It’s always wise to prepare for significant transitions well in advance. Consider the logistics of buying a house, sending a child to college, or retiring: each can be years in the planning.

The Federal Reserve has been thinking for a long time about the potential transition to less-accommodative monetary policy. The preparation is well-warranted, even though the first step in the process may not occur “for a considerable time.” With its balance sheet at an unprecedented size, interest rates at zero and new tools to be employed, there is no map for the road that lies ahead.

The statement that emerged from the September meeting of the Federal Open Market Committee (FOMC) was substantially unchanged from prior editions, and Fed Chair Janet Yellen revealed little during her press conference about the potential timing of interest rate hikes.

Overshadowed by other meeting materials was a statement on “Policy Normalization Principles and Plans” The announcement was the culmination of discussions that began at the Fed some time ago. It provides an outline of the Fed’s strategy for draining reserves from the financial system when the time comes.

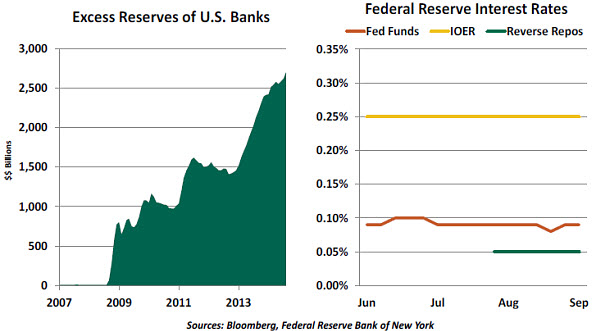

Historically, the Federal Reserve has used one primary interest rate to manage credit in the economy: the federal funds rate, at which banks lend money to each other. Recently, though, there have been two important additions to the collection. Since 2008, the Fed has been paying an interest rate to banks on excess reserves (IOER) held at the central bank. These balances have mushroomed in the last six years as a result of the Fed’s quantitative easing program.

The hope has certainly been that these monies would be lent, but modest credit demand and a desire to conserve capital have led banks to settle for the 25 basis points currently paid by the Fed on excess reserves.

Even more recently, the Fed initiated a program under which it takes in funding and pledges the securities it owns as collateral. This is known as a reverse repurchase agreement (reverse repo). The transaction is typically for a short time, and the lender earns a rate of interest on the money. The instrument is common in the financial industry, but its use by central banks is new.

So instead of one rate to pay attention to, we now have to watch three. As shown in the chart above, the IOER and the reverse repo rate form a corridor for the Federal funds rate. This pattern is expected to persist when the exit strategy begins, with the upper and lower bounds set in a manner that attempts to control volatility.  On the surface, this outline sounds promising. But it is untried. Two of the three components have never been through a rising interest rate cycle, so there isn’t any history with which to calibrate their administration.

On the surface, this outline sounds promising. But it is untried. Two of the three components have never been through a rising interest rate cycle, so there isn’t any history with which to calibrate their administration.

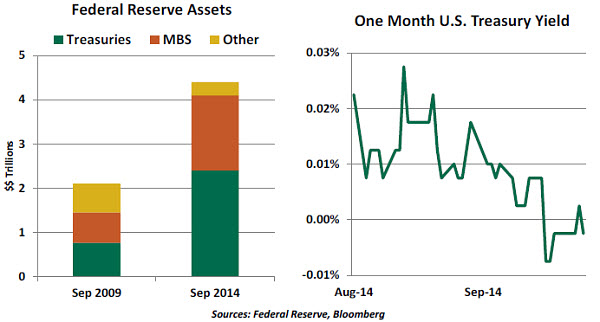

The reverse repo program is perhaps the most uncertain element. Introduced just this past summer on an experimental basis, the construct has an intelligent design. The Fed is planning to keep a very large balance sheet for a long time; its communiqué indicated that its securities holdings would be reduced “in a gradual and predictable manner primarily by ceasing to reinvest repayments of principal.”

The statement made special mention of its intent to avoid sales of its mortgage-backed securities. With housing activity tepid, the Fed likely wishes to keep the cost of credit to this sector low. (One of the Fed governors expressed reservations about this tack, as it tends to favor one industry over others.)

Using the securities as collateral instead of selling them drains reserves without risking the market disruption that might accompany portfolio liquidation. And participants in the reverse repo program would have the security of the central bank as a counterparty, which also minimizes the capital they’ll be required to hold against the transactions.

