From the Suez Canal, to Japanese bullet trains, to the American interstate highway system, to the Millennium Bridge to the Three Gorges Dam, the grandeur of infrastructure is on full display the world over. Awe-inspiring and beautiful to some, these fixtures also play a critical role in the functioning of the global economy. The choices nations make in the area of infrastructure can bear critically on prosperity.

A nation’s infrastructure plays an important role in its economy by facilitating production and the movement of people, goods and ideas. Appropriate investment in infrastructure is essential to sustaining productivity. Poor transportation systems, telecommunication facilities, water treatment or electricity grids are threats to growth.

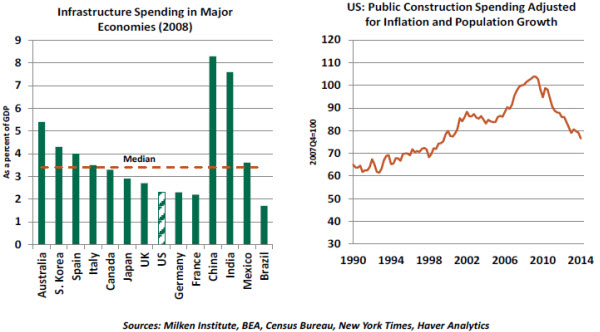

In many areas, infrastructure is not getting the attention it deserves. The McKinsey Global Institute estimates that $57 trillion will be needed to finance infrastructure around the world through 2030 to maintain present levels of gross domestic product (GDP) growth. Among the world’s major economies, China, India, Australia and South Korea are the top four nations investing in infrastructure, while others are lagging behind.

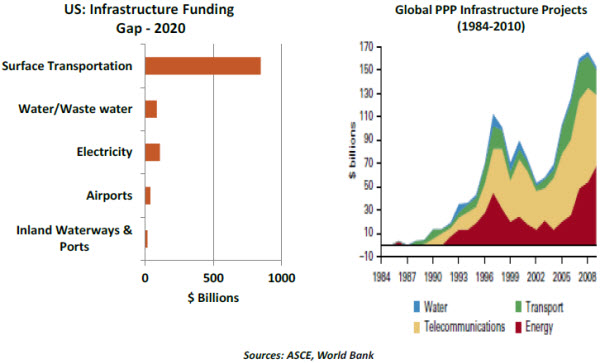

In the United States, public construction spending adjusted for inflation and population growth shows a marked decline since the peak of the previous business cycle. The American Society of Civil Engineers estimates that at current levels of public sector spending, the U.S. economy will face an infrastructure funding gap of roughly $1.1 trillion by 2020, with surface transportation estimated to face the largest shortfall.

Historically, governments have provided financial support for infrastructure through their budget processes and used tax proceeds to pay for them. Yet central and local governments worldwide face pressing budgetary constraints. The global financial crisis damaged revenues, and many regions are facing huge obligations for the health and retirement of their citizens.

This has led legislatures to defer or deny investments in infrastructure. The U.S. Congress is currently engaged in an acrimonious debate over funding the depleted highway trust fund through the balance of the year. It is disappointing that a solid long-term plan is not in place.  Unfortunately, in these times of public austerity, every line in the ledger looks like a cost to be cut. Yet certain types of spending are really investments that pay off over time in enhanced economic performance. Failing to maintain what’s in place and invest in the expansion of infrastructure can leave an economy at a disadvantage to its global competitors.

Unfortunately, in these times of public austerity, every line in the ledger looks like a cost to be cut. Yet certain types of spending are really investments that pay off over time in enhanced economic performance. Failing to maintain what’s in place and invest in the expansion of infrastructure can leave an economy at a disadvantage to its global competitors.

The McKinsey Global Institute also projects a global gap of $500 billion per year between public funds and investment needs through 2030. To fill some of the gap, public-private partnership (PPP) ventures have gained ground, and their numbers have increased significantly in Europe.

There are several factors that support this development. The long duration of infrastructure projects does not match well with the short-term focus of budget-strained governments, but they do match well with long-term investors. PPPs are subject to market discipline and are known to result in associated efficiencies. And they produce public budget optics that can help compliance with debt limits or balanced-budget rules.

Opponents of PPPs hold that profit-seeking motives of the private sector are at odds with providing public services. Fees or tolls charged by private operators of PPPs are more subtle than direct taxation, but they can still be costly. (Citizens will come to understand that private operators can often increase their rates without going through the legislative process.)

