One afternoon in the summer of 2010, I had a meeting planned with a colleague in the Federal Reserve’s economic research division. I went up to his office at the appointed hour but found it empty.

From across the floor, I heard shouting coming from the seminar room. That, in itself, was not out of the ordinary. Fed researchers take their subjects very seriously; authors who survive the crucible of the seminar room will typically have their papers accepted by the best journals. I moved toward the noise, wondering if they were debating the natural rate of unemployment or the productivity paradox.

Instead, I found that work had been suspended for the day so the group could watch the World Cup. With economists from all over the world importing their parochial passions, the atmosphere was intense and intoxicating. I watched with them to the final whistle.

With the 2014 World Cup kicking off this week, I was thinking back to that scene: economists taking a break from their discipline to enjoy the tournament. Ironically, economics has become a bigger and bigger influence on the event, with recent headlines illustrating the power of money in its staging. We may have to keep one eye on the pitch and the other on the profits.

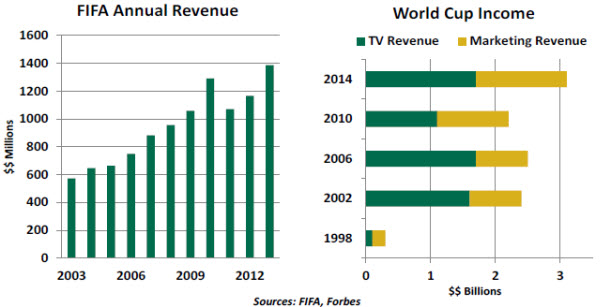

Like other major sporting events, the World Cup has become big business. This year’s tournament is expected to generate an astonishing $4 billion in revenue and $2 billion in profit for the Swiss-based Fédération Internationale de Football Association (FIFA), soccer’s global governing body. This will add a new peak to a progression that has already seen FIFA revenues double in the past 10 years.

Where sporting events once used to derive the lion’s share of their income from ticket sales, the reach of global television has made rights fees a primary revenue source. And since more people can see more matches on television, the opportunities available to sponsors have become much more valuable. This year’s competition in Brazil is expected to generate almost $1.5 billion in marketing fees, a record by a wide margin.

While FIFA is a clear winner in the World Cup’s financial arena, the calculus for the host country is considerably more complicated. Nations staging the event are responsible for improvements to infrastructure and stadiums. The 2014 event is going to cost Brazil an estimated $15 billion, triple the amount that South Africa paid to put on the 2010 edition.

Hosts get a short-term economic boost from the hordes that attend the competition. But these inflows are not nearly sufficient to completely defray costs. The main reason that countries are willing to invest such large sums in the World Cup and the Olympic Games (which Brazil will host in 2016) is branding. Putting on a successful show can inspire confidence and admiration that fosters both tourism and capital inflows. The illustrates the increment of image that this event generated.

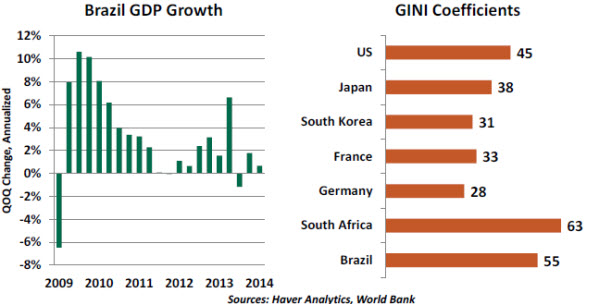

Of course, failing to stage a successful event can have the opposite effect. Brazil did not cover itself in glory in its preparation; cost overruns in construction left many public works projects unfinished (or in some cases, unstarted). Workers were lost while building stadiums, several of which remained incomplete just weeks before the opening kickoff. Allegations of bid-rigging to favor friends of the government abound. Many of the new facilities do not have permanent tenants after the tournament ends, threatening to turn them into “white elephants.”

Of course, failing to stage a successful event can have the opposite effect. Brazil did not cover itself in glory in its preparation; cost overruns in construction left many public works projects unfinished (or in some cases, unstarted). Workers were lost while building stadiums, several of which remained incomplete just weeks before the opening kickoff. Allegations of bid-rigging to favor friends of the government abound. Many of the new facilities do not have permanent tenants after the tournament ends, threatening to turn them into “white elephants.”

This has left the populace disappointed and disillusioned. The Brazilian economy has been faltering in spite of the massive investment related to the World Cup. And Brazil has a GINI coefficient, which measures the level of income inequality, that is much higher than any recent World Cup host save South Africa. There are those who think the money devoted to the tournament might better have been spent on health and education.

Violent protests surrounded last summer’s Confederations Cup, a dress rehearsal for the World Cup. A transit worker’s strike crippled Sao Paolo in the week before the opening match. These are not the kinds of things that inspire inbound investors or visitors.