Some have worried, though, that the reverse repo program might become too popular. If concern arises over the health of institutions in the private sector, funds might rush to the Fed and create dangerous dislocations of liquidity. To address this, the Fed announced that it was placing a $300 billion cap on the program.  Restricting supply has a downside, though. Demand for reverse repos exceeded the amount offered at the end of June, and we’re seeing the same phenomenon as September 30 approaches. Stopped out of the reverse repo facility, banks are crowding into other very low-risk assets, pushing some short-term Treasury rates into negative territory. This condition will likely ease after quarter’s end, but it illustrates how challenging it will be for the Fed to set the parameters of its programs in a more-dynamic environment.

Restricting supply has a downside, though. Demand for reverse repos exceeded the amount offered at the end of June, and we’re seeing the same phenomenon as September 30 approaches. Stopped out of the reverse repo facility, banks are crowding into other very low-risk assets, pushing some short-term Treasury rates into negative territory. This condition will likely ease after quarter’s end, but it illustrates how challenging it will be for the Fed to set the parameters of its programs in a more-dynamic environment.

Again, it may be a while before the Fed is called on to transition from beta testing to live application. But when it does, the stakes will be high. The process of normalization must not undermine the economic expansion, roil the financial markets or prompt capital dislocation across the globe. The communication and execution of the exit strategy will be complicated. We’ll have to watch more variables and potentially cope with more variability.

China: A Failure to Communicate

A key element of the fine art of policymaking is establishing positions through simple actions and carefully worded statements. As an example, the interplay of central bankers and markets is an ongoing interpretation of each other’s moves that, ideally, minimizes uncertainty. In China, however, policymaking seems to have lost these subtleties. If not regained, this lack of tact may become detrimental to the country’s fragile outlook.

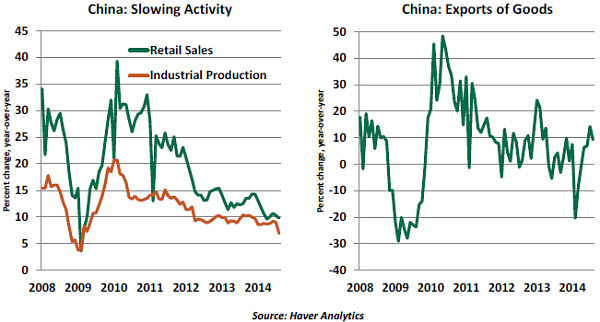

The Chinese economy is slowing. Confidence is waning, and uncertainty about the future is on the rise. Growth in industrial production is at a five-year low, retail sales growth is slumping toward decade-lows, and exports continue to struggle.

The government may be talking about a steady deceleration to a new normal of economic growth, one which is better balanced and less reliant on artificial stimulus. But it is not offering a credible outline for how China will reach this state. Markets are without guidance and increasingly unable to place disappointing indicators into any positive perspective.

Another point also playing on the minds of the markets is the real estate “bubble” – a word the government abhors. For years, Beijing has tried to implement delicate measures to deter the massive inflation of home values, including restrictions on credit growth, all without actually acknowledging market fears that a bubble exists. This did not deter expansion but rather created the groundwork for the now-extensive shadow banking system, which is another issue policymakers have not tackled head-on.  Now, with growth slowing and concerns rising about defaults in real estate, the government is seemingly reversing course. Incentives to allow people to purchase second homes at advantageous interest rates are under discussion. Last week, the Peoples Bank of China (PBoC) put 500 billion yuan (US$81 billion) of three-month loans into the markets through the top five banks. Analysts interpreted it as a de facto easing, equivalent to a 50-basis-point cut to the reserve ratio; money markets considered it a hike in liquidity to promote further lending.

Now, with growth slowing and concerns rising about defaults in real estate, the government is seemingly reversing course. Incentives to allow people to purchase second homes at advantageous interest rates are under discussion. Last week, the Peoples Bank of China (PBoC) put 500 billion yuan (US$81 billion) of three-month loans into the markets through the top five banks. Analysts interpreted it as a de facto easing, equivalent to a 50-basis-point cut to the reserve ratio; money markets considered it a hike in liquidity to promote further lending.

Even after the PBoC explained it was an assurance of available liquidity in the run-up to quarter-end, upcoming holidays and significant IPOs, the markets pursued their own interpretations. Clearly, the process of policy communication broke down.

