My youngest daughter has an acute case of arachnophobia; even the tiniest spider sets her off. When a daddy longlegs appeared in the bathroom of a vacation home we were renting, she covered herself in the shower curtain and ran straight out the front door. It’s gotten so bad that the mere mention of a spider upsets her; the fear is almost worse than the reality.

As expected, the Federal Reserve closed its conclave this week without changing interest rates. The composed post-meeting statement betrayed little about when they might move. As “liftoff” draws near, though, phobias are emerging. Looking past promises that any tightening will be slow, some have conjured images of an aggressive program that will have deleterious effects on economic and market performance. Is there reason to fear?

Short-term interest rates in the United States have been near zero since December 2008. There are financial professionals who have entered the industry during the intervening years who have never known anything different. So any change, no matter how small, will represent an important departure from the recent status quo.

Market veterans could certainly be excused for having some apprehension. U.S. interest rates have generally been trending downward for a generation, so the prospect of the first sustained reversal is somewhat discomfiting.

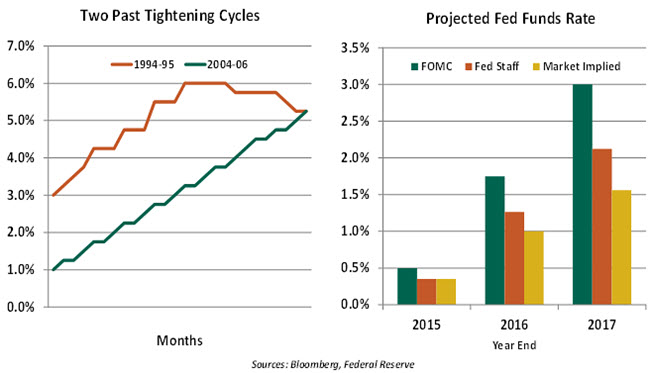

Two past Fed tightening phases have been cited as cause for concern. The first, in 1994, saw the markets caught by surprise as the funds rate doubled in a little over a year. The second, 10 years later, was better foreshadowed; overnight rates went from a low of 1% to a peak of 5.25%.

What both episodes demonstrate is that central banks rarely move in single steps. The opening usually begins a progression to a distant point. Most think that this time will be no different; the Federal Open Market Committee’s (FOMC) most-recent projection anticipates the funds rate will reach 3% by the end of 2017. (The outlook from the Fed’s staff, released prematurely, anticipates a less-aggressive strategy.)

An important increase in overnight interest rates, even if implemented over a period of years, could have adverse impacts on global fortunes. The U.S. economy may not handle the transition well. Even six consecutive years of growth and an unemployment rate approaching historic lows have failed to extinguish the sense that the American expansion remains fragile. The housing sector, which is quite sensitive to interest rates, would have an even more-difficult time shaking the doldrums if the Fed follows its forecast.

On a more-academic level, those who believe the secular stagnation theory feel that the interest rate that is consistent with full employment and targeted inflation is far lower than it used to be. The potential for a policy error is high; a number of other world central banks have tried tightening credit since 2008, only to retreat in the face of poor performance.

On a more-academic level, those who believe the secular stagnation theory feel that the interest rate that is consistent with full employment and targeted inflation is far lower than it used to be. The potential for a policy error is high; a number of other world central banks have tried tightening credit since 2008, only to retreat in the face of poor performance.

This latter angle may be among the leading reasons why “the market” does not seem to believe the Fed’s projections. The pricing of overnight index swaps, which reflects expectations for monetary policy, suggests only half the tightening shown in the June FOMC forecasts.

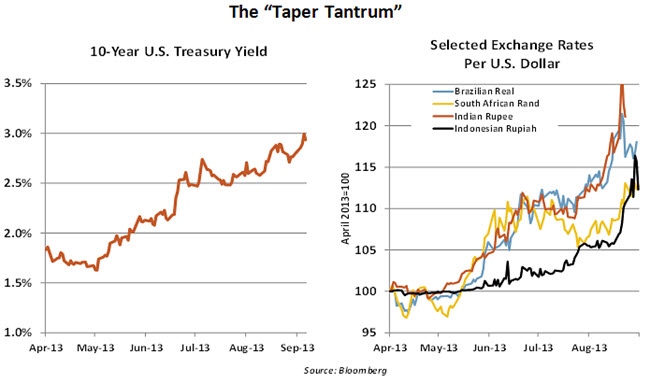

Higher interest rates in the United States could mean trouble for emerging markets. When Fed Chairman Ben Bernanke mentioned a potential tapering of asset purchases in the spring of 2013, it roiled markets.

