The destruction wrought by the 2008 financial crisis necessitated a good deal of repair. In some areas, that repair is complete; in others, it is well along. But in one spot, it hasn’t really begun. Freddie Mac and Fannie Mae, the giant U.S. mortgage companies, remain in structural limbo more than five years after the American government rescued them.

Just as plans to restructure these government-sponsored entities (GSEs) finally began making their way through the U.S. Congress, cross currents arose that greatly complicate the way forward. Some former shareholders are suing to recover some value from the companies, while some legislators would like to leverage public ownership of Freddie and Fannie to boost the U.S. housing markets.

The visions of these two groups are misguided. Instead of being the subject of much- needed reform, it feels as if the GSEs are being pushed back in the direction that got them into trouble in the first place.

Freddie Mac and Fannie Mae are among the largest financial institutions in the world. They serve as a conduit through which U.S. home loans are accumulated and packaged for sale, and they guarantee principal payments to investors. The companies grew tremendously prior to 2008, as American housing boomed.

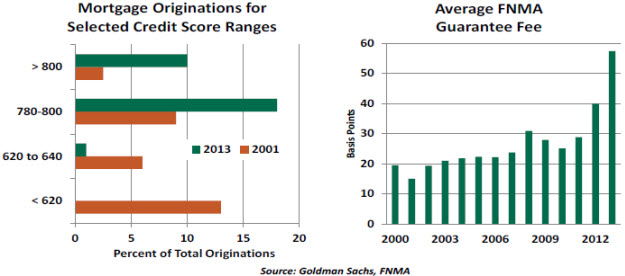

But their business models had two important complications. They were asked to promote broader home ownership, which led them to insure and own riskier loans. And they had private shareholders while enjoying a public backstop, which clouded their incentives.

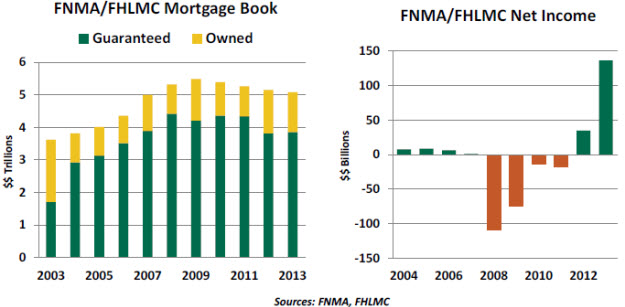

When housing values crashed and defaults crested, Freddie and Fannie found themselves in dire straits. Losses between 2008 and 2011 totaled more than $160 billion. Their regulator (now the Federal Housing Finance Authority, or FHFA) had allowed them to operate with very low levels of capital, which quickly disappeared. In August 2008, the U.S. government was forced to place them into conservatorship. And there they have remained.

The form of the support offered to Freddie and Fannie was carefully chosen. Had the Treasury taken them through a resolution, shareholders would have been wiped out and the assets of the two companies would have been consolidated onto the balance sheet of the U.S. Treasury. This would have created significant issues with the optics of the nation’s debt.  Under conservatorship, the government has warrants to buy 80% of the stock of the two companies. While this kept Freddie and Fannie at arm’s length from the federal ledger, it also kept shareholders in the picture. Some of these owners filed suits to reclaim some of the tremendous cash flow that the two GSEs spun off in the last two years.

Under conservatorship, the government has warrants to buy 80% of the stock of the two companies. While this kept Freddie and Fannie at arm’s length from the federal ledger, it also kept shareholders in the picture. Some of these owners filed suits to reclaim some of the tremendous cash flow that the two GSEs spun off in the last two years.

Whatever the legal form of the bailout, the companies were insolvent. The plaintiffs are essentially seeking to claim private profits after public assistance was provided. As unjust as this may sound, some think that the claimants have a reasonable chance of winning. And if they do, it would weaken the government’s standing to restructure the companies.

On the other side of things are those who would like to keep the GSEs as a piggy bank for the Congress and as an instrument to stimulate the housing sector. As we described in our recent note on housing, home sales and starts seem to have taken a turn for the worse. In response, some would like to roll back some of the post-crisis rules tightening lending criteria and have Freddie and Fannie lower the fees charged for backing mortgage credit.

As challenging as the housing correction has been for homeowners, investors and banks, it must be allowed to run its course so that the market can find a new, more- sustainable equilibrium. Stronger underwriting standards are designed to protect borrowers, not inhibit them. And the requirement that originators keep some skin in the game when selling loans is a very sensible reaction to the excesses of the last decade. This will mean lower levels of homeownership, but that is not necessarily a terrible thing.

