One of my favorite jokes is the one about an economics graduate returning to campus for his 30th class reunion. Seeing his favorite professor in a classroom giving final exams, the man wanders in. After a warm greeting, the alumnus notices that the questions on the test are exactly the same as the ones posed three decades prior. “Ahh yes,” the professor replies, “but the answers have changed.”

I was thinking about that punch line during a lunch with clients last week. As it turned out, all five of us at the table had degrees in economics, albeit earned in different eras. I asked each how they had been taught to define full employment. The estimates ranged from 4% joblessness to 6% — wide enough to drive a truck through.

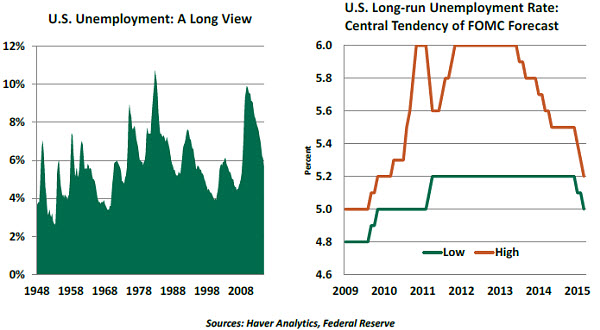

In the present day, the Federal Reserve has been struggling to define full employment. Its estimates cover a wide range, and change over time. What connotes peak labor market performance in today’s world, and what obstacles does the Fed face in steering us there? The responses to these questions are central to the outlook for interest rates.

Back in my day, research in this area centered on the “natural” rate of unemployment. It was thought that there were always a certain number of people in labor market transition (“frictional” unemployment) and a certain number who were not really employable for some reason (“structural” unemployment). The two components added to about 6%, according to my macroeconomics textbook, which was written by no less an authority than the current vice chairman of the Federal Reserve Board.

My elders at the lunch table pointed out that unemployment in their day had been persistently lower than 6%, which shaped the teaching of those times. Of course, this outcome was achieved with the help of military spending associated with the Korean and Vietnam conflicts, both of which had ended by the time I entered college.

By the 1990s, unemployment had fallen to levels not seen in a generation. Economists speculated that technology had made it easier for firms and employees to match, reducing the “frictional” component of the natural rate. A 4% rate not only seemed possible, but sustainable.

Further, leading thinkers gradually found less value in defining an absolute minimum for the unemployment level and focused instead on the point at which low joblessness would kindle higher inflation. This was called the “non-accelerating inflation rate of unemployment,” or NAIRU for short. I’ve never warmed to that term, which seems designed to confuse. But it does do a good job of expressing how hot the labor market can get before causing problems.

The Federal Reserve’s projection of the long-run unemployment rate, which many suggest is equivalent to the NAIRU, has been adjusting downward. It fell to around 5% in the forecasts they released this week. Those who set monetary policy base their decisions on how close we are to maximum employment; when that target moves, it can be very challenging.  Much has been said and written about the limitations of the traditional jobless rate as the basis for the NAIRU. It includes part-time workers who want to work full-time and excludes those who have temporarily given up looking for work. It is a purely domestic measure and thereby does not assess the capacity that exists overseas. Faced with constraints here, firms can shift work elsewhere to avoid triggering rapid wage gains.

Much has been said and written about the limitations of the traditional jobless rate as the basis for the NAIRU. It includes part-time workers who want to work full-time and excludes those who have temporarily given up looking for work. It is a purely domestic measure and thereby does not assess the capacity that exists overseas. Faced with constraints here, firms can shift work elsewhere to avoid triggering rapid wage gains.

It should also be noted that while maximum employment is one of the Fed’s mandates, achieving that objective is not entirely under the central bank’s control. Joblessness depends on many things, including education, trade and social policy, both here and overseas. These factors can create temporary or permanent skills mismatches.

