves. The reserve coverage ratio of the International Institute of Finance captures this information succinctly (see table).

Much of the external borrowing done by governments and companies in emerging markets is denominated in U.S. dollars, which creates an additional challenge. The latest quarterly review of the Bank of International Settlements notes that loans of international banks to EMs amounted to $3.1 trillion in mid-2014, mainly in dollars. Also, three-quarters of the $2.6 trillion of international debt securities issued by EMs are in dollars.

Much of the external borrowing done by governments and companies in emerging markets is denominated in U.S. dollars, which creates an additional challenge. The latest quarterly review of the Bank of International Settlements notes that loans of international banks to EMs amounted to $3.1 trillion in mid-2014, mainly in dollars. Also, three-quarters of the $2.6 trillion of international debt securities issued by EMs are in dollars.

As EM currencies depreciate vis-à-vis the dollar, their debt service costs will escalate and EM debtors could be under severe duress. This will result in EM debtor firms scaling back spending and employment, thereby initiating a downswing in economic activity. In other words, the foreign currency liabilities of EMs present a risk to the well-being of the global economy through direct and indirect channels.

Third, actual inflation in several EMs exceeds the inflation target of their respective central banks. The recent reduction in oil prices is a boon to oil-importing EMs, as it will contain headline inflation. But for others, monetary tightening will be needed to contain inflation, and could create additional hardships.

Fourth, the diversity of goods and services EMs produce offers a cushion to swings in exports and imports of these economies. Understanding the texture of what countries bring to world markets is critical to assessing the stability of an emerging market. For example, India’s service exports help cushion the blow that country feels when commodities markets realign.

Developing countries have been a tremendous source of global economic progress over the last generation. And over that long length of time, participating in their success has enriched investors. But many EMs remain vulnerable to the volatility in global markets, which can reveal (and exacerbate) internal weaknesses. The failure to manage these makes certain countries vulnerable to the loss of capital, which has been trickling away in recent months. Let’s hope the trickle doesn’t turn into a destabilizing flood.

Recommended Content

Editors’ Picks

AUD/USD stands firm above 0.6500 with markets bracing for Aussie PPI, US inflation

The Aussie Dollar begins Friday’s Asian session on the right foot against the Greenback after posting gains of 0.33% on Thursday. The AUD/USD advance was sponsored by a United States report showing the economy is growing below estimates while inflation picked up. The pair traded at 0.6518.

EUR/USD mired near 1.0730 after choppy Thursday market session

EUR/USD whipsawed somewhat on Thursday, and the pair is heading into Friday's early session near 1.0730 after a back-and-forth session and complicated US data that vexed rate cut hopes.

Gold soars as US economic woes and inflation fears grip investors

Gold prices advanced modestly during Thursday’s North American session, gaining more than 0.5% following the release of crucial economic data from the United States. GDP figures for the first quarter of 2024 missed estimates, increasing speculation that the US Fed could lower borrowing costs.

Bitcoin price continues to get rejected from $65K resistance as SEC delays decision on spot BTC ETF options

Bitcoin (BTC) price has markets in disarray, provoking a broader market crash as it slumped to the $62,000 range on Thursday. Meanwhile, reverberations from spot BTC exchange-traded funds (ETFs) continue to influence the market.

Bank of Japan expected to keep interest rates on hold after landmark hike

The Bank of Japan is set to leave its short-term rate target unchanged in the range between 0% and 0.1% on Friday, following the conclusion of its two-day monetary policy review meeting for April. The BoJ will announce its decision on Friday at around 3:00 GMT.