In their current form, Freddie and Fannie present considerable risk to American taxpayers. A recent stress test of the two companies showed that they would suffer $190 billion in losses in a stressful environment, a blow that would require another bailout.  The GSE reform proposal calls for private investors to insure mortgage-backed securities, with the government acting as a final backstop. Freddie and Fannie would continue to serve as packagers, but their role as guarantors would end. This could create competition for the business, which could lower the price of the insurance. And the activity would be backed by proper levels of capital and covered by strong prudential oversight.

The GSE reform proposal calls for private investors to insure mortgage-backed securities, with the government acting as a final backstop. Freddie and Fannie would continue to serve as packagers, but their role as guarantors would end. This could create competition for the business, which could lower the price of the insurance. And the activity would be backed by proper levels of capital and covered by strong prudential oversight.

Unfortunately, there seems little chance that this design will progress very far. The legislature is unlikely to do anything significant before the midterm elections, and the courts may ultimately have the final say. This very messy situation may not have arisen had policy-makers not dragged their feet on GSE reform for so long. And now it may be too late.

India: Economic Measures for a New Era

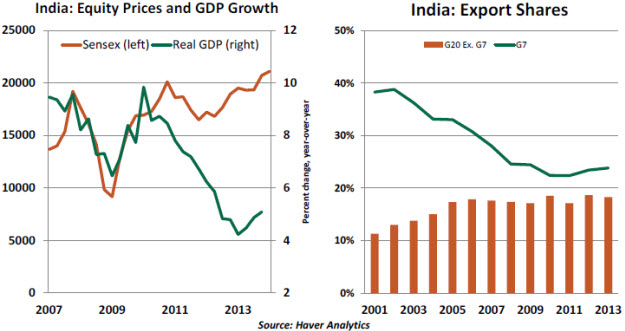

Expectations are riding high after Narendra Modi’s landslide victory in India’s elections. The new prime minister has vowed to shake India’s sluggish growth trend. For now, market reaction is strongly positive, with the Sensex recording significant gains and the rupee strengthening.

It is estimated that international financial institutions hold 22% of Indian equities; reportedly, U.S. investment accounts for a significant share of foreign holdings. Foreign direct investment in India has grown from an insignificant amount a decade ago to about $20 billion now, a jump of more than 400%.

Large capital outflows occurred after growth in India slowed to only 4.6% during 2012-2013. The recovery in equity prices suggests that markets place a high probability on real gross domestic product (GDP) growth catching up after Modi’s election.

These expectations for a return to much stronger growth can only be delivered if infrastructure demands, educational needs, an impaired banking system, corruption and lack of governance are adequately addressed. In the absence of these developments, money will find its way to a different destination to reap better rewards.

Inflation is the biggest impediment that will haunt the central bank and the newly elected government. Inflation has hovered between 8.5% and 10.3% for six straight years, with a decelerating trend visible only after the central bank lifted the policy rate last fall. The inflation-fighting credentials of the Reserve Bank of India were strengthened last fall; a continuation of this steadfast stance against inflation is critical for future growth.

Exports and foreign direct investment are both complements to other domestic initiatives that can spur growth. The Indian economic model is not export-driven. Total exports of goods make up only 25% of real GDP compared with China (40% of GDP). China’s export model is the not the most suitable, but the point is that India’s exports have the potential to lift growth.

The G7 (United States, United Kingdom, Canada, Japan, Canada, France and Japan) receive about one-fourth of India’s exports, while the members of the broader G20 are recipients of about 18% of India’s exports. This share has changed in the last decade, with the G7 importing fewer goods from India. India has explored ways to increase exports, but a lack of infrastructure is part of the reason for the limited success of Special Economic Zones (partly export promoting centers) in India.  Lifting caps on foreign direct investment and engaging in global business partnerships for infrastructure development is a sure bet to lift business momentum. The new prime minister’s goals for foreign direct investment should include less-stringent restrictions on that activity. China established Economic and Technological Zones to encourage foreign direct investment. Borrowing this from China’s playbook is a constructive step.

Lifting caps on foreign direct investment and engaging in global business partnerships for infrastructure development is a sure bet to lift business momentum. The new prime minister’s goals for foreign direct investment should include less-stringent restrictions on that activity. China established Economic and Technological Zones to encourage foreign direct investment. Borrowing this from China’s playbook is a constructive step.

