The business press has recently been heralding a “renaissance” for the eurozone. To us, that is a bit of hyperbole. The real Renaissance had a deep literal meaning, coming as it did after the era of the Black Death. And in ending the Dark Ages, the Renaissance ushered in a rebirth of human achievement that we are still marveling at some 600 years later.

It does appear that the eurozone is moving past its recent economic darkness to become a brighter part of the global economic outlook. But avoiding a recessionary/deflationary spiral is not the same as establishing a strong expansion. The eurozone may have new life but is still plagued by a series of pesky problems.

Writing in the most recent European Central Bank (ECB) Annual Report, President Mario Draghi expressed confidence that “…the weak and uneven recovery experienced in 2014 will turn into a more robust, sustainable upturn….” Some dismissed this forecast as more hope than conviction, but Draghi is proving to be somewhat prescient.

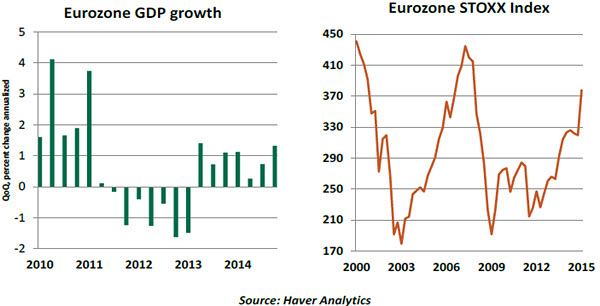

Headline real gross domestic product (GDP) for the eurozone expanded 0.3% in the fourth quarter of 2014, which translates into a comfortable 1.3% annualized growth rate. The eurozone economy has now expanded for seven consecutive quarters after contracting for seven. The plunge in global oil prices strengthened the nascent cyclical recovery and gave a boost to eurozone consumers and businesses alike. Meanwhile, the ECB’s easy monetary policy has caused the euro to slide, to the delight of exporters.

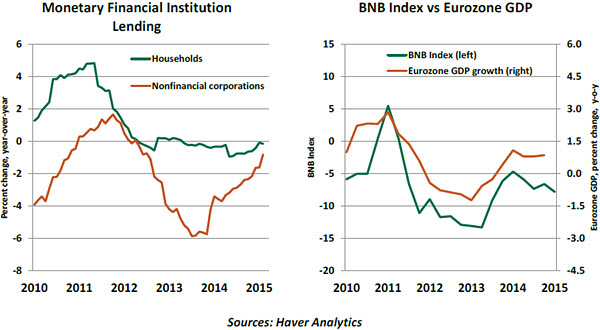

Equity markets have embraced the more upbeat outlook. Major indices across the continent have hit a series of record highs in the weeks since the ECB initiated its quantitative easing (QE) program. Skeptics would say that this is little more than investors fleeing negative interest rates in the fixed-income markets. But the favorable psychology associated with QE has abetted the recent improvement in the flow of credit. There are tentative signs that eurozone bank lending is expanding again after three years of contraction; given the region’s reliance on bank financing, this is an encouraging sign.

However, one of the leading indicators of eurozone growth is the Belgian National Bank’s (BNB) Business Confidence Survey. About 80% of Belgium’s manufacturing output is sold abroad, mostly to fellow European Union members. Thanks to strong trade ties with its neighbors, the BNB’s Business Confidence Survey is a reliable leading indicator for year-over-year GDP growth in the eurozone. After peaking in early 2014, the confidence index has been retreating since.

However, one of the leading indicators of eurozone growth is the Belgian National Bank’s (BNB) Business Confidence Survey. About 80% of Belgium’s manufacturing output is sold abroad, mostly to fellow European Union members. Thanks to strong trade ties with its neighbors, the BNB’s Business Confidence Survey is a reliable leading indicator for year-over-year GDP growth in the eurozone. After peaking in early 2014, the confidence index has been retreating since.

Modest estimates of global economic growth for 2015 might be one root cause of this trend. With overseas markets somewhat more sluggish than expected, the short-term boost to exports from a weaker euro is unlikely to gain much strength. In addition, other regions seem to be joining the devaluation game, creating more competition for eurozone producers.

Further, a significant constraint on eurozone growth is how unevenly it is spread across its leading members. In the fourth quarter, real GDP expanded at an annualized rate of 2.8% in Germany, the eurozone’s largest member. In France, however, it edged up just 0.5% and in Italy, real GDP has yet to turn positive (-0.1% annualized in the fourth quarter).

