- The debt ceiling drama is heating up

- Threatening default is reckless, but long-term budget issues require attention

- Measures of policy uncertainty show a link to economic performance

On the first Friday of each month, the U.S. employment report usually gives us plenty of food for thought. Sadly, the government shutdown has left us starved for economic information.

As of this writing, there is no resolution to report, although the pace of conversations seems to be increasing. Negotiations are now combining proposals to reopen federal agencies with measures to increase the government’s borrowing ceiling, which seems like a step in the right direction. The latter is the more critical issue, by far.

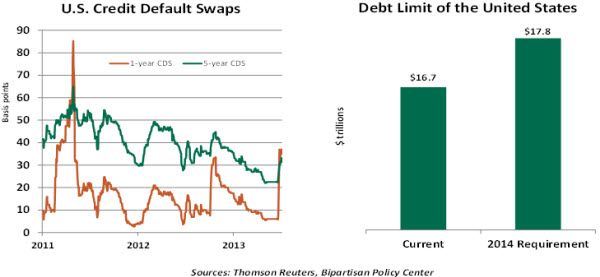

American legislators have been reminded by an international range of voices that failure to increase the debt limit would be a calamity whose impact on the financial system could be severe. While equity and bond markets have generally been pretty well behaved this week, the prices of credit default swaps against U.S. Treasury debt have jumped dramatically.

Some background on the central role of the debt ceiling in the current situation follows.

The No Budget, No Pay Act suspended the debt ceiling between February 4 and May 18, 2013. Treasury issues during this period were added to the previous debt limit, but there was no permanent increase in borrowing authority. The U.S. Treasury has been using “extraordinary measures” since then to avoid breaching the new ceiling. (These steps largely involve delaying reinvestment in several government funds.)

The uncertainty of key transactions and government cash flows makes it difficult to establish a precise date on which the Treasury will exhaust its extraordinary measures. In the weeks ahead, large transactions such as Social Security benefits, interest payments and Medicare payments will certainly test this capacity. The latest official projections anticipate a breach roughly two weeks from now.

Thereafter, the Treasury will have to prioritize payments to match the cash inflows from income and payroll taxes. Among the possible strategies to deal with expected revenue shortfalls is to delay interest payment on government bonds. The strong presumption would be that any arrears would be paid immediately upon the passage of a debt ceiling extension, but this would create what some have called a “technical default.”  The global financial system depends extensively on risk-free Treasury securities. Markets will have to make quick decisions if holdings of Treasury securities become non-performing assets. Some funds may no longer be able to hold them, and some investors may flee funds which do. There are innumerable financial transactions that use Treasury securities as collateral, all of which would have to be revalued (at best) or cancelled (at worst).

The global financial system depends extensively on risk-free Treasury securities. Markets will have to make quick decisions if holdings of Treasury securities become non-performing assets. Some funds may no longer be able to hold them, and some investors may flee funds which do. There are innumerable financial transactions that use Treasury securities as collateral, all of which would have to be revalued (at best) or cancelled (at worst).

The ripple effects of such an event are difficult to estimate. But policy-makers are not anxious to trigger a repeat of 2008, when the path taken by falling financial dominos was far longer and more circuitous than anyone could have imagined. In light of this, House Speaker John Boehner has reportedly vowed not to throw the country into default.

It is estimated that a debt ceiling of around $17.8 billion would accommodate government operations through the end of 2014. Congress may opt to reach this level in stages, but it must take the first step without delay.

The Long Run May Come Sooner Than We Think

We expect that the present fiscal brouhaha will prove to be a short-term annoyance. But lasting fiscal stability for the United States can only be achieved by correcting long-term imbalances.

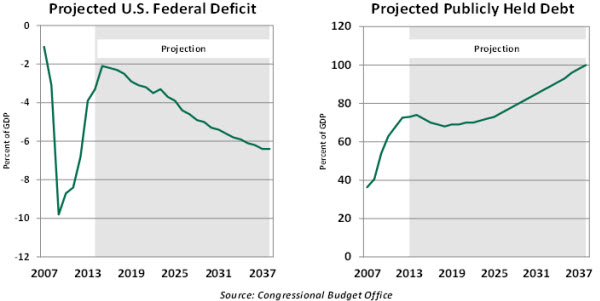

The American federal budget deficit shot up from 1.1% of gross domestic product (GDP) in 2007 to 9.8% in 2009. Better economic performance, some tax changes and spending discipline reduced the shortfall to 3.9% in 2013. It is projected by the nonpartisan Congressional Budget Office (CBO) to touch a low of 2.1% in 2015.