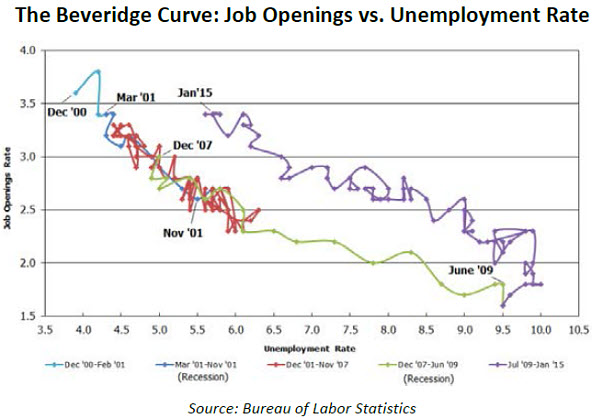

The Beveridge Curve: Job Openings vs. Unemployment Rate Source: Bureau of Labor Statistics

The Beveridge curve (shown above) attempts to illustrate the degree of structural unemployment. Some think that a high level of job openings relative to the unemployment rate means there are opportunities that workers are not in a position to take advantage of. The current expansion (shown in purple) has departed significantly from past experience, suggesting that something structural may be going on.  Monetary policy can certainly attempt to close this gap by maximizing economic performance. But it may be limited in addressing the more structural forms of unemployment, and trying too hard could kindle unpleasant side effects.

Monetary policy can certainly attempt to close this gap by maximizing economic performance. But it may be limited in addressing the more structural forms of unemployment, and trying too hard could kindle unpleasant side effects.

So while markets often prefer simple rules, defining full employment requires consulting a wide range of indicators and appreciating the shifting frictions and structures of the labor market. Those of us seeking answers in this area may periodically need to go back to school.

Spreading Negativity

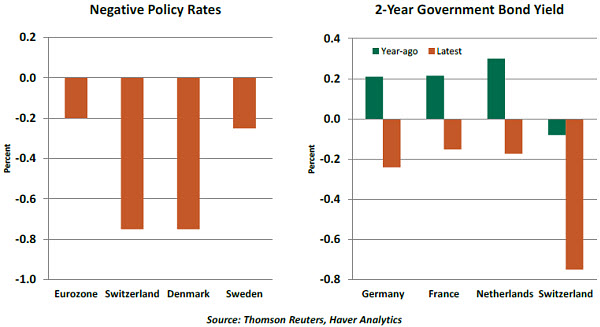

Following the Global Financial Crisis, central bankers lowered their policy rates close to zero. They also engaged in additional forms of monetary easing to raise the level of economic activity. In Europe, a lingering lack of demand and the threat of deflation pushed several central banks to adopt negative policy rates.

The European Central Bank (ECB) lowered its deposit rate to -0.10% in June 2014. A larger dip in inflation led to a second reduction of the deposit rate to -0.20% in September 2014. The Swiss National Bank reduced its policy rate to -0.25% in December 2014 and brought it down further to -0.75% in January 2015. The Danish and Swedish central banks have also joined the negative interest-rate club.

As the ECB embarks on its quantitative easing program, an expanding number of long-term interest rates have fallen below zero. Following these extraordinary measures of European central bankers, roughly 25% of all outstanding government bonds in Europe now trade at negative rates.

The German 2-year sovereign bond is trading at -0.24%. What does it mean when an investor buys a bond with a negative yield? The investor owes interest to the issuer, instead of the other way around. The mechanics in the payments system are reversed.

Why would an investor willingly purchase a security with a negative yield? For institutional investors in Europe, the yield comparison runs as follows. Parking money at the ECB at a deposit rate of minus 20 basis points entails a loss to bankers. Therefore, bonds yielding minus 8 basis points are more attractive.

In the private sector, investors’ fears about a deepening of the crisis and entrenched deflation allow them to view negative rates in a balanced light. Hypothetically, a bond with a negative rate of 8 basis points could represent a positive real return if deflation sets in, and it could be attractive if yields are expected to fall further.

But the consequences of negative interest rates cannot be overlooked. A prolonged period of negative interest rates has important implications across the broader economy.

- Negative yields send a signal that risk-aversion is so intense that investors are willing to pay to hold risk-free assets. This could color general perceptions of economic health.

- Individuals, firms, and financial institutions might hoard cash in physical form, where possible. Accumulation of cash implies it is not being spent, which translates into lower spending and economic growth. And it removes liquidity from the financial system, which could limit credit flows.

- There could be operational challenges with computer platforms that are not used to processing negative numbers in the interest-rate field.

- Commercial banks could pass on negative rates to customers as it costs them to place funds at the central bank. This could initiate important levels of dislocation if those clients seek better terms at other institutions or in other countries.

- Low and negative returns cause significant problems for insurance firms and pension funds. These institutions need to match their assets to future liabilities. If bond returns are low or negative and they face restrictions about the types of assets they can purchase, their assets will fall short of liabilities.

