Thirty years ago, Japan was in the ascendance, and America seemed to be falling back. The Rising Sun was taking control of steel, electronics, autos and banking. I recall attending a modern adaptation of “The Mikado” back then; instead of lovable 19th-century Japanese bureaucrats, the players were salarymen intent on world dominance.

To keep pace, Americans were encouraged to follow the Japanese example. Feedback circles were formed, and cooperative competition was fostered. Eventually, the performance gap between the countries closed, but not because we caught up. After flying high, Japan suffered a dramatic fall that kept it grounded for two decades. Viewed with hindsight, practices that propelled the country forward eventually paved the path to privation. The Japanese experience remains instructive, but no longer is it the object of admiration.

The eurozone’s recent struggles have reached a point where some analysts are concerned that a Japan-style scenario might lie ahead. A review of that experience, and an evaluation of how today’s European condition might compare, seem in order.

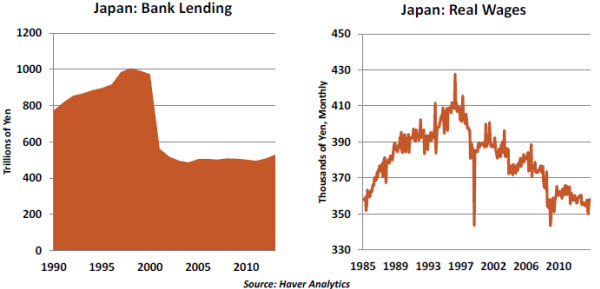

The details of Japan’s correction are alarming. Real economic growth has averaged less than 1% annually since 1990. Equity markets are still at less than half the peak recorded 25 years ago. A crippling deflation set in and proved very difficult to dislodge.

Many measures suggest that the eurozone may be at risk for the same fate. For a number of years after the euro was introduced, the region was prosperous. But there have been two recessions since 2008, and growth in the area seems to have stalled once again. Aggregate inflation across the 18 countries that share the common currency is only 0.3% over the past 12 months. Inflation expectations in Europe are beginning to follow actual readings downward.

Both Japan and the eurozone had real estate excesses that corrected severely, leaving local financial institutions with substantial pools of bad assets. In both cases, banking authorities were less than aggressive at acknowledging the problems and cleaning them up. The resulting burden of bad debt led to a deep curtailment of credit that served to deepen the malaise.

Both situations were complicated by structural issues that make economic adjustment difficult. Labor market rigidity and restrictive business regulation delayed the necessary correction in Japanese real wages. Those wages are still in decline. High public debt levels has an influence on the degree of fiscal stimulus that can be applied.  Both central banks took a long time to make a strong commitment to accommodation. The Bank of Japan first cut its overnight rates to zero in 1999 but then prematurely raised them twice before finally leaving them alone. Japan also implemented a modestly sized program of quantitative ease but did not stick to it long enough to realize the full benefit.

Both central banks took a long time to make a strong commitment to accommodation. The Bank of Japan first cut its overnight rates to zero in 1999 but then prematurely raised them twice before finally leaving them alone. Japan also implemented a modestly sized program of quantitative ease but did not stick to it long enough to realize the full benefit.

So does this doom the eurozone to repeat this ignominious history? Not necessarily. While deflation has set in in some countries, inflation expectations are still solidly in positive territory. It is the expectation of inflation that can be more pernicious, deterring consumption and inflating the real value of debts.  Europe has its demographic challenges, but they are nothing compared to Japan’s. (Sales of adult diapers now exceed sales of baby diapers there.) Higher birth rates and immigration should keep Europe’s labor force more vital in the years ahead. Europe certainly has its political challenges, but the Japanese structure (which still gives disproportionate power to rural interests) was not ideally designed to respond to crisis.

Europe has its demographic challenges, but they are nothing compared to Japan’s. (Sales of adult diapers now exceed sales of baby diapers there.) Higher birth rates and immigration should keep Europe’s labor force more vital in the years ahead. Europe certainly has its political challenges, but the Japanese structure (which still gives disproportionate power to rural interests) was not ideally designed to respond to crisis.

The key to getting the eurozone’s path to diverge from Japan’s is aggressive policy in several areas.