This recent reduction of the federal budget deficit is noteworthy, but the trajectory after 2015 is worrisome. The CBO projects the deficit to hit a high of more than 6.0% of GDP in the next 25 years. Publicly held debt as percent of GDP is forecast to reach 100% of GDP by 2038. These are troubling numbers, and current discussions barely touch on these challenges.

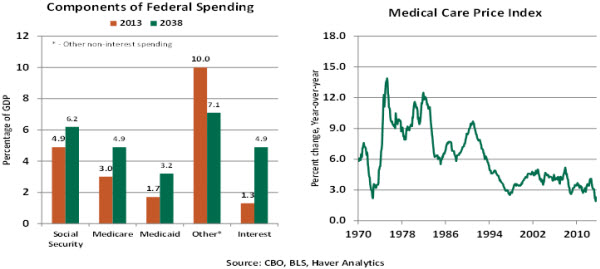

A brief overview of expected trends in federal government spending illustrates the urgency of the long-term fiscal problems of the nation. Among the five major components of federal spending – Social Security, Medicare, Medicaid, interest costs and non-interest spending (discretionary outlays) – discretionary spending is projected to make up a very small share of federal spending in the years ahead.  Of the remaining four elements, the CBO’s projections indicate that interest costs are predicted to grow from only 1.3% of GDP to almost 5.0% of GDP in the next 25 years. Higher deficits and the return of interest rates to more normal levels will be an influence here. These costs have a far reaching impact because Treasury yields influence borrowing costs of the private sector also.

Of the remaining four elements, the CBO’s projections indicate that interest costs are predicted to grow from only 1.3% of GDP to almost 5.0% of GDP in the next 25 years. Higher deficits and the return of interest rates to more normal levels will be an influence here. These costs have a far reaching impact because Treasury yields influence borrowing costs of the private sector also.

Social Security, Medicare and Medicaid have accounted for more than 50% of the federal government’s non-interest spending during the past 10 years. The aging population, rising health care spending per beneficiary and changes related to the Affordable Care Act (ACA) are the three major reasons for increases in the projected outlays of these programs.

The CBO projections indicate that under current law, 76 million people would collect Social Security benefits in 2023 and more than 101 million people would collect in 2038, compared with 57 million current beneficiaries. As the baby boom generation retires and longer life spans lead to longer retirements, Social Security will be stressed. Assets in the Social Security trust fund are ample but not enough to fully cover projected payments over time.

To bring the program into actuarial balance, either payroll taxes would have to increase, scheduled benefits would have to be reduced or program parameters (like the retirement age or the indexing of benefits) would have to be altered. Many households have very modest wealth and saving, so their reliance on Social Security benefits will make concessions difficult.

The aging of the population also causes the number of Medicare beneficiaries and elderly Medicaid beneficiaries to increase, which in turn leads to higher health care spending per person and larger total federal health care spending.

Total health care spending in the United States has grown rapidly in recent decades, excluding the period from 1993 to 2000 when managed care plans helped to trim the growth of health care spending. A weak economy is believed to have reduced the growth and cost of health care over the past few years, but it is unclear how long this will persist.

If the share of health care expenditures in GDP advances, by implication it will divert resources away from other sectors and may not result in an optimal economic composition. Therefore, it is essential to cap the pace of growth of health care spending.

Expanding federal deficits can be traced largely to the growth of Social Security and major health care programs. There are some interesting ideas out there for containing their associated costs, yet we’ve heard little from the Congress on this front during recent debate. Once remote, these burdens are becoming more proximate and must be addressed soon.

Fear of the Unknown

One of my favorite jokes involves a doctor, an engineer and an economist arguing about which is the oldest profession. The doctor stakes his claim by suggesting that the use of Adam’s rib to create Eve on the sixth day was an early surgical procedure. Not to be outdone, the engineer cites the formation of heaven and earth from chaos at the very outset of creation. The economist trumps the other two by asking, “well, who do you think created the chaos?”  As amusing as it is, the story is a bit unfair. Economists are not the creators of chaos, but rather the interpreters of chaos. Uncertainty is a constant in our lives, yet at times it escalates to a degree that challenges diagnosis. This week’s shutdown of the American government has not yet passed that tipping point, but reaching the debt ceiling would certainly defy logic for many.