Despite the criticisms, PPPs are known to be successful in transportation, telecommunications, electricity and water projects. The use of PPPs to provide infrastructure in the United States has risen noticeably following the Great Recession. Apart from enhancing the value of infrastructure, these programs create jobs in categories that have struggled since 2008.  Overall, the combination of the growing need for infrastructure funding in the global economy and budget-constrained government agencies is the perfect nurturing ground for PPPs. But it bears noting that PPPs are complements – not substitutes – for government infrastructure projects.

Overall, the combination of the growing need for infrastructure funding in the global economy and budget-constrained government agencies is the perfect nurturing ground for PPPs. But it bears noting that PPPs are complements – not substitutes – for government infrastructure projects.

The estimated gap between investment needs and government funding in the global economy is one that needs to be closed. Infrastructure investment carries the potential to positively transform lives and nations; failing to invest will have the opposite effect.

Rules, Not Tools

We’ve tried a range of methods to get our kids to keep their rooms clean. Simply asking them to neaten up kindles debate over exactly what constitutes “neat.” Giving them specific instructions (make your bed, put laundry in the hamper) can leave blind spots (“You never told me I couldn’t leave a dirty plate under my bed for a week”). It’s maddening.

Is it best to govern by rules or by principles? This question recently popped up in the debate over the proper conduct of American monetary policy. For some, the Federal Reserve has far too much discretion. Instead, they seek legislation requiring that interest rates be set strictly by a mathematical rule. This idea was advanced in a Wall Street Journal editorial by John Taylor, the architect of the leading candidate to serve this formulaic role.

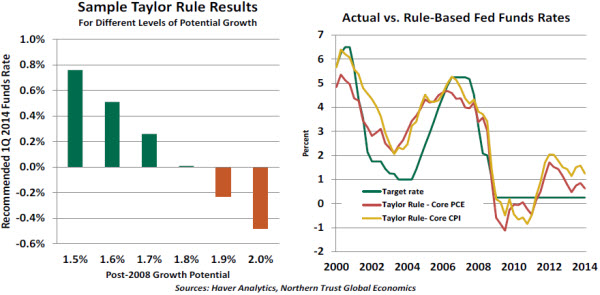

Upon close examination, though, the “Taylor Rule” is not the simple operating algorithm that its supporters suggest. Essentially, it calls for interest rates to be set on the basis of where inflation stands relative to its target and where economic growth stands relative to its potential level. When actual values are higher than desired, tighter policy is called for.

Implementing a Taylor Rule is a matter of art as well as science. Determining the long-term potential growth rate of an economy is difficult; it can vary considerably over time, based on demography and productivity. Just a small variance in this assumption can yield significantly different prescriptions.

Further, the actual data required by the Taylor Rule is far from perfect. As we discussed in last week’s View from Here on economic data, revisions and rebasings can dramatically change the reported course of business activity. Since monetary policy must be made in real time, a decision taken today using a formula could look very unwise in a month or two. And which inflation rate should you choose for the calculation? Different indicators suggest very different levels for overnight interest rates in the Taylor formula.

Further, the actual data required by the Taylor Rule is far from perfect. As we discussed in last week’s View from Here on economic data, revisions and rebasings can dramatically change the reported course of business activity. Since monetary policy must be made in real time, a decision taken today using a formula could look very unwise in a month or two. And which inflation rate should you choose for the calculation? Different indicators suggest very different levels for overnight interest rates in the Taylor formula.

The Taylor Rule has a series of other challenges to overcome:

- It doesn’t work well when interest rates have reached the zero nominal bound. It is hard to factor unconventional tools like quantitative ease or forward guidance into the equation.

- It makes no allowance for financial conditions. The amount of stimulus or restraint produced by a given level of interest rates is dependent on credit flows within an economy. These can sometimes be overly ample or constricted.

- It does not take a forward view. The formula uses actual GDP growth, which is backward-looking. No allowance is made for potential acceleration or deceleration of output in the period ahead.

- It may not take account of risks in the environment. Using point estimates instead of distributions of outcomes prevents monetary policy from leaning in a manner that is sensitive to perceived vulnerabilities.

Broadly stated, using a Taylor Rule requires a great deal of judgment. This would appear to make such a regime seem much more principles-based than its adherents would concede.

All of this said, Taylor rules are (and should be) an important input to monetary decisions. The Federal Reserve calculates a number of different Taylor outcomes as background for its deliberations. Janet Yellen has cited them favorably in speeches. But using them exclusively would seem to be limiting and potentially dangerous.

As a final thought, movements by Congress to become more engaged in the governance of the Federal Reserve threaten the independence of central banking, which has been so important to American economic and market performance over the past generation. Given the low marks the legislature has received for its recent conduct of fiscal policy, Congress might want to focus its energies inward instead.