The host country is not the only target of financial concern. Recent revelations have highlighted fixing of soccer matches through corrupt referees. And a recent alleged that FIFA delegates had accepted payments from Qatar to support that country’s bid for the 2022 competition. The perception that corrupt Swiss bureaucrats are profiting handsomely from the World Cup while Brazil may be left with huge debts from its conduct is an unfortunate juxtaposition.

These difficult matters will need to be addressed over time, but most of us would prefer that they be temporarily forgotten once the tournament gets into full swing. We watch games, in part, to transport us from the business focus that dominates our days. For the next month, let’s hope the emphasis is on the beautiful game, not the dirty money.

Japan’s Internal and External Challenges

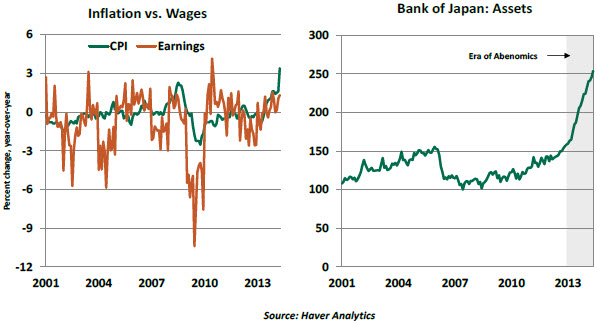

It has been just over a year since Japan’s leadership announced a sweeping program of economic reforms. These steps known as Abenomics, or the “three arrows,” were aimed at ending 15 years of economic stagnation. So far, the effort has shown some promise, but the harder steps may lie ahead.

Substantial monetary easing from the Bank of Japan (BoJ) has established inflation at a normal level. In recent comments, the BoJ’s Governor Haruhiko Kuroda expressed satisfaction with the progress of its quantitative and qualitative easing program, suggesting that effort was near its end.

In a break with his sponsor, though, Kuroda admonished Prime Minister Shinzo Abe for not doing more on the structural front. His fear is that the BoJ will reach its 2% inflation goal without a corresponding hike in the medium-term growth potential, which currently stands at 1% – 1.5%. Kuroda seems to genuinely believe that the country faces a seminal moment in which its economic course could be fundamentally altered if the proper steps were taken quickly.

In the short term, most signs suggest that Japan’s fragile economic recovery will survive April’s tax increase. The second quarter will definitely see the economy contract, but the strength of demand in the first quarter should keep the first half of 2014 in positive territory.

The governor has identified three steps necessary to increase the potential growth rate: an increase in private sector investment in human and physical capital; higher labor force participation; and the pursuit of deregulation and structural reforms. The BoJ is patting itself on the back for providing liquidity and breaking down the deflationary mindset, but it desperately desires reinforcements from Abe to carry the effort forward.

Prime Minister Abe continues to assert that structural reforms are an ongoing process and that he has already taken concrete steps. Those include limited agricultural reform; loosening restrictions on immigrant construction works; increasing daycare spaces; and proposing corporate governance measures. Abe has also lowered corporate income taxes by 2.4%, with a proposal for a 10% cut in fiscal year 2015 already on the table. Still, many of the programs that form the “third arrow” have very long timelines for implementation.  The challenge of restoring growth in Japan is complicated by the neighborhood in which it resides. Asia is filled with tough competitors and acrimonious history. Abe has simultaneously tried to balance a “charm offensive” toward most countries with a steely resolve toward others, namely China.

The challenge of restoring growth in Japan is complicated by the neighborhood in which it resides. Asia is filled with tough competitors and acrimonious history. Abe has simultaneously tried to balance a “charm offensive” toward most countries with a steely resolve toward others, namely China.

Abe has proposed reinterpreting the Japanese constitution to loosen restrictions on the use of the Japanese military. This can be seen as an attempt to counter China’s military rise and a way to deflect attention from lackluster growth at home. If passed, this step could also provide a way to stimulate growth through additional defense spending.

Relations with the rest of the region are less fraught as Abe presents Japan as a benevolent neighbor and alternative to China. The prime minister has offered patrol boats to the Philippines in response to tensions with China in the South China Sea and is considering doing the same for Vietnam. Japanese companies continue to aggressively expand operations in the Asian market. In 2013, new foreign direct investment to Association of Southeast Asian Nations countries rose to ¥2.3 trillion, nearly three times the 2012 level.

Japan’s improving relationship with Russia presents its own unique challenges. Japan is eager to establish a stronger relationship with its embattled neighbor, while also being careful to toe the official line on sanctions and coercive force. There must certainly be envy in Tokyo of the broad energy deal Russia and China signed last month; Japan could certainly use a cheap and stable source of fuel, given the reluctance to restart nuclear reactors.

