Our warm wishes to those observing holidays this weekend.

I have a drawer full of foreign currency at home. Pounds, won, euros, yuan, reals, pesos and four different kinds of dollars are included in the collection. I suppose I should exchange some of it, but I’d pay a fortune in fees to do so.

Besides, the contents of that drawer may be the best-performing asset class in my portfolio. For the past year, the dollar has depreciated against major world currencies, making my holdings more valuable. While the position is small, the gains are nonetheless appreciated.

It may be time to reallocate. An expanding number of nations are pushing to devalue their currencies, in the name of competitiveness, price stability, or both. Few have been truly successful at this game, though, and some would be wise not to play.

Let me say at the outset that I am not the foremost currency strategist in the bank. I leave that to Joe Halwax in Chicago and Andrew Priest in London, who do a great job advising clients in this space. I tend to look at exchange rates based on long-term fundamentals, while they are much better aware of the technical influences that drive movements in the near term.

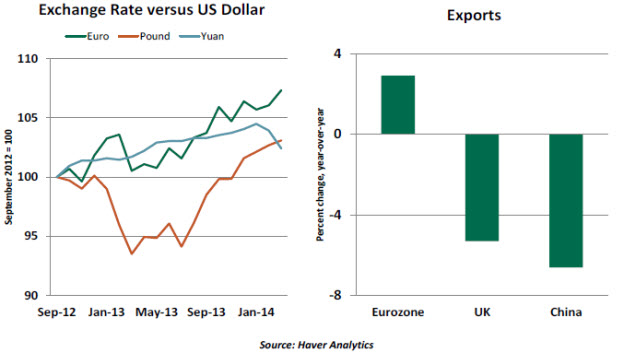

From my perspective, the American dollar has been surprisingly weak against some key counterparts. This has come despite economic growth and market performance that has been relatively strong in the United States.

Having a strong currency may be nice for travelers, but it annoys exporters. Local products become more expensive for foreigners when exchange rates are strong. Such conditions also place downward pressure on inflation by making imports less expensive. This complicates the task of central banks, which seek to keep the price level moving up at a targeted rate. Policy-makers in London, Frankfurt and Beijing (among other capitals) have expressed displeasure at the standing of their currencies and aimed to diminish them.

Recent attention has focused on China’s decision to broaden the trading band for the renminbi (RMB). The given reason was to allow the currency to trade over a broader range and thereby force those speculating in the RMB to endure greater volatility. But the RMB has inhabited the lowest end of that range over the past month, leading some to suspect that an intentional devaluation was underway.  Like their Asian neighbors, the Chinese have been somewhat perturbed by the mountain of quantitative ease introduced by the Bank of Japan. Ostensibly intended to end deflation, this action has also diminished the value of the yen and affected competitiveness in the region.

Like their Asian neighbors, the Chinese have been somewhat perturbed by the mountain of quantitative ease introduced by the Bank of Japan. Ostensibly intended to end deflation, this action has also diminished the value of the yen and affected competitiveness in the region.

Moving west, Mario Draghi, president of the European Central Bank (ECB), chimed in last week with a threat to take monetary steps to address what he sees as an overly strong euro. The ECB has struggled to put a floor under its inflation rate, and low imported inflation is one reason why. At the end of the chain, U.S. Treasury Secretary Jack Lew warned trading partners about their actions, offering a veiled threat of retaliation.

This sequence of events raises some important observations.

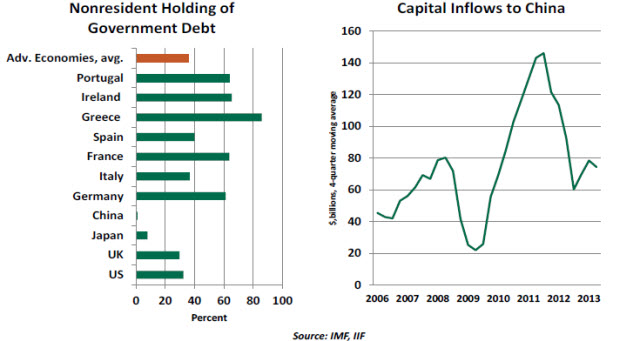

- Currencies are often driven more by capital flows than goods flows. As investors seek opportunities and safe havens, their movements can be very influential in determining currency rates. The recent attraction of European sovereign debt has been a major reason for the euro’s strength; it will be hard for the ECB to lean against that tide.

- Devaluing a currency reduces the returns earned by foreign investors in local markets. In places where foreign capital is a significant presence, actions taken to help exporters could jeopardize the flows of these funds. For countries with significant public debt that is owned by foreigners, this represents a risk to be respected.

- A weak currency can only go so far in promoting competitiveness. If the underlying products offered on world markets are struggling to win market share, currency devaluation may not win new adherents. For example, one reason that China is thought to be losing manufacturing market share is that Chinese labor costs are now rising much more rapidly than they are among its neighbors.

The simple truth is that everyone can’t have a weak currency. In trying to gain an advantage through devaluation, actors can invite retaliation that begins an expensive race to the bottom that no one really wins. Emerging markets with thin reserves can’t afford to play, and their currencies can end up in a downward spiral.

The simple truth is that everyone can’t have a weak currency. In trying to gain an advantage through devaluation, actors can invite retaliation that begins an expensive race to the bottom that no one really wins. Emerging markets with thin reserves can’t afford to play, and their currencies can end up in a downward spiral.

Quite a few of the world’s central banks have the management of currency value among their mandates. This is perhaps their most difficult task, given the myriad global influences that bear on the result. For that reason, it might be better for them to focus primarily on domestic outcomes like growth and inflation that are closer at hand.

