The housing sector has historically been an important driver of American economic recoveries. Construction is among the main industries to benefit from accommodative monetary policy and can initiate positive carryover to other sectors. When builders are busy, jobs are created for sectors of the labor force most often idled by recession.

We are now almost six years into the current American economic recovery, but residential activity still seems to be struggling. The rehabilitation of household balance sheets and housing finance remains incomplete, limiting progress. We’ve suggested in the past that that full recovery could take a decade, and that still seems to be a reasonable guess.

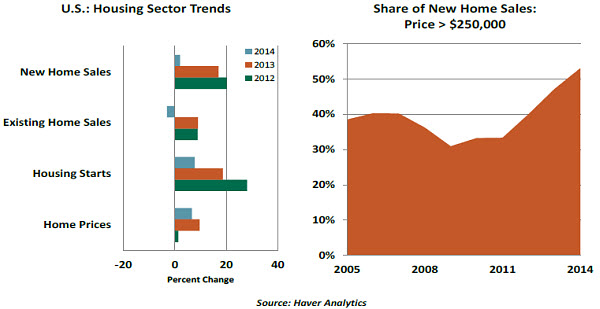

2014 was a disappointing year for U.S. housing. Combined sales of new and existing homes fell 2.7%, reflecting a nearly flat reading for new home purchases and a dip in sales of existing homes. The retreat came in spite of mortgage rates that were exceptionally low. Sales of high-end properties moved ahead most briskly, while those in the middle moved more slowly.  One reason for this outcome was the tapering of investor purchases of homes in foreclosure, which were eventually turned out for rental. These “distressed transactions” have fallen to only 11% of total sales from a peak of 49% in 2009. This has left realtors waiting for “organic buyers” to re-enter the market, but they have yet to do so.

One reason for this outcome was the tapering of investor purchases of homes in foreclosure, which were eventually turned out for rental. These “distressed transactions” have fallen to only 11% of total sales from a peak of 49% in 2009. This has left realtors waiting for “organic buyers” to re-enter the market, but they have yet to do so.

The direct impact of housing activity is reflected in the residential investment expenditure component of gross domestic product (GDP). The 2014 share of residential investment expenditure in GDP was 3.1%, well below the 6% peak in 2005 and the 5.2% average over the past 50 years. Construction of new homes increased in 2014, but largely in multi-family units. Rather than serving as an accelerant to economic activity, housing has been a headwind.

Some of the factors holding housing back are easing, while others will remain anchors. On the positive side, substantial gains in payroll employment over the past two years have restored income and creditworthiness to many American families. Real personal income grew 3.2% from a year ago in the fourth quarter, the best in the past two years. Strong stock market performance has provided an additional source of potential home equity for some prospective purchasers.

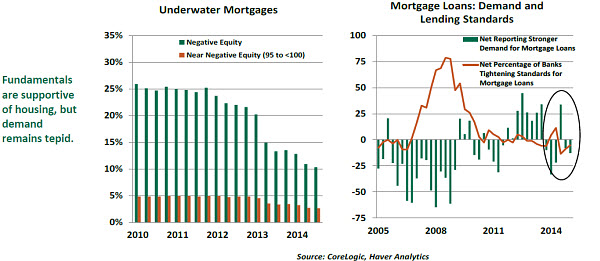

While it has been a slow process, the pressure from underwater mortgages (one where the outstanding mortgage loan value exceeds the market value of the home) is less worrisome. These loans now represent only about 10% of those outstanding, down from 25% in 2012. And the fraction of borrowers with only modest (less than 5%) equity in their homes has also declined. Rising home prices and careful deleveraging have both helped in this area.

In spite of these favorable trends, banks report very tepid demand for new mortgages. This could be a result of a reluctance to take on additional debt or the absence of a down payment sufficient to meet updated lending standards. Prospective buyers in the lower income quintiles may still be engaged in balance-sheet repair.

While credit terms for all other categories of loans have eased importantly over the past several years, mortgage standards have not. This sector of finance has been extensively re-regulated since 2008, and underwriters are still getting comfortable with new requirements and procedures. The ink is barely dry on a few of these new tenets.

Establishing the ability to repay and ensuring that borrowers understand their obligations are two points of emphasis in the new mortgage regime. Failing to comply can expose institutions to penalties, which may make them a little hesitant to commit. Hopefully, this impediment will ease somewhat over time.