Brazil: Back to Reality

Over the past five weeks, millions around the world were glued to their televisions as they followed the FIFA World Cup in Brazil. Nail-biting finishes, early upsets and spectacular goals provided plenty to celebrate. Even better, the drama largely stayed on the field, as the anticipated logistical glitches and disruptive protests failed to emerge. Yet after Brazil’s stunning 7-1 semifinal loss to Germany, the host nation’s joy quickly turned to whistles of disapproval. Brazilians looking at their economy won’t find much to cheer about either.

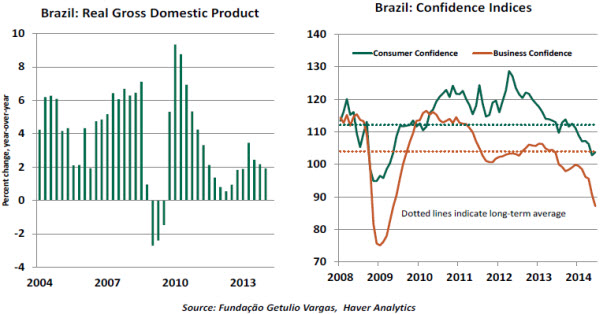

Latin America’s largest economy is stuck in a rut. After booming from 2004 – 2010 with average GDP growth of 4.5%, the economy is headed toward disappointment for the fourth straight year. Inflation has once again climbed above the central bank’s 6.5% target ceiling despite 375 basis points of interest rate hikes since early 2013. Elevated debt levels and rising interest rates have households holding back, while businesses are curtailing investment due to uncertainty over economic policy. Business and consumer confidence are at their lowest since the financial crisis. Despite a bump from the World Cup, second-quarter 2014 growth will likely be negative. The result is annual GDP growth of just 1.0% in 2014 and 1.5% in 2015, according to consensus forecasts.

Many are pointing the finger at President Dilma Rousseff of the Worker’s Party, who is running for re-election in October. Her four years at the helm have been marked by increased economic intervention, creative accounting in public finances and an inability to tackle structural challenges through reform. Last summer’s street demonstrations confirmed mounting frustration over government waste and poor public services.

Rousseff continues to lead the polls ahead of elections, but her advantage has dwindled. Her main challenger is Senator Aécio Neves, the Brazilian Social Democracy Party candidate whose more investor-friendly approach has the backing of the business community. Latest polling points to a second round runoff, with Rousseff gaining 46% over Neves’ 39%. But Brazil’s economic malaise could turn the table.

A Neves victory would likely boost business sentiment, but a tough road lies ahead regardless of the election results. With the public sector deficit set to balloon to nearly 5% of GDP this year, a tough fiscal adjustment looms. Deeper tax and labor reforms are desperately needed to improve competitiveness. Yet without a strong mandate, neither candidate is likely to push unpopular legislation through the fractious parliament. Without the political will to address these and other structural issues, Brazil will stay trapped in a dynamic of low growth and high inflation.

In less than two years, the Olympic Games will open in Rio de Janeiro. Brazil will be hoping for better results in that competition and in its economy as 2016 approaches.

Recommended Content

Editors’ Picks

AUD/USD posts gain, yet dive below 0.6500 amid Aussie CPI, ahead of US GDP

The Aussie Dollar finished Wednesday’s session with decent gains of 0.15% against the US Dollar, yet it retreated from weekly highs of 0.6529, which it hit after a hotter-than-expected inflation report. As the Asian session begins, the AUD/USD trades around 0.6495.

USD/JPY finds its highest bids since 1990, approaches 156.00

USD/JPY broke into its highest chart territory since June of 1990 on Wednesday, peaking near 155.40 for the first time in 34 years as the Japanese Yen continues to tumble across the broad FX market.

Gold stays firm amid higher US yields as traders await US GDP data

Gold recovers from recent losses, buoyed by market interest despite a stronger US Dollar and higher US Treasury yields. De-escalation of Middle East tensions contributed to increased market stability, denting the appetite for Gold buying.

Ethereum suffers slight pullback, Hong Kong spot ETH ETFs to begin trading on April 30

Ethereum suffered a brief decline on Wednesday afternoon despite increased accumulation from whales. This follows Ethereum restaking protocol Renzo restaked ETH crashing from its 1:1 peg with ETH and increased activities surrounding spot Ethereum ETFs.

Dow Jones Industrial Average hesitates on Wednesday as markets wait for key US data

The DJIA stumbled on Wednesday, falling from recent highs near 38,550.00 as investors ease off of Tuesday’s risk appetite. The index recovered as US data continues to vex financial markets that remain overwhelmingly focused on rate cuts from the US Fed.