The mid-year review round was not kind to us. Last December, we forecast that real U.S. gross domestic product (GDP) would grow at an annual pace of just under 3% during the first half of the year. It now looks like the initial six months will show no growth in real GDP.

We had all of our excuses ready: bad winter weather, tough new mortgage lending rules, the dog ate our model, etc. But our bosses were not entirely sympathetic. We’ve been given six months to set things right … or else!

With a temporary reprieve in hand, we’ve scurried to analyze what’s happened and update expectations for what’s ahead. As one byproduct of the process, we thought we’d share some of the things that have surprised us the most so far in 2014.

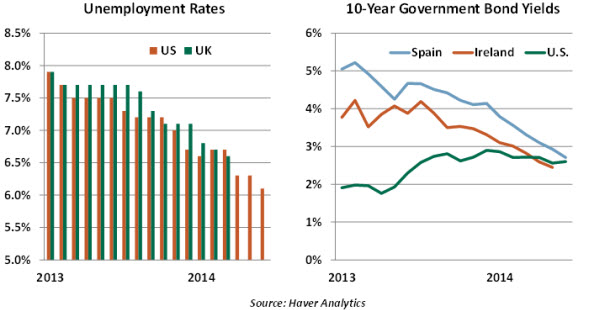

- Unemployment has fallen remarkably quickly in the United States and the United Kingdom. Last year, the Federal Reserve and the Bank of England established targets for joblessness that would initiate discussion of tighter policy; these levels were reached many months earlier than projected.

There are certainly pockets of slack left in labor markets: part-time employees who would like full-time jobs, discouraged workers who have stopped searching, and even retirees who might be lured back into the workplace. But the speed at which jobless rates are approaching levels associated with full employment will cause forecasters and central banks to recalibrate their expectations.

- Counter to the expectations of many, long-term interest rates have fallen sharply this year. And there has been a surprising convergence between the rates paid by sovereigns with very different credit standing. Yields in Europe’s periphery have certainly benefitted from renewed easing on the part of the European Central Bank (ECB). And some countries have made tremendous progress toward getting their fiscal houses in order.

But one is left wondering whether something is wrong with the right-hand picture above. Why should Ireland be able to borrow more cheaply than the United States? Monetary accommodation across the globe has initiated a search for yield, and government debt once thought to be risky is now viewed as an opportunity. Hopefully, the newfound confidence of investors proves justified. - Housing has turned from a welcome driver of recovery into a global problem. Hurt more deeply than almost any other industry, real estate showed a “V-shaped” recovery thanks to very low interest rates. But advances in construction seem to have stalled a bit, while prices have continued to rise. And the market has become very bifurcated, with high-end property in key cities doing extraordinarily well while first-time homebuyers are shut out.

It will be difficult to even things out without going back to the homeownership promotion that paved the way for the 2008 crisis. The high end is viewed as potential evidence of financial excess by many policy makers, who have implemented a series of taxes and rules in an attempt to curb the enthusiasm. This sector may ultimately prove whether these kinds of “macroprudential” strategies can effectively address asset price excesses.

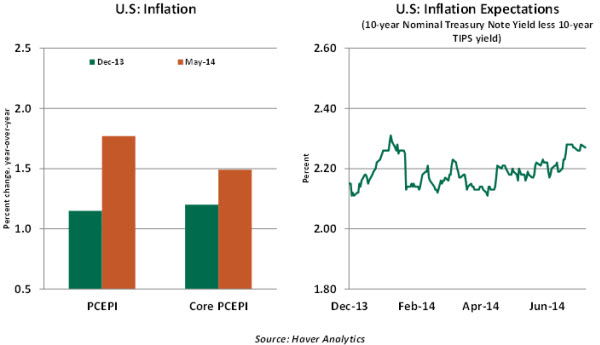

It will be difficult to even things out without going back to the homeownership promotion that paved the way for the 2008 crisis. The high end is viewed as potential evidence of financial excess by many policy makers, who have implemented a series of taxes and rules in an attempt to curb the enthusiasm. This sector may ultimately prove whether these kinds of “macroprudential” strategies can effectively address asset price excesses. - U.S. inflation has risen more rapidly than expected. The personal consumption expenditure price index (PCEPI) has risen quite a bit more briskly at the overall and core levels since December 2013.

Geopolitical issues have pressed energy prices higher, and drought is partly to blame for higher food prices. We can certainly hope that these challenges ease in the months ahead. Among the core items, which exclude food and energy, rental and health care costs show a noticeable increase. Inflation expectations have risen slightly in the past few months but remain well-anchored.

Although inflation is creeping up, it is still below the Fed’s 2% target. Fed rhetoric suggests that normalization of interest rates will not occur until wage gains are much stronger than the current, very subdued trend. The theme of the annual Federal Reserve symposium at Jackson Hole in August is “Re-Evaluating Labor Market Dynamics.” Is it only a matter of coincidence? - Markets have been faced with a significant string of international incidents so far this year. Russia’s annexation of Crimea, the military coup in Thailand, and Iraq’s seeming descent into civil war are just a few of the significant events that have earned headlines so far in 2014. Each situation has some specific economic implications, and reminds us that there are risks to the outlook.