Rising rates in the United States, especially if prompted by strong economic conditions, would almost certainly cause the U.S. dollar to strengthen. Developing countries that have borrowed in dollars but earn revenue in their local currencies will consequently find it more difficult to service and repay their debt. This prospect, along with the potential for associated market instability, was highlighted in the International Monetary Fund’s (IMF) recent report on the U.S. economy. IMF Managing Director Christine Lagarde has urged the Fed to hold off until wages and inflation begin rising more rapidly.

During the 2013 episode, Ben Bernanke may not have fully appreciated the weight of his words His successor, Janet Yellen, has certainly learned from that experience. Communication to this point about any change in policy has been carefully measured. During her appearance in front of Congress earlier this month, she consistently suggested that monetary policy would proceed with some caution. But the Fed’s decisions will be influenced by so many moving parts that it would be quite a feat to engineer an orderly return to normal rate levels. One or two hiccups might certainly occur along the way, and that is a legitimate cause for anxiety.

Fear is often not completely rational, but it must be respected. The Fed, however, must guard against giving it too much respect. Monetary policy works with long and variable lags, so starting soon provides insurance against imbalances that might arise in the future. There are those who think that markets have become addicted to zero interest rates and must be weaned off this dependence.

Fear is often not completely rational, but it must be respected. The Fed, however, must guard against giving it too much respect. Monetary policy works with long and variable lags, so starting soon provides insurance against imbalances that might arise in the future. There are those who think that markets have become addicted to zero interest rates and must be weaned off this dependence.

So the Fed will be facing a tangled web of data and opinion in the coming months as it approaches one of the most important decisions in its history. The markets are hoping that the bite of higher rates will be tolerable.

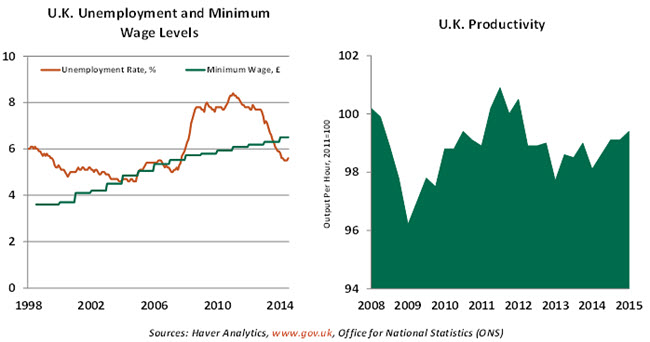

Britain Wages Debate

On July 8, Britain received its first fully Conservative budget since 1996. Free from coalition restrictions, George Osborne (the Chancellor of the Exchequer) announced spending cuts, new insurance taxes, a crackdown on tax avoidance and a reduction in working tax credits. The measures amount to a net tax increase of around £6 billion a year.

The balance between spending and austerity has global resonance, especially when times are tough. Spending more to stimulate the economy can generate jobs and increase tax revenues but also lead to higher debt levels, which can become unsustainable. Austerity can reduce debt and deficits, making a country more able to withstand global shocks. U.K. economic performance has been strong, though, so the fiscal drag embedded in the new budget should not be much of a hindrance.

The Chancellor has stated that he wants to transform Britain from a “low wage, high tax, high welfare” society toward one of “high wage, low tax, low welfare.” Making work pay has been a Conservative tagline for years and the Chancellor stuck to this, announcing a “living wage” for U.K. employees to offset lower tax credits. He is banking on a higher minimum wage to incent people into jobs, away from welfare dependency. But will it work?

Simply put, a minimum wage is a price floor, raising the cost of labor for the lowest-paid jobs in the economy. As prices rise, demand generally falls, thus the main fear of raising the minimum wage has always been that it creates unemployment as firms become unwilling to absorb higher costs. Indeed, Mr. Osborne admits his policy could result in 60,000 lost jobs.

On the flip side there are benefits, the most obvious being that improved pay can help alleviate poverty among low earners. Also, higher wages can incentivize people to work harder if they feel they are rewarded more for doing so, thus improving productivity (which is languishing in the United Kingdom). And the increased compensation could be the basis for stronger consumer spending.

A “living wage” (i.e., high enough to maintain a normal standard of living) is not a new idea. In fact, Britain already has one; it is just not mandatory. The Living Wage Foundation estimates the current rate would be £7.85 per hour in the United Kingdom or £9.15 in London. Companies paying it voluntarily report positive results. One study found that 80% of employers believe it improved the quality of output from their staff, and nonattendance fell by around 25% on adoption.