- Scholars, including then-future Federal Reserve Chairman Ben Bernanke, studied the causes of the Japanese correction and proposed policy steps to arrest the downward spiral of decline, deflation and debt. In a landmark 2002 speech, Bernanke foreshadowed some of the nontraditional monetary tools that he would ultimately employ six years later to head off a similar fate in the United States.

- The strategy, in sum: go big, go fast and stick to it. Changing perceptions – and quickly – is key to keeping disappointing conditions from being seen as the new normal. Steps taken by Mario Draghi and the European Central Bank (ECB) this week may begin to turn the tide.

- Getting losses out into the open and recapitalizing the banking system are essential early steps for dealing with crisis. Japan dithered, and Europe has been dithering. But the ECB’s asset quality review/stress test, results of which will be released next month, represents a golden opportunity to reckon with problems and reopen credit channels.

- Speeding market adjustment, however painful, is better than delaying and praying. This is true of real estate, equities and labor. Is Europe ready for the reforms that would allow a new equilibrium to set in? In some places, the answer seems to be yes; in others ….

So there is still time for the eurozone, but that should be a call to action and not cause for complacency. Continued policy failures will, in the words of the Mikado, find the punishment fitting the crime.

U.S. August Employment Data: Somewhat Disappointing

This month’s report from the Labor Department did not live up to its predecessors, but we continue to believe that job creation will progress nicely during the balance of the year. That said, today’s news will make decision-making easier for the Federal Reserve later this month.

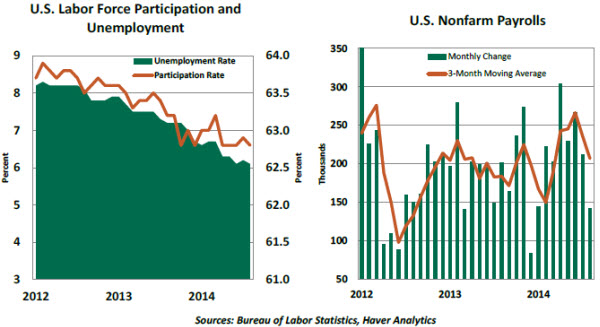

The unemployment rate inched down to 6.1% in August from 6.2% in the prior month, reflecting the decline in the participation rate (62.8% from 62.9%). For the most part, the participation rate is unchanged over the past five months, while the unemployment report shows a decline in this period. We are tracking this relationship closely. Updated research from the Fed suggests that demography explains a major part of the recent decline in the participation rate. But it is not the only reason, as other economic evidence suggests that cyclical factors are at play.

The number of part-time workers declined 234,000 to 7.27 million during August. The broad measure of unemployment – which includes part-time employment and marginally attached workers – fell to 12.0% from 12.2% in the prior month. The number of long-term unemployed (unemployed for 27 weeks or more) dropped to 31.2% of the total unemployed, down from 32.9% in July and 34.6% three months ago. These measures are part of Fed Chair Janet Yellen’s dashboard.

Payroll employment increased 142,000 in August, and revisions resulted in 28,000 fewer jobs in the June-July period. The modest hiring pace reduces the three-month moving average to 207,000 from the stronger readings seen in the past four months.  In the goods-producing sector, construction employment (+20,000) advanced while factory payrolls were unchanged, following two months of strong gains. The timing of auto industry layoffs and recalls in the summer often results in wide swings in auto sector hiring. So we should not read too much into this result.

In the goods-producing sector, construction employment (+20,000) advanced while factory payrolls were unchanged, following two months of strong gains. The timing of auto industry layoffs and recalls in the summer often results in wide swings in auto sector hiring. So we should not read too much into this result.

In the services sector, payrolls increased only 112,000 compared with an average gain of 182,000 in the last six months. With the exception of professional and business services (+47,000) and health care (+34,000), hiring across all other categories of service employment in August was lower than the three-month moving average. The official report indicates that a loss of 17,000 retail-sector jobs is related to the disruption of employment in a New England chain store.