As amusing as it is, the story is a bit unfair. Economists are not the creators of chaos, but rather the interpreters of chaos. Uncertainty is a constant in our lives, yet at times it escalates to a degree that challenges diagnosis. This week’s shutdown of the American government has not yet passed that tipping point, but reaching the debt ceiling would certainly defy logic for many.

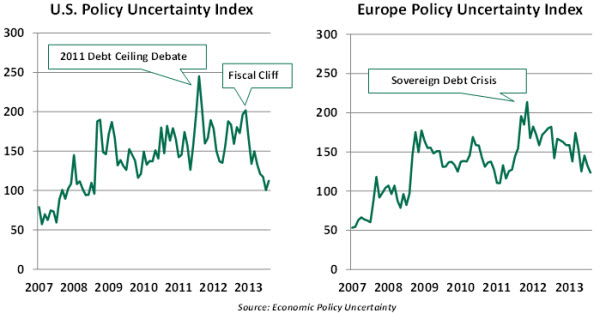

Researchers at Stanford University and the University of Chicago have assembled an index of policy uncertainty. It combines citations from media regarding policy debate, the volume of expiring tax rules that may not be sustained and the level of dispersion among economic forecasters. (So I guess we do contribute to the chaos, in some way.) The progression of these indicators for the United States and Europe is shown below.

The details behind the U.S. index show that taxes and health care have been the leading contributors to uncertainty over the last several years, potentially foreshadowing the present fiscal impasse. The lack of clarity over Federal Reserve policy has also been at play. The monthly series shown in the graph does not show the influence of the present government shutdown, but the daily reading reached 243 on October 1. If resolution does not arrive soon, we could see a new peak forming.

During last week’s trip to Europe, I noted the state of policy flux there. While the Continent has made impressive efforts to restructure and rehabilitate, structural reform still has some distance to travel. Discussions about forming a banking union to identify and resolve failed financial institutions are unfinished. Greece is likely to require another helping hand, and it is not clear what type of debt restructuring will be offered. Central banks still have challenges trying to restore more consistent economic growth.

During better times, some observers hailed the rise of the “United States of Europe.” Since the financial crisis, though, nations have been more inwardly focused and have become more sensitive to the flow of labor and capital across borders. Countries like Britain are asking tough questions about the European Union, which creates uncertainty over the future of shared governance.

Increasingly, research is finding that high levels of policy uncertainty can be damaging to economic performance. Worried consumers don’t spend; worried businesses don’t hire and expand; and worried investors are less inclined to take on risk. During the last debt ceiling debacle in 2011, confidence measures plunged and took some time to recover.

Economists have found a very tangible link between sustained upward movements in policy uncertainty and downward trends in industrial output and employment. The ramifications for financial markets can be seen in higher term premiums in fixed income markets and higher levels of market volatility. Policy-makers would, therefore, do well to calm the chaos instead of creating it.

Recommended Content

Editors’ Picks

AUD/USD remained bid above 0.6500

AUD/USD extended further its bullish performance, advancing for the fourth session in a row on Thursday, although a sustainable breakout of the key 200-day SMA at 0.6526 still remain elusive.

EUR/USD faces a minor resistance near at 1.0750

EUR/USD quickly left behind Wednesday’s small downtick and resumed its uptrend north of 1.0700 the figure, always on the back of the persistent sell-off in the US Dollar ahead of key PCE data on Friday.

Gold holds around $2,330 after dismal US data

Gold fell below $2,320 in the early American session as US yields shot higher after the data showed a significant increase in the US GDP price deflator in Q1. With safe-haven flows dominating the markets, however, XAU/USD reversed its direction and rose above $2,340.

Bitcoin price continues to get rejected from $65K resistance as SEC delays decision on spot BTC ETF options

Bitcoin (BTC) price has markets in disarray, provoking a broader market crash as it slumped to the $62,000 range on Thursday. Meanwhile, reverberations from spot BTC exchange-traded funds (ETFs) continue to influence the market.

US economy: slower growth with stronger inflation

The dollar strengthened, and stocks fell after statistical data from the US. The focus was on the preliminary estimate of GDP for the first quarter. Annualised quarterly growth came in at just 1.6%, down from the 2.5% and 3.4% previously forecast.