The Low Pay Commission, an independent organization which recommends the level of the existing minimum wage, funded a number of reports into the effect of the wage floor. The majority found little effect on overall employment, although some found a decrease in hours worked and increases in productivity. An estimate from Queen Mary University suggests 10,000 people escaped out of poverty as a direct result of the living wage.

The Low Pay Commission, an independent organization which recommends the level of the existing minimum wage, funded a number of reports into the effect of the wage floor. The majority found little effect on overall employment, although some found a decrease in hours worked and increases in productivity. An estimate from Queen Mary University suggests 10,000 people escaped out of poverty as a direct result of the living wage.

Other global research is varied. Evidence from Australia, although limited, indicates no effect on employment levels among youths. More expansive studies from the U.S. restaurant industry also find no employment effects. But an examination of data over an 18-year period in Canada found a decrease in youth employment of 2.5% in response to a 10% rise in the minimum wage. Worryingly, this impact took six years to reveal itself.

Britain is not alone in wanting to up the salary of its lowest-paid workers. Japan’s government is preparing for a “large-scale” increase in its hourly minimum wage in an attempt to increase the country’s poor productivity levels and get the economy moving. The minimum wage debate is also raging in the United States as it enters the early stages of the 2016 presidential campaign.

The Chancellor is currently riding a wave of popularity, meaning his spending plans are likely to be implemented in full. Thereafter, he’ll have to hope that higher minimums maximize economic performance.

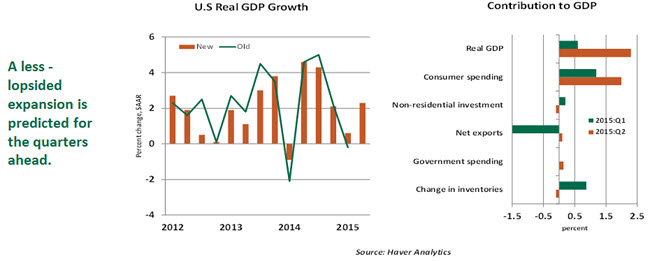

Slow but Steady

U.S. real gross domestic product (GDP) grew at an annual rate of 2.3% in the second quarter, a much-awaited improvement following a weak first quarter. Today’s report included revisions that replaced the 0.2% decline of the first quarter by a marginally better reading (+0.6%).

Consumer spending (+2.9%) was the major driver of economic growth in the second quarter, after a 1.8% gain during the first quarter. The weakness in business investment spending reflects declines in both information processing equipment and oil industry outlays. Surprisingly, inventories held nearly steady after a large accumulation in the first quarter. A correction is nearly certain in the second half of the year. Inflation remains subdued; the Fed’s favorite inflation measure showed a benign 0.2% gain, and the core price measure (which excludes food and energy) moved up 1.3% from a year ago.

Revised GDP data for 2012-2014 indicate annual average growth of 2.0% versus the originally reported advance of 2.3%, largely due to downward revisions of consumer outlays and government spending. The reduction in real GDP growth indicates that the recovery has been slower than previously estimated. By implication, productivity of the U.S. economy is also lower than earlier assessments.

Earlier this year, “residual seasonality” was cited as one of the reasons for a weak first quarter, and there were questions about regularity of slow first quarters in recent years. The Bureau of Economic Analysis (BEA) noted that it is has begun a three-phase project to address this problem.

The latest revisions reflect new seasonal factors and improvements in the seasonal methodology for defense spending, consumer service expenditures, net interest income and corporate profits. The second phase entails a detailed component-by-component review, which is a collaborative effort with agencies that provide data to the BEA. The final phase involves publication of non-seasonally adjusted data to enhance transparency.

The data will never be perfect. The data we have confirm that the expansion picked up pace in the second quarter and that potential economic growth in the United States is modest. This combination supports a “soon-and-slow” strategy from the Federal Reserve.

As expected, the Federal Reserve closed its conclave this week without changing interest rates. The composed post-meeting statement betrayed little about when they might move. As “liftoff” draws near, though, phobias are emerging. Looking past promises that any tightening will be slow, some have conjured images of an aggressive program that will have deleterious effects on economic and market performance. Is there reason to fear?

Short-term interest rates in the United States have been near zero since December 2008. There are financial professionals who have entered the industry during the intervening years who have never known anything different. So any change, no matter how small, will represent an important departure from the recent status quo.

Market veterans could certainly be excused for having some apprehension. U.S. interest rates have generally been trending downward for a generation, so the prospect of the first sustained reversal is somewhat discomfiting.

Two past Fed tightening phases have been cited as cause for concern. The first, in 1994, saw the markets caught by surprise as the funds rate doubled in a little over a year. The second, 10 years later, was better foreshadowed; overnight rates went from a low of 1% to a peak of 5.25%.