Better development would also have significant benefits for the Indian population. About 75% of India has electricity and around 35% has access to treated tap water. The vast majority lack refrigerators, washing machines, bank accounts and basic transportation.

The political will to reduce corruption and promote good governance is imperative for India’s economic progress. India’s policy choices in the coming years will determine its place in the global economy. A strong political majority, the absence of a touchy coalition and the business focus of the newly elected leadership favor expectations of a revival.

Big Data: Will It Improve Quality of Inflation Estimates?

Measuring inflation is difficult, and the funding provided by governments for this purpose is inadequate. But there may be a better way.

Professors Alberto Cavallo and Roberto Rigobon of the Massachusetts Institute of Technology founded the Billion Prices Project (BPP) to compute alternative consumer price indexes on a real-time basis. The computer software they designed collects 3 million prices of goods sold online in more than 70 countries to compute real-time consumer price indexes.

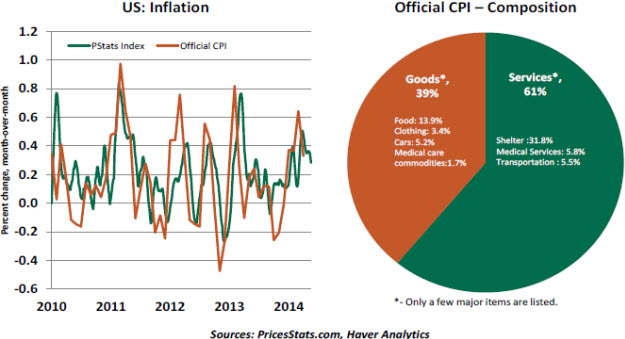

By contrast, the Bureau of Labor Statistics (BLS) gathers 89,000 prices in 87 cities in the United States spread over an entire month, using a mix of old and new ways to gather information. The BLS casts a wide net and captures the prices of all goods and services in its representative basket. Services make up nearly 61% of the Consumer Price Index (CPI) in the United States, and goods purchases account for the remaining 39%.

The US PriceStats Index (the official name for the BPP price index) uses proxies for offline purchases of services such as education and health care. So, coverage is different and includes a measure of educated estimation for a major part of the CPI.

Nonetheless, the change in the PriceStats Index tracks the change in the official U.S. CPI closely. This may not be the case in all countries; Professor Cavallo discovered that the official estimate of inflation in Argentina understated actual inflation – a good case to justify automated price collation.

Timeliness, cost-effectiveness, objectivity and shortening of policy lags are all advantages of big data for computing inflation estimates. However, purchases in most countries are done offline. Automated data collection prevents manipulation of inflation numbers, but the biggest drawback is limited coverage.

It is also fair to ask if we need a price index in real time to make the best business and policy decisions. The prices of the goods and services we purchase change in different time intervals. At one extreme, products sold on Amazon change by the minute, while the newsstand price for “The Wall Street Journal” has not changed for several months. So collecting prices more frequently may not necessarily produce better information.

Nonetheless, the BPP is an intriguing effort that capitalizes on “big data.” As time goes on and the process becomes better refined, techniques of this kind may be the wave of the future when it comes to producing economic readings.

Recommended Content

Editors’ Picks

EUR/USD clings to daily gains above 1.0650

EUR/USD gained traction and turned positive on the day above 1.0650. The improvement seen in risk mood following the earlier flight to safety weighs on the US Dollar ahead of the weekend and helps the pair push higher.

GBP/USD recovers toward 1.2450 after UK Retail Sales data

GBP/USD reversed its direction and advanced to the 1.2450 area after touching a fresh multi-month low below 1.2400 in the Asian session. The positive shift seen in risk mood on easing fears over a deepening Iran-Israel conflict supports the pair.

Gold holds steady at around $2,380 following earlier spike

Gold stabilized near $2,380 after spiking above $2,400 with the immediate reaction to reports of Israel striking Iran. Meanwhile, the pullback seen in the US Treasury bond yields helps XAU/USD hold its ground.

Bitcoin Weekly Forecast: BTC post-halving rally could be partially priced in Premium

Bitcoin price shows no signs of directional bias while it holds above $60,000. The fourth BTC halving is partially priced in, according to Deutsche Bank’s research.

Week ahead – US GDP and BoJ decision on top of next week’s agenda

US GDP, core PCE and PMIs the next tests for the Dollar. Investors await BoJ for guidance about next rate hike. EU and UK PMIs, as well as Australian CPIs also on tap.