Any improvement in demand would translate almost directly into new construction. Inventories of unsold existing and new homes are well below the historical medians.  To help things along, Fannie Mae and Freddie Mac have offered to purchase mortgage loans with only a 3% down payment as long as they satisfy the terms of a “qualifying mortgage.” In addition, the mortgage insurance premium for FHA loans was recently reduced by 50 basis points to 0.80%. There are also policy discussions underway to forgive some mortgage principal for some borrowers.

To help things along, Fannie Mae and Freddie Mac have offered to purchase mortgage loans with only a 3% down payment as long as they satisfy the terms of a “qualifying mortgage.” In addition, the mortgage insurance premium for FHA loans was recently reduced by 50 basis points to 0.80%. There are also policy discussions underway to forgive some mortgage principal for some borrowers.

Tempting though it might be to accelerate housing demand, these steps should be considered with extreme caution. It was aggressive credit practices that created the problems we’re still recovering from, and the U.S. economy has performed pretty well without its traditional contribution from the housing sector. In this case, patience may be the best policy.

Millennial Living

It is difficult to ascribe a personality to a whole generation, but there does seem to be a lot of focus and fuss around the “Millennials.” This cohort, commonly described as persons 18 - 33 years old, is larger (75.3 million) than the Baby Boomers (74.9 million). Their work habits and consumption habits have, therefore, been closely analyzed.

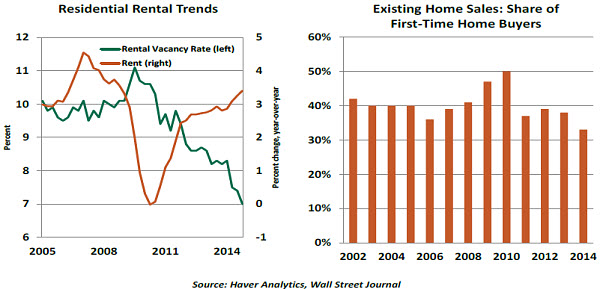

The dwelling habits of the Millennials have also been the subject of intense discussion, as they form the pool of prospective first-time homebuyers. They have not exactly been embracing this possibility; homeownership for those under the age of 35 is at a 10-year low, and more than 14% of 25- to 34-year-olds are currently living with their parents.

Most of those who ventured out are typically renting. Multifamily property has been among the most active in the real estate market, and rents have been rising at a pace of more than 3% annually. While renting has traditionally been a gateway to home purchases, that transition has been very, very slow in the current environment.

Some have posited that the Millennials have different attitudes toward ownership. Renting offers flexibility, and many young people may not see homes as the ideal investment vehicle. Whereas their parents grew up in an environment of ever-increasing house prices, their children have witnessed a terrible correction and its impact on their parents’ finances.  But surveys seem to contradict this narrative, with Millennials revealing a desire to eventually own homes. Their hesitance may be primarily due to modest finances; many are burdened by student debt, and some recent graduates have seen their careers get off to a slow start. Further, Millennials are marrying later (which limits the number of two-earner households) and having children later (which defers the need for extra space).

But surveys seem to contradict this narrative, with Millennials revealing a desire to eventually own homes. Their hesitance may be primarily due to modest finances; many are burdened by student debt, and some recent graduates have seen their careers get off to a slow start. Further, Millennials are marrying later (which limits the number of two-earner households) and having children later (which defers the need for extra space).

Ascertaining the psychology of a 25-year-old is not the easiest thing to do…trust me, I’ve tried. But when it comes to housing, the decisions made by the Millennials will be based less on mood and more on money.

Tight Quarters

When I returned from a recent business trip, I noticed that a second desk had been added to my office. My new suite-mate is a charming gentleman, but he sharpens his pencils obsessively with a pen knife every two hours and sings “The Hallelujah Chorus” every time the stock market hits a new record level. Intraday.