The workweek has held at 34.5 hours for six straight months. Average hourly earnings rose 6 cents in August to $24.53, putting the year-to-year change at 2.1%, matching the July gain, and there is no sign of wages breaking away from this muted trend. A slightly narrower measure of earnings pertaining to production and non-supervisory workers rose 2.5% in August, showing a bit of acceleration from the prior two months. But both readings are noticeably lower than gains seen prior to the Great Recession.

Developments in the labor market are the centerpiece of Yellen’s monetary policy strategy. Focusing on elements in Yellen’s dashboard, there are improvements in place, but the tone of the August establishment survey softened a bit in August. Even though recent data such as auto sales and purchasing managers’ surveys were robust, the latest employment numbers were not. Tapering of asset purchases will continue following the September Fed meeting, while the policy statement is unlikely to include a major transformation of the Fed’s views.

Capital Spending – Room to Grow?

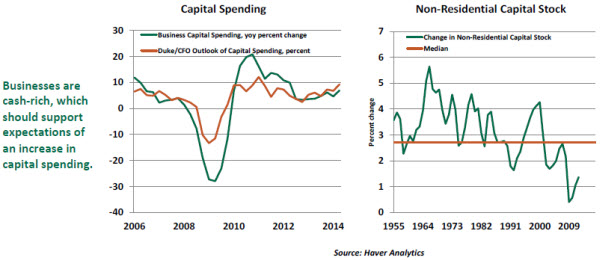

Business capital spending is a cyclical component of gross domestic product (GDP) that recovers rapidly in the early stages of an economic recovery and maintains momentum in the later stages of a business expansion. Following the Great Recession, the trend of business capital spending has been slightly different, as it posted significant gains in 2010-11 but grew at a more subdued pace in the subsequent two years. In the most recent quarter, there was a noticeable pickup in capital spending and expectations point to further gains in the rest of the year.

Surveys indicate that businesses are optimistic about capital expenditures in the near term. In the Duke/CFO Magazine survey, respondents indicated that capital expenditures are likely to grow at the fastest pace since early-2011. The Institute of Supply Management’s composite index of the manufacturing sector posted strong improvements in July and August. Indexes from both these surveys have a strong positive correlation with the equipment spending component of GDP and lead capital spending by one calendar quarter.

The low-interest-rate environment, favorable cash position of firms and positive outlook of businesses bode positively for capital spending in the near term.

Capital spending adds to stock of existing capital stock and is one of the main drivers of the nation’s productivity. Capital stock data are published with a long lag and are available only through 2012. Real non-residential fixed assets grew 1.4% in 2012. This reading is below the 40-year median of 2.7% and mean of 2.8%.

Essentially, there is room for capital spending to advance and replenish capital stock of the nation. Capital spending could be the surprise factor that gives an extra lift to GDP in the next few quarters.

Recommended Content

Editors’ Picks

EUR/USD hovers around 1.0700 ahead of German IFO survey

EUR/USD is consolidating recovery gains at around 1.0700 in the European morning on Wednesday. The pair stays afloat amid strong Eurozone business activity data against cooling US manufacturing and services sectors. Germany's IFO survey is next in focus.

USD/JPY refreshes 34-year high, attacks 155.00 as intervention risks loom

USD/JPY is renewing a multi-decade high, closing in on 155.00. Traders turn cautious on heightened risks of Japan's FX intervention. Broad US Dollar rebound aids the upside in the major. US Durable Goods data are next on tap.

Gold: Defending $2,318 support is critical for XAU/USD

Gold price is nursing losses while holding above $2,300 early Wednesday, stalling its two-day decline, as traders look forward to the mid-tier US economic data for fresh cues on the US Federal Reserve interest rates outlook.

Worldcoin looks set for comeback despite Nvidia’s 22% crash Premium

Worldcoin (WLD) price is in a better position than last week's and shows signs of a potential comeback. This development occurs amid the sharp decline in the valuation of the popular GPU manufacturer Nvidia.

Three fundamentals for the week: US GDP, BoJ and the Fed's favorite inflation gauge stand out Premium

While it is hard to predict when geopolitical news erupts, the level of tension is lower – allowing for key data to have its say. This week's US figures are set to shape the Federal Reserve's decision next week – and the Bank of Japan may struggle to halt the Yen's deterioration.