German exporters are well-placed to benefit from a weaker euro. Its labor markets were made more flexible by reforms implemented 10 years ago, and its consumers have responded to lower inflation. However, the French and Italian economies remain constrained. France may struggle to reach 1.0% growth and has not yet implemented necessary structural adjustments. And although Italy’s government is trying to implement long-term change, the economic payoff will not be felt for some time; this year, the economy will be lucky to record real GDP growth of 0.5%.

Germany accounts for about 29% of the total eurozone economy – hence an uptick in Germany is, indeed, good for the region as a whole. In Spain, growth will also be healthy this year as its exporters benefit from the painful internal devaluation of 2009-11. Add the two countries together and their combined 40% of the eurozone should ensure no return to recession.

But France and Italy together account for about 38% of the total eurozone GDP. With these two struggling to reach their longer-term growth potential, the recent recovery is unlikely to turn into a period of sustained, robust growth. Such constraints help explain why the level of eurozone GDP in the fourth quarter of 2014 was still 2% below the pre-crisis peak.

Finally, the prospect of “Grexit” – Greece leaving or being pushed out of the eurozone – is also looming. While not our base case, the situation creates event risk that could yet upset the recovery. One can hope that the markets have priced in much of that risk, which would limit any shock to the eurozone. But no one can anticipate the size of the splash or the ripples that might ensue.

For all its glory, the Renaissance was not without its rough patches. After all, the Protestant Reformation and the wars that followed took place during that interval. As today’s eurozone seeks renewed prosperity, there may still be some rough patches to face.

Realizing Potential

Markets follow GDP reports closely to track an economy’s progress. While GDP data are important on their own, the relationship of actual GDP growth to “potential” GDP growth is potentially more impactful.

Potential GDP growth is a theoretical estimate of the maximum increase in output a country can sustain without stoking inflationary pressures. If actual performance exceeds potential, then idle resources are being called back into production and inflation becomes more of a risk. If the opposite is true, slack is being created and disinflation becomes more likely.

Monetary policymakers use the difference between actual and potential GDP to determine if the economy needs more or less stimulus. For example, actual output in 2009 fell sharply in major advanced economies, and policymakers put in place policies to spur growth toward the potential.

Looking longer-term, lifting a nation’s standard of living is tied to increasing the economy’s potential capacity. In this context, the growth of potential GDP drives inbound investment and the attraction of a country’s equity markets.

Further, potential GDP growth plays a critical role in determining whether a country can comfortably manage its debt. Reduced prospects for potential growth make it much more difficult to sustain interest payments and reduce principal.

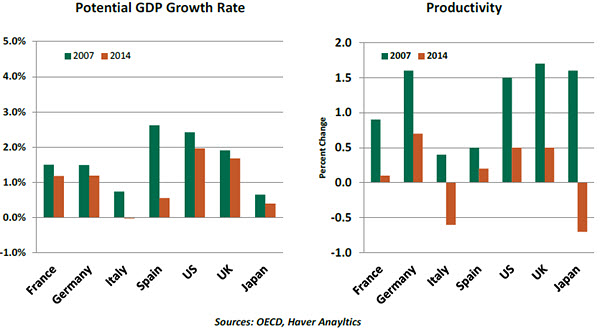

The growth rate of potential GDP is not fixed. It can change over time based on the levels of labor, capital and technology in an economy. Simply stated, an economy’s potential to expand in a non-inflationary way is the sum of its labor force growth and its productivity growth. In recent years, potential growth in advanced economies has slowed.

And as the charts below show, the changes are not uniform across these economies. The United States and the United Kingdom have fared better than Germany and Japan.

To be sure, cyclical factors can account for some of the recent drop in potential growth. Lingering balance sheet repair around the world has limited aggregate demand and slowed investment in productive infrastructure. But it will be critical to restore both to acceptable levels in the years ahead.

Policies to achieve this might take several forms. Demographics are difficult to change, but programs to sustain labor force participation would be helpful. Retraining programs for the structurally unemployed would be one way to spark expansion of the labor force in advanced economies.  Private investment in advanced economies declined sharply in the post-crisis period and is only now approaching the pre-crisis level in several major countries. Investment in Spain and Italy remains more than 30% below the pre-crisis level. Inducements to accelerate investment spending are clearly in order for some countries.

Private investment in advanced economies declined sharply in the post-crisis period and is only now approaching the pre-crisis level in several major countries. Investment in Spain and Italy remains more than 30% below the pre-crisis level. Inducements to accelerate investment spending are clearly in order for some countries.

Further, making the most of physical and human capital requires flexibility within an economy. The United States and United Kingdom have a structural advantage in this area: the World Bank’s measure of the ease of doing business places the United States and United Kingdom among the top 10 nations. Japan, France, Spain and Italy rank considerably below. Structural reform in these latter economies is, therefore, essential to enhancing potential growth.