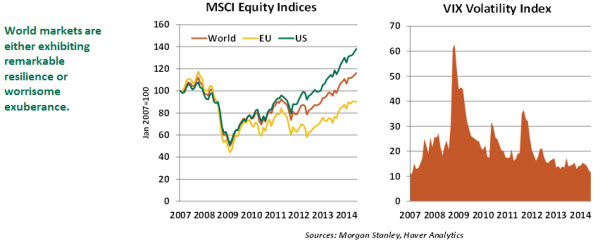

In spite of these periodic alerts, world asset prices continue to soar. The Dow Jones average recently closed above 17,000 for the first time and measures of market volatility remain very low. An optimist would say that we’ve simply gotten better at rolling with punches. A pessimist would say that we may be setting ourselves up for a significant correction. - The ECB is finally walking the walk. After using an open mouth policy for many months as its primary strategy for combatting disinflation, eurozone monetary authorities have become more active and aggressive. It was not a complete surprise to see short term rates breach the zero nominal bound, but it was a dramatic step for a major central bank. The ECB’s discussion of potential quantitative ease seems to be accelerating as well.

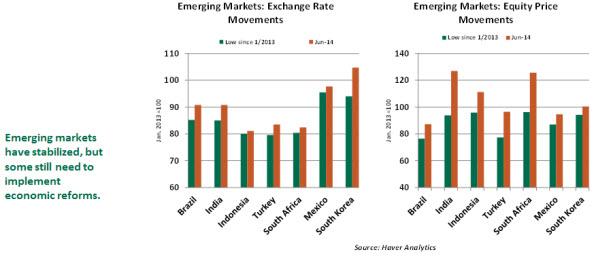

A key for the second half of the year is the asset quality review and stress test being applied to the eurozone’s banks. If handled well, the reckoning could be a very constructive step towards financial rehabilitation. If not handled well, it could add to the uncertainty over Europe’s economic future. - Emerging markets have rebounded somewhat more quickly so far this year than some anticipated. The extraordinarily easy monetary policy in advanced economies after the outbreak of the global financial crisis led to a global search for yield. Emerging markets were the beneficiaries of these capital flows. This trend was disrupted after former chairman Ben Bernanke’s May 2013 remarks indicating the Fed’s intention to commence tapering of asset purchases, which led to corrections in emerging market exchange rates and equity prices.

Capital flows to emerging markets have resumed. Although the timing and magnitude of improvement varies, currency values and equity prices have retraced a large part of the initial losses despite the execution of the Fed’s tapering program. Countries with strong economic conditions, less oppressive external balances, and appropriate monetary and fiscal policy actions have fared better. Those that lag must continue to restructure themselves. - Debate over the fiscal problems of the United States has been surprisingly quiet. We are grateful to have a break from the acrimony.

Unfortunately, there remain substantial long-term imbalances that need to be addressed, and silence is not a solution. Nothing is likely to get done before the mid-term elections in November, but things may get back to a boil quickly thereafter. The suspension of the debt ceiling ends next February, shortly after the new Congress is seated.

It’s very likely that there will be a whole new set of surprises that will challenge our sensibilities and our forecasts during the balance of 2014. We hope our readers and our bosses will understand that we cannot control economic policy and world events. But we will continue trying to make sense of shifts in these areas as they occur.

Recommended Content

Editors’ Picks

AUD/USD could extend the recovery to 0.6500 and above

The enhanced risk appetite and the weakening of the Greenback enabled AUD/USD to build on the promising start to the week and trade closer to the key barrier at 0.6500 the figure ahead of key inflation figures in Australia.

EUR/USD now refocuses on the 200-day SMA

EUR/USD extended its positive momentum and rose above the 1.0700 yardstick, driven by the intense PMI-led retracement in the US Dollar as well as a prevailing risk-friendly environment in the FX universe.

Gold struggles around $2,325 despite broad US Dollar’s weakness

Gold reversed its direction and rose to the $2,320 area, erasing a large portion of its daily losses in the process. The benchmark 10-year US Treasury bond yield stays in the red below 4.6% following the weak US PMI data and supports XAU/USD.

Bitcoin price makes run for previous cycle highs as Morgan Stanley pushes BTC ETF exposure

Bitcoin (BTC) price strength continues to grow, three days after the fourth halving. Optimism continues to abound in the market as Bitcoiners envision a reclamation of previous cycle highs.

US versus the Eurozone: Inflation divergence causes monetary desynchronization

Historically there is a very close correlation between changes in US Treasury yields and German Bund yields. This is relevant at the current juncture, considering that the recent hawkish twist in the tone of the Federal Reserve might continue to push US long-term interest rates higher and put upward pressure on bond yields in the Eurozone.