Some of these challenges are not new, as advanced economies have experienced very low interest rates for an extended period. But moving to a negative interest-rate environment exacerbates these difficulties. Moreover, a loss of principal is likely to elicit a quicker and larger response than situations of low return.

Dire distortions from negative interest rates have not materialized yet. Although markets have experienced negative interest rates for only a short time span, eurozone bank lending is moving in the right direction after a prolonged contraction. Equity prices have moved up, the latest inflation reading is less negative than a month ago, and the euro has depreciated significantly vis-à-vis the U.S. dollar. These are positive developments that suggest that negative interest rates may not be dangerous. And if sustained, improving economic conditions and expectations could ultimately lead to a normalization of interest rates.

Deflation and significantly low resource utilization drove the ECB to put in place a negative deposit rate and quantitative easing to stimulate economic activity. The jury is out on whether negative interest rates will help, hurt or just confuse.

A New Roof Over Our Heads

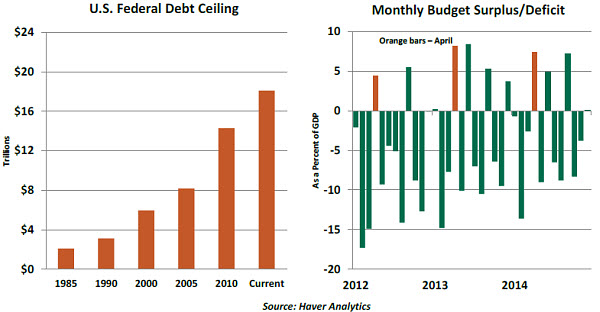

Quietly this week, the U.S. federal debt ceiling went back into force. It had been suspended since February 2014 as part of the Congressional budget agreement covering the last two fiscal years. The question on the horizon is where it might go from here.

To review, the United States is the only developed country that has a cap on the amount its government can borrow. It hasn’t been a particularly limiting feature; the ceiling has been raised nearly 100 times since it was first established nearly 100 years ago. We’ve argued in past commentary that it should be removed.

With the debt ceiling back in force, the government has no additional room to borrow. But this constraint will not become binding for a number of months. The Treasury has a roster of bookkeeping measures that will help manage cash flow for a time, and we are entering that part of the tax season where revenues exceed expenses by a significant margin. The Congressional Budget Office estimates that funding won’t run out until October or November.

The expiration of the debt ceiling serves as a checkpoint for fiscal policy. In recent years, this checkpoint has periodically become a “no-passing” zone, resulting in government shutdowns and market uncertainty. The country’s budget issues are important and deserve active debate. But here’s hoping that Congress won’t risk having the ceiling collapse on the economy.

Recommended Content

Editors’ Picks

AUD/USD tumbles toward 0.6350 as Middle East war fears mount

AUD/USD has come under intense selling pressure and slides toward 0.6350, as risk-aversion intensifies following the news that Israel retaliated with missile strikes on a site in Iran. Fears of the Israel-Iran strife translating into a wider regional conflict are weighing on the higher-yielding Aussie Dollar.

USD/JPY breaches 154.00 as sell-off intensifies on Israel-Iran escalation

USD/JPY is trading below 154.00 after falling hard on confirmation of reports of an Israeli missile strike on Iran, implying that an open conflict is underway and could only spread into a wider Middle East war. Safe-haven Japanese Yen jumped, helped by BoJ Governor Ueda's comments.

Gold price jumps above $2,400 as MidEast escalation sparks flight to safety

Gold price has caught a fresh bid wave, jumping beyond $2,400 after Israel's retaliatory strikes on Iran sparked a global flight to safety mode and rushed flows into the ultimate safe-haven Gold. Risk assets are taking a big hit, as risk-aversion creeps into Asian trading on Friday.

WTI surges to $85.00 amid Israel-Iran tensions

Western Texas Intermediate, the US crude oil benchmark, is trading around $85.00 on Friday. The black gold gains traction on the day amid the escalating tension between Israel and Iran after a US official confirmed that Israeli missiles had hit a site in Iran.

Dogwifhat price pumps 5% ahead of possible Coinbase effect

Dogwifhat price recorded an uptick on Thursday, going as far as to outperform its peers in the meme coins space. Second only to Bonk Inu, WIF token’s show of strength was not just influenced by Bitcoin price reclaiming above $63,000.