![]() Stephen Innes

Stephen Innes

SPI Asset Management

A combination of Financial Sector Risk in Europe, Geopolitical concerns, and Federal Reserve Board policy debate have injected a degree of apprehension into markets.

Moreover, while WTI continues to hold on to gains, not unexpectedly, the latest OPEC oil patch musings are taking an inferior position as traders kick the oil can down the road until there is more clarity on the OPEC deal, perhaps at the November meeting in Vienna.

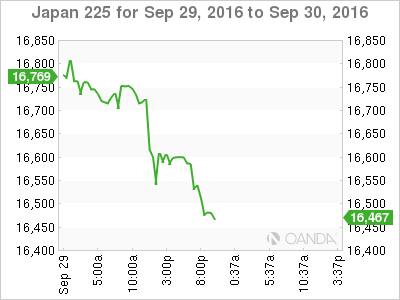

With escalating Macro concerns, the market is turning risk unfriendly. In particular, rumblings in the European-banking sector were reverberating throughout the NY session and we have seen the axiomatic risk off effect with USDJPY falling near 101, with USD Dollar buying versus risk-sensitive currencies like the Aussie dollar and other EM Asia Currencies.

While pre-US election risk jitters were expected, the mounting concerns over the stability of the European financial sector were not and this has raised more than a few eyebrows as risk managers scurry to reduce industry exposure.

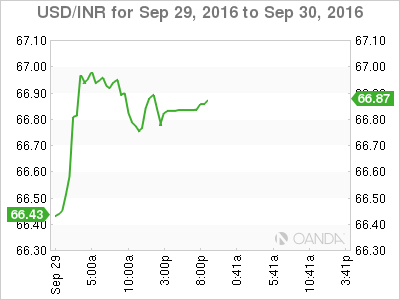

In APAC, regional geopolitical concerns also frothed after news broke that India carried out a surgical strike across the Line of Control. And while full-scale military escalation is unlikely, it’s always a risk and the market remains clearly focused on that possibility. USDINR has eased somewhat ahead of USDINR 67.00, as opportunists place nervous long Rupee bets.

Indeed, very mixed signals in currency markets as uncertainty rule the day.

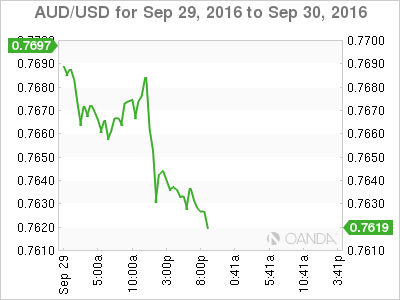

Australian Dollar

Very whippy markets exist after risk rallied in response to the OPEC deal, then hammered back to reality on a combination of risk reversal regarding European financials, Geo-Political concerns and a decent round of US economic data.

With long positions likely overextended in the wake of the OPEC risk euphoria, all eyes will be on the closing levels with the key .7600 level lining up as a significant near-term pivot point, so all eyes will be on today’s closing levels.

What appeared, after only 24 hours, to be a relatively straightforward bet post-OPEC decision, the long Aussie risk has ratcheted higher as another “too big to fail” scenario start to unfold in Europe.

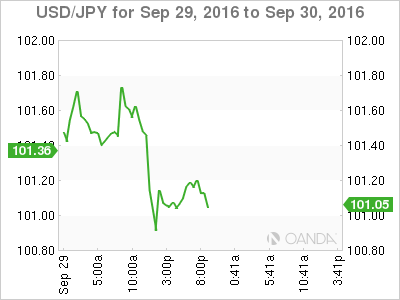

Japanese Yen

With risk aversion in play, the relatively buoyant US economic data offered temporary support to USDJPY. And, coupled with the risk-off dynamic as well as a high level of uncertainty creeping into the Yen landscape, I would expect upticks sold at least until the dust settles in the European Financial sector and Federal Reserve Board implements a rate hike. Then, the conundrum gets ironed out. The high level of uncertainty may see traders opt for the side-lines, ahead of unexpected weekend headline risk.

While it is not the time to hit the panic button, it is best to remember that where there’s smoke there’s usually fire.

The data from the CPI prints came in as expected; August’s Preliminary Industrial Production came in higher than anticipated.

Kuroda was on the wires this morning, but offered little new insight.

Yuan

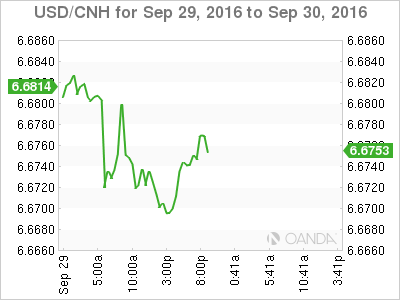

The iron fist takes is taking hold as the PBOC continues to quell Yuan speculation ahead of the SDR. As the mainland markets are closed from Oct 1 through 7, the PBOC took an unexpected tack of not easing onshore liquidity ahead of the holiday. In addition to the steady Yuan guidance theory, the other school of thought has the PBOC intentionally adjusting credit conditions as asset bubble risks become frothy again.

MYR

A lack of a convincing follow through on oil prices, coupled with whiffs of global risk aversion, has EM Asia back peddling to a degree. Until the landscape clears, expect to chop around in the current ranges as we head into the weekend

SPI Asset Management provides forex, commodities, and global indices analysis, in a timely and accurate fashion on major economic trends, technical analysis, and worldwide events that impact different asset classes and investors.

Our publications are for general information purposes only. It is not investment advice or a solicitation to buy or sell securities.

Opinions are the authors — not necessarily SPI Asset Management its officers or directors. Leveraged trading is high risk and not suitable for all. Losses can exceed investments.

Recommended Content

Editors’ Picks

EUR/USD clings to daily gains above 1.0650

EUR/USD gained traction and turned positive on the day above 1.0650. The improvement seen in risk mood following the earlier flight to safety weighs on the US Dollar ahead of the weekend and helps the pair push higher.

GBP/USD recovers toward 1.2450 after UK Retail Sales data

GBP/USD reversed its direction and advanced to the 1.2450 area after touching a fresh multi-month low below 1.2400 in the Asian session. The positive shift seen in risk mood on easing fears over a deepening Iran-Israel conflict supports the pair.

Gold holds steady at around $2,380 following earlier spike

Gold stabilized near $2,380 after spiking above $2,400 with the immediate reaction to reports of Israel striking Iran. Meanwhile, the pullback seen in the US Treasury bond yields helps XAU/USD hold its ground.

Bitcoin Weekly Forecast: BTC post-halving rally could be partially priced in Premium

Bitcoin price shows no signs of directional bias while it holds above $60,000. The fourth BTC halving is partially priced in, according to Deutsche Bank’s research.

Week ahead – US GDP and BoJ decision on top of next week’s agenda

US GDP, core PCE and PMIs the next tests for the Dollar. Investors await BoJ for guidance about next rate hike. EU and UK PMIs, as well as Australian CPIs also on tap.