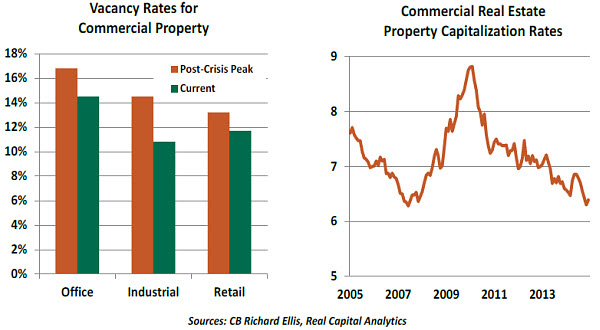

I asked management about the new seating arrangement and was told it was a consequence of the tight commercial real estate (CRE) market. While the residential side of the market gets the lion’s share of attention, the office, industrial and retail properties have been a growing focus for investors. Since this sector has been associated with past excesses, it has also become a growing focus for regulators.

The strengthening American economy has been very beneficial to the CRE sector. Offices are more completely occupied, an increasing volume of goods is moving through distribution centers, and consumers are spending more at the mall. Across the property spectrum, vacancy rates are well down over the past couple of years, and rents are rising.

Improving property cash flow is one factor helping CRE values. Another is scarcity of supply; last year’s addition to square footage was a little more than half of the pre-crisis peak, suggesting that builders have not yet gotten too far out of hand.

But another factor pushing valuations higher has been increasing interest from investors seeking yield in a low-interest-rate environment. Real estate investment trusts (REITs) have been increasingly popular elements of asset allocation, and those with significant means are acquiring parcels outright. Foreign investors have been particularly smitten by U.S. commercial real estate; an estimated $46 billion came into the market from overseas last year, up from $27 billion two years ago.  Returns to REITs were outstanding last year, and institutional investors have indicated that they will be increasing their devotion to the sector. As a result, capitalization rates (which are the ratios of annual profit to price for a property) have fallen to levels last seen since in 2007. Noting this, some observers wonder if the market is once again overheated and whether the credit used to finance CRE is at risk.

Returns to REITs were outstanding last year, and institutional investors have indicated that they will be increasing their devotion to the sector. As a result, capitalization rates (which are the ratios of annual profit to price for a property) have fallen to levels last seen since in 2007. Noting this, some observers wonder if the market is once again overheated and whether the credit used to finance CRE is at risk.

For the moment, this worry seems to be unfounded. Loans to finance commercial property have increased by 7% over the past year, only about half the pace of 10 years ago. Credit terms for CRE loans are getting marginally easier but have tightened a bit over the last two quarters. The prospect of more-substantial economic growth should enhance rental incomes. And capitalization rates are often judged on their relation to long-term interest rates, which remain very low.

In some key markets, though, conditions are a little more interesting. The market for multifamily property is particularly hot in selected cities, and capitalization rates of only 3% or 4% have been reported recently on some high-profile transactions. Further, there is a general concern about whether the sector can sustain its recent performance in a rising-interest-rate environment.

But to the degree that rising rates are prompted by strong economic activity, property cash flow should stay ahead of any increase in debt service. And the interest from investors is likely to remain strong as long as returns are strong. The outlook for CRE therefore remains quite positive.

There is a downside to this, though, in my increasingly cramped quarters. If this goes on much longer, I’ll be forced to start singing Willy Nelson’s classic line, “I can’t wait to get on the road again.”

Recommended Content

Editors’ Picks

EUR/USD clings to daily gains above 1.0650

EUR/USD gained traction and turned positive on the day above 1.0650. The improvement seen in risk mood following the earlier flight to safety weighs on the US Dollar ahead of the weekend and helps the pair push higher.

GBP/USD recovers toward 1.2450 after UK Retail Sales data

GBP/USD reversed its direction and advanced to the 1.2450 area after touching a fresh multi-month low below 1.2400 in the Asian session. The positive shift seen in risk mood on easing fears over a deepening Iran-Israel conflict supports the pair.

Gold holds steady at around $2,380 following earlier spike

Gold stabilized near $2,380 after spiking above $2,400 with the immediate reaction to reports of Israel striking Iran. Meanwhile, the pullback seen in the US Treasury bond yields helps XAU/USD hold its ground.

Bitcoin Weekly Forecast: BTC post-halving rally could be partially priced in Premium

Bitcoin price shows no signs of directional bias while it holds above $60,000. The fourth BTC halving is partially priced in, according to Deutsche Bank’s research.

Week ahead – US GDP and BoJ decision on top of next week’s agenda

US GDP, core PCE and PMIs the next tests for the Dollar. Investors await BoJ for guidance about next rate hike. EU and UK PMIs, as well as Australian CPIs also on tap.