What both episodes demonstrate is that central banks rarely move in single steps. The opening usually begins a progression to a distant point. Most think that this time will be no different; the Federal Open Market Committee’s (FOMC) most-recent projection anticipates the funds rate will reach 3% by the end of 2017. (The outlook from the Fed’s staff, released prematurely, anticipates a less-aggressive strategy.)

An important increase in overnight interest rates, even if implemented over a period of years, could have adverse impacts on global fortunes. The U.S. economy may not handle the transition well. Even six consecutive years of growth and an unemployment rate approaching historic lows have failed to extinguish the sense that the American expansion remains fragile. The housing sector, which is quite sensitive to interest rates, would have an even more-difficult time shaking the doldrums if the Fed follows its forecast.

On a more-academic level, those who believe the secular stagnation theory feel that the interest rate that is consistent with full employment and targeted inflation is far lower than it used to be. The potential for a policy error is high; a number of other world central banks have tried tightening credit since 2008, only to retreat in the face of poor performance. This latter angle may be among the leading reasons why “the market” does not seem to believe the Fed’s projections. The pricing of overnight index swaps, which reflects expectations for monetary policy, suggests only half the tightening shown in the June FOMC forecasts.

Higher interest rates in the United States could mean trouble for emerging markets. When Fed Chairman Ben Bernanke mentioned a potential tapering of asset purchases in the spring of 2013, it roiled markets.

Rising rates in the United States, especially if prompted by strong economic conditions, would almost certainly cause the U.S. dollar to strengthen. Developing countries that have borrowed in dollars but earn revenue in their local currencies will consequently find it more difficult to service and repay their debt. This prospect, along with the potential for associated market instability, was highlighted in the International Monetary Fund’s (IMF) recent report on the U.S. economy. IMF Managing Director Christine Lagarde has urged the Fed to hold off until wages and inflation begin rising more rapidly.

During the 2013 episode, Ben Bernanke may not have fully appreciated the weight of his words His successor, Janet Yellen, has certainly learned from that experience. Communication to this point about any change in policy has been carefully measured. During her appearance in front of Congress earlier this month, she consistently suggested that monetary policy would proceed with some caution. But the Fed’s decisions will be influenced by so many moving parts that it would be quite a feat to engineer an orderly return to normal rate levels. One or two hiccups might certainly occur along the way, and that is a legitimate cause for anxiety.

Fear is often not completely rational, but it must be respected. The Fed, however, must guard against giving it too much respect. Monetary policy works with long and variable lags, so starting soon provides insurance against imbalances that might arise in the future. There are those who think that markets have become addicted to zero interest rates and must be weaned off this dependence. So the Fed will be facing a tangled web of data and opinion in the coming months as it approaches one of the most important decisions in its history. The markets are hoping that the bite of higher rates will be tolerable.

Britain Wages Debate

On July 8, Britain received its first fully Conservative budget since 1996. Free from coalition restrictions, George Osborne (the Chancellor of the Exchequer) announced spending cuts, new insurance taxes, a crackdown on tax avoidance and a reduction in working tax credits. The measures amount to a net tax increase of around £6 billion a year.

The balance between spending and austerity has global resonance, especially when times are tough. Spending more to stimulate the economy can generate jobs and increase tax revenues but also lead to higher debt levels, which can become unsustainable. Austerity can reduce debt and deficits, making a country more able to withstand global shocks. U.K. economic performance has been strong, though, so the fiscal drag embedded in the new budget should not be much of a hindrance.

The Chancellor has stated that he wants to transform Britain from a “low wage, high tax, high welfare” society toward one of “high wage, low tax, low welfare.” Making work pay has been a Conservative tagline for years and the Chancellor stuck to this, announcing a “living wage” for U.K. employees to offset lower tax credits. He is banking on a higher minimum wage to incent people into jobs, away from welfare dependency. But will it work?

Simply put, a minimum wage is a price floor, raising the cost of labor for the lowest-paid jobs in the economy. As prices rise, demand generally falls, thus the main fear of raising the minimum wage has always been that it creates unemployment as firms become unwilling to absorb higher costs. Indeed, Mr. Osborne admits his policy could result in 60,000 lost jobs.

On the flip side there are benefits, the most obvious being that improved pay can help alleviate poverty among low earners. Also, higher wages can incentivize people to work harder if they feel they are rewarded more for doing so, thus improving productivity (which is languishing in the United Kingdom). And the increased compensation could be the basis for stronger consumer spending.