Amid increasing failures of wealth management products and rumors of loan rollovers to avoid default, it is understandable why markets see the PBoC as saying one thing and doing another. The PBoC has called its recent actions “targeted policy fine-tuning,” but the markets are hardly satisfied. Adding to the suspicion is speculation that the governor of the PBoC, a noted reformer, might soon be replaced.

So, how does all of this play into China’s outlook? In a nutshell, not favorably. This failure of the People’s Bank to fill the information void leaves room for doubt and uncertainty to dampen sentiment and weigh on confidence. These factors could then play into the real area of concern – the health of the financial industry.

At a time when the PBoC wants to increase credit generation to support its economic fine-tuning efforts, credit growth is at its slowest since 2005. A downturn in market confidence could be part of the reason people are not borrowing, but a further deterioration in sentiment would definitely run counter to the bank’s intentions of boosting the economy. Government stimulus has been ruled out for the time being (it is seen as the reason the country is having such problems), but if the situation gets worse, policymakers will not rule out any tool if it brings near-term stability.

The best remedy would, of course, be for the PBoC to make a very clear case about the country’s economic trajectory in a way that addresses standing concerns and provides a Chinese-style forward guidance. But that is the problem with communication – if not credible, it confuses instead of clarifying.

Central Bank Policy: Time for Dissents

The Federal Reserve and the Bank of England (BoE) are expected to tighten monetary policy in the months ahead, while the European Central Bank (ECB) could consider additional monetary accommodation. At these inflection points for policy, dissents among members of the policymaking committees are emerging. This is not at all unusual, but the task of reaching consensus behind decisions is becoming more challenging.

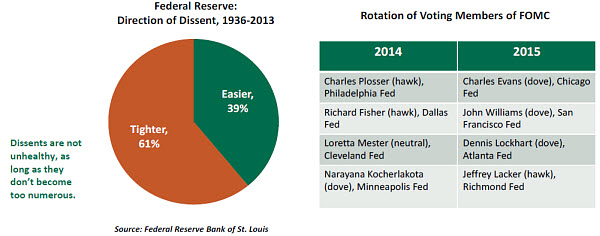

FOMC members cast three dissents in the last two meetings in favor of raising the policy rate. Some have wondered whether this number will multiply as we move into next year. A recent study from the St. Louis Fed showed that dissents from Federal Reserve decisions have historically favored tighter policy, which is likely to get careful consideration in the months ahead.

It bears noting that the annual FOMC voting rotation in 2015 shifts the composition of the voting members slightly toward the dovish camp. (“Doves” are typically concerned about the unemployment mandate, while “hawks” worry about inflation.)

On the other side of the Atlantic, two members of the rate-setting committee of the BoE dissented at the August and September 2014 meetings. Differences about rate-setting are not new, as BoE records indicate that there was at least one dissent at 44% of its Monetary Policy Committee meetings since June 1997.

The ECB is tight-lipped about voting patterns of its decisions. This could change when minutes of meetings will be published 2015 onward, but it is not clear if the identity of dissenting voters will be disclosed. Mario Draghi was forthcoming when he noted that the decisions at the last meeting were not unanimous.

Dissents can be a sign of thorough evaluation before monetary policy is set. But too much dissent can rattle financial markets. The trick for central bank leadership is to find a balance between the two.

Recommended Content

Editors’ Picks

EUR/USD clings to daily gains above 1.0650

EUR/USD gained traction and turned positive on the day above 1.0650. The improvement seen in risk mood following the earlier flight to safety weighs on the US Dollar ahead of the weekend and helps the pair push higher.

GBP/USD recovers toward 1.2450 after UK Retail Sales data

GBP/USD reversed its direction and advanced to the 1.2450 area after touching a fresh multi-month low below 1.2400 in the Asian session. The positive shift seen in risk mood on easing fears over a deepening Iran-Israel conflict supports the pair.

Gold holds steady at around $2,380 following earlier spike

Gold stabilized near $2,380 after spiking above $2,400 with the immediate reaction to reports of Israel striking Iran. Meanwhile, the pullback seen in the US Treasury bond yields helps XAU/USD hold its ground.

Bitcoin Weekly Forecast: BTC post-halving rally could be partially priced in Premium

Bitcoin price shows no signs of directional bias while it holds above $60,000. The fourth BTC halving is partially priced in, according to Deutsche Bank’s research.

Week ahead – US GDP and BoJ decision on top of next week’s agenda

US GDP, core PCE and PMIs the next tests for the Dollar. Investors await BoJ for guidance about next rate hike. EU and UK PMIs, as well as Australian CPIs also on tap.