As the focus shifts firmly from monetary policy to fiscal and social policy, Abe must balance a number of competing interests. The BoJ is echoing the broader consensus that the third arrow needs to take flight soon. However, political reality probably necessitates the current piecemeal approach to structural reform. The huge majority enjoyed by the ruling party has increased the danger that the Liberal Democratic Party reverts to its old habit of blocking reforms to the benefit of vested interests, especially agriculture and construction.

Abe has to restrain his party’s instinct to declare mission accomplished before the hard work even begins. And after a smooth initial partnership, the BoJ seems willing to call him out on this front. The need to keep internal and external relationships in careful balance will be key to the continued success of Japan’s reform program.

Capital: The Debate over Data

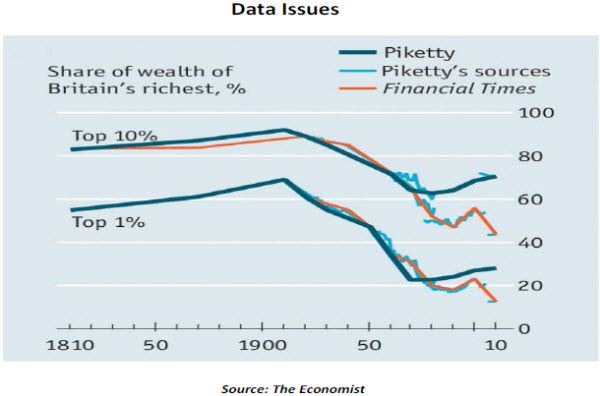

Thomas Piketty’s book, “Capital in the Twenty-First Century,” is once again in the limelight, but not for its controversial conclusions. Shortly after publication, The Financial Times raised questions about the veracity of data the book uses in its analysis. This started an exchange that reveals something fundamental about economic study.

The key idea in Piketty’s book is that a concentration of income and wealth occurs when the rate of return on wealth exceeds the growth rate of the economy. The rise in income inequality over the last 40 years is tied to this discrepancy, and he drives home his point with historical data.

Data sets of the nature that Piketty’s analysis employs present problems, because it is nearly impossible to find a uniform data set for “wealth” going back more than 100 years within a given country. And it would be more than a stretch to find data for an apples-to-apples comparison of wealth trends across many countries. To fill gaps and raise comparability, researchers use their judgment to adjust and interpolate data.

Piketty made all of his data available for inspection. He thought this would enhance the credibility of his conclusions, but it instead served as grounds for attack. Looking through the spreadsheets, The Financial Times saw some assumptions that it found objectionable.

After correcting for these, the FT found a more egalitarian distribution of wealth in Britain compared with Piketty’s time series. This undermines Piketty’s premise and his conclusions. This work invited a counter-editorial from Paul Krugman, who felt as if the FT was trying to hide a problem which Krugman sees as plain as day.

After correcting for these, the FT found a more egalitarian distribution of wealth in Britain compared with Piketty’s time series. This undermines Piketty’s premise and his conclusions. This work invited a counter-editorial from Paul Krugman, who felt as if the FT was trying to hide a problem which Krugman sees as plain as day.

Economic data is never clear and therefore offers room for selective analysis. Knowing the leanings of the author always helps place conclusions in the proper perspective. But the debate over data should not pre-empt discussions about the potential causes of, and remedies for, economic problems. Thomas Piketty attempted to focus on the latter but appears to have been dragged down by the former.

Recommended Content

Editors’ Picks

EUR/USD climbs to 10-day highs above 1.0700

EUR/USD gained traction and rose to its highest level in over a week above 1.0700 in the American session on Tuesday. The renewed US Dollar weakness following the disappointing PMI data helps the pair stretch higher.

GBP/USD extends recovery beyond 1.2400 on broad USD weakness

GBP/USD gathered bullish momentum and extended its daily rebound toward 1.2450 in the second half of the day. The US Dollar came under heavy selling pressure after weaker-than-forecast PMI data and fueled the pair's rally.

Gold rebounds to $2,320 as US yields turn south

Gold reversed its direction and rose to the $2,320 area, erasing a large portion of its daily losses in the process. The benchmark 10-year US Treasury bond yield stays in the red below 4.6% following the weak US PMI data and supports XAU/USD.

Here’s why Ondo price hit new ATH amid bearish market outlook Premium

Ondo price shows no signs of slowing down after setting up an all-time high (ATH) at $1.05 on March 31. This development is likely to be followed by a correction and ATH but not necessarily in that order.

Germany’s economic come back

Germany is the sick man of Europe no more. Thanks to its service sector, it now appears that it will exit recession, and the economic future could be bright. The PMI data for April surprised on the upside for Germany, led by the service sector.