A “living wage” (i.e., high enough to maintain a normal standard of living) is not a new idea. In fact, Britain already has one; it is just not mandatory. The Living Wage Foundation estimates the current rate would be £7.85 per hour in the United Kingdom or £9.15 in London. Companies paying it voluntarily report positive results. One study found that 80% of employers believe it improved the quality of output from their staff, and nonattendance fell by around 25% on adoption.

The Low Pay Commission, an independent organization which recommends the level of the existing minimum wage, funded a number of reports into the effect of the wage floor. The majority found little effect on overall employment, although some found a decrease in hours worked and increases in productivity. An estimate from Queen Mary University suggests 10,000 people escaped out of poverty as a direct result of the living wage. Other global research is varied. Evidence from Australia, although limited, indicates no effect on employment levels among youths. More expansive studies from the U.S. restaurant industry also find no employment effects. But an examination of data over an 18-year period in Canada found a decrease in youth employment of 2.5% in response to a 10% rise in the minimum wage. Worryingly, this impact took six years to reveal itself.

Britain is not alone in wanting to up the salary of its lowest-paid workers. Japan’s government is preparing for a “large-scale” increase in its hourly minimum wage in an attempt to increase the country’s poor productivity levels and get the economy moving. The minimum wage debate is also raging in the United States as it enters the early stages of the 2016 presidential campaign.

The Chancellor is currently riding a wave of popularity, meaning his spending plans are likely to be implemented in full. Thereafter, he’ll have to hope that higher minimums maximize economic performance.

Slow but Steady

U.S. real gross domestic product (GDP) grew at an annual rate of 2.3% in the second quarter, a much-awaited improvement following a weak first quarter. Today’s report included revisions that replaced the 0.2% decline of the first quarter by a marginally better reading (+0.6%).

Consumer spending (+2.9%) was the major driver of economic growth in the second quarter, after a 1.8% gain during the first quarter. The weakness in business investment spending reflects declines in both information processing equipment and oil industry outlays. Surprisingly, inventories held nearly steady after a large accumulation in the first quarter. A correction is nearly certain in the second half of the year. Inflation remains subdued; the Fed’s favorite inflation measure showed a benign 0.2% gain, and the core price measure (which excludes food and energy) moved up 1.3% from a year ago.

Revised GDP data for 2012-2014 indicate annual average growth of 2.0% versus the originally reported advance of 2.3%, largely due to downward revisions of consumer outlays and government spending. The reduction in real GDP growth indicates that the recovery has been slower than previously estimated. By implication, productivity of the U.S. economy is also lower than earlier assessments.

Earlier this year, “residual seasonality” was cited as one of the reasons for a weak first quarter, and there were questions about regularity of slow first quarters in recent years. The Bureau of Economic Analysis (BEA) noted that it is has begun a three-phase project to address this problem.

The latest revisions reflect new seasonal factors and improvements in the seasonal methodology for defense spending, consumer service expenditures, net interest income and corporate profits. The second phase entails a detailed component-by-component review, which is a collaborative effort with agencies that provide data to the BEA. The final phase involves publication of non-seasonally adjusted data to enhance transparency.

The data will never be perfect. The data we have confirm that the expansion picked up pace in the second quarter and that potential economic growth in the United States is modest. This combination supports a “soon-and-slow” strategy from the Federal Reserve.

Recommended Content

Editors’ Picks

EUR/USD clings to modest gains above 1.0650 ahead of US data

EUR/USD trades modestly higher on the day above 1.0650 in the early American session on Tuesday. The upbeat PMI reports from the Eurozone and Germany support the Euro as market focus shift to US PMI data.

GBP/USD extends rebound, tests 1.2400

GBP/USD preserves its recovery momentum and trades near 1.2400 in the second half of the day on Tuesday. The data from the UK showed that the private sector continued to grow at an accelerating pace in April, helping Pound Sterling gather strength against its rivals.

Gold flirts with $2,300 amid receding safe-haven demand

Gold (XAU/USD) remains under heavy selling pressure for the second straight day on Tuesday and languishes near its lowest level in over two weeks, around the $2,300 mark in the European session. Eyes on US PMI data.

Here’s why Ondo price hit new ATH amid bearish market outlook Premium

Ondo price shows no signs of slowing down after setting up an all-time high (ATH) at $1.05 on March 31. This development is likely to be followed by a correction and ATH but not necessarily in that order.

US S&P Global PMIs Preview: Economic expansion set to keep momentum in April

S&P Global Manufacturing PMI and Services PMI are both expected to come in at 52 in April’s flash estimate, highlighting an ongoing expansion in the private sector’s economic activity.