Those nations that find the right formula to increase potential will be in the ascendance as this decade continues. And those that do not may find themselves facing a very challenging future.

Trans-Pacific Partnership – Make-or-Break Period

The next couple of weeks could prove to be a make-or-break interval for the Trans-Pacific Partnership (TPP) negotiations. The agreement is far-reaching in its scope because, in addition to traditional free-trade aims, it incorporates “behind-the-border” issues such environmental and labor standards; intellectual property rights; and government procurement and state-owned enterprises.

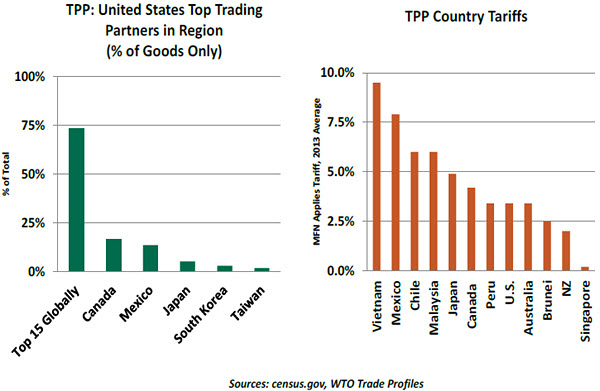

U.S. President Barack Obama is in the midst of a renewed push to secure the Trade Promotion Authority (TPA) necessary to close the deal. If the president fails to secure fast-track authority, there is a high likelihood that the multilateral trade agreement — comprising 12 countries representing 40% of world GDP — will be shelved until the next administration takes office.  In a rare turn of events, President Obama has aligned himself with congressional Republicans on this issue to overcome opposition from within the Democratic Party. Chief among Democratic critics are Senators Elizabeth Warren and Charles Schumer. Senator Warren argues that TPP would contribute to the decline of the middle class. Senator Schumer would like to add currency rules to trade negotiations. However, any attempt toward regulating the monetary policy of sovereigns is thorny and could prove fatal to the deal.

In a rare turn of events, President Obama has aligned himself with congressional Republicans on this issue to overcome opposition from within the Democratic Party. Chief among Democratic critics are Senators Elizabeth Warren and Charles Schumer. Senator Warren argues that TPP would contribute to the decline of the middle class. Senator Schumer would like to add currency rules to trade negotiations. However, any attempt toward regulating the monetary policy of sovereigns is thorny and could prove fatal to the deal.

In spite of ongoing negotiations among all proposed member countries, bilateral negotiations between Japan and the United States have been the major hold-up to any agreement. Tokyo wants tariffs lowered immediately on auto imports, whereas the United States wants to stretch out the process. For its part, Washington wants Japan to fully liberalize its agricultural sector. Once considered impossible, Japanese Prime Minister Shinzo Abe has gone some way toward taming Japan’s powerful agricultural cooperative and securing the support (acquiescence) of ruling backbenchers. The agreement is a centerpiece of the third arrow of Abenomics.

With TPA a real possibility, the Obama administration is likely aiming to announce an agreement to terms with Japan by April 29, when Abe becomes the first Japanese prime minister to address a joint session of Congress in nearly 50 years. The question now is can President Obama hold up his end of the bargain and deliver the U.S.-sponsored trade deal before Abe comes to Washington.

Recommended Content

Editors’ Picks

EUR/USD clings to modest gains above 1.0650 ahead of US data

EUR/USD trades modestly higher on the day above 1.0650 in the early American session on Tuesday. The upbeat PMI reports from the Eurozone and Germany support the Euro as market focus shift to US PMI data.

GBP/USD extends rebound, tests 1.2400

GBP/USD preserves its recovery momentum and trades near 1.2400 in the second half of the day on Tuesday. The data from the UK showed that the private sector continued to grow at an accelerating pace in April, helping Pound Sterling gather strength against its rivals.

Gold flirts with $2,300 amid receding safe-haven demand

Gold (XAU/USD) remains under heavy selling pressure for the second straight day on Tuesday and languishes near its lowest level in over two weeks, around the $2,300 mark in the European session. Eyes on US PMI data.

Here’s why Ondo price hit new ATH amid bearish market outlook Premium

Ondo price shows no signs of slowing down after setting up an all-time high (ATH) at $1.05 on March 31. This development is likely to be followed by a correction and ATH but not necessarily in that order.

US S&P Global PMIs Preview: Economic expansion set to keep momentum in April

S&P Global Manufacturing PMI and Services PMI are both expected to come in at 52 in April’s flash estimate, highlighting an ongoing expansion in the private sector’s economic activity.