In light of all of this, I may hang on to my international collection of bills and coins. After all, I am pretty long U.S. dollars, so some diversification can’t hurt. And I certainly hope that travel will give me the opportunity to return to those great places and boost consumption.

Acting Locally, Thinking Globally

The Federal Reserve and the Bank of England engaged in aggressive quantitative easing following the collapse of Lehman Brothers in 2008. While these efforts have helped local economies, they have created some hardship for emerging markets.

Raghuram Rajan, governor of Reserve Bank of India, recently presented his views on this topic at the Brookings Institution. Governor Rajan expounded on the different consequences advanced and that emerging markets have experienced over the past year; he suggested that optimum domestic economic policies do not assure international macroeconomic stability.

He noted that domestic political demands to lower unemployment could guide monetary policy to a path that is “sub-optimal” if legislatures aren’t able to address joblessness with other types of policy (like funds or incentives for retraining). The translation here is that a dysfunctional Congress in the United States led to the Fed shouldering most of the policy burden.

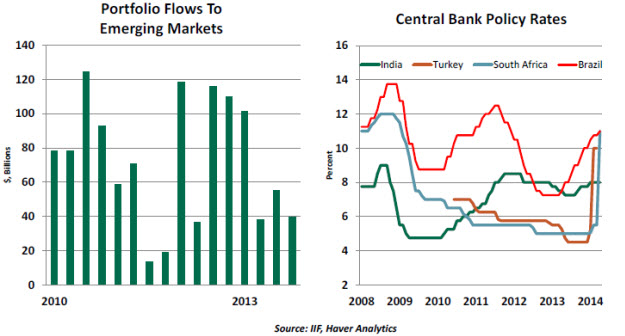

Low interest rates in developed markets have led capital into emerging markets. The recipient economies experience an appreciation of their exchange rates, which can hinder trade. In order to prevent a reduction of exports and economic growth, recipient countries will choose to accumulate foreign exchange reserves.

The positives of capital inflows – increased economic activity, rising asset prices, higher tax collections and improved fiscal status – can create an unsustainable environment because these benefits can dissipate just as quickly as they arise. Eventually, exit from unconventional accommodative monetary policy in advanced economies leads to capital outflows from emerging markets, a correction in asset prices and a depreciation of the exchange rate.

Higher interest rates are the traditional response to contain the depreciation of a currency due to capital outflows. This policy action disrupts growth in the recipient economies. In order to prevent this potentially vicious cycle, Rajan recommended that the Federal Reserve take into account the spillover effects of its actions and the expected feedback that will develop after other countries respond. Rajan even recommended that an independent assessor vet unconventional monetary policies.

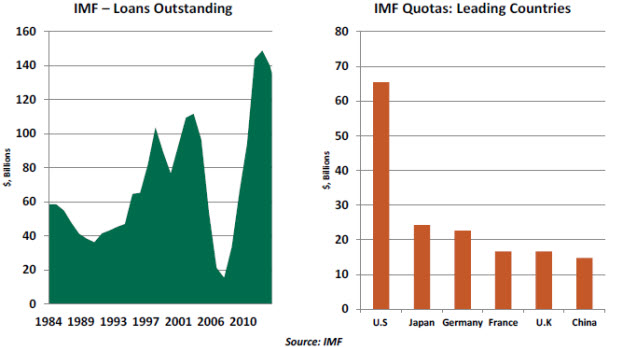

Rajan also suggested that the International Monetary Fund (IMF) could be a safety net in this regime, providing additional liquidity when emerging countries are suffering from the capital withdrawal caused by sudden reversal in quantitative easing.

Mr. Rajan is an exceptionally bright mind, and one who is not afraid to provoke controversy. At the Federal Reserve’s 2005 conference in Jackson Hole, Wyo., Rajan spoiled what was largely a retirement party for Alan Greenspan by suggesting that trouble lay ahead. He proved to be very right on that front.

Nonetheless, one can find flaws in his thinking about policy coordination. Central banks already have many variables and mandates to balance, and adding more would complicate an already intricate process. It can certainly be contended that a domestic focus can produce good results internationally: stronger growth in the United States, for example, would be very good for emerging markets.

As we have observed in the past, problems in the emerging markets are partly of their own making. And the vicissitudes of erratic capital flows can be contained with a wide range of controls and regulations that reduce the potential for instability.

Even if Rajan’s call for monetary policy coordination is heeded, weak economic fundamentals of some emerging markets leave them vulnerable to damage from large capital movements in a flexible exchange-rate regime. International monetary policy coordination is a lofty ideal, but implementation is fraught with practical impediments.

A Fund for Good

The IMF was founded in the wake of World War II, with the mission of heading off financial problems in troubled countries that had the potential to spark global contagion. Anywhere there is crisis – from Ukraine to Greece, the Middle East and Latin America – the IMF is sure to be involved.

Yet the recently concluded IMF spring meetings in Washington illustrated the challenges the organization faces in trying to promote its stated objectives. Since the financial crisis, countries have turned inward, using their policies and capital to address domestic concerns. High levels of joblessness in many places, for example, have diminished political and financial support for promoting economic activity elsewhere in the world.  There are also questions about the effectiveness of the IMF’s approach to troubled countries. Aid typically comes with tough prescriptions for fiscal and monetary policy; this austerity, while often necessary, can carry a tremendous economic cost. IMF Managing Director Christine Lagarde and ECB President Mario Draghi have recently sparred with one another on this front, with Lagarde criticizing the ECB’s inaction and Draghi offering that action might be less necessary had the IMF not dictated harsh terms to Europe’s periphery.

There are also questions about the effectiveness of the IMF’s approach to troubled countries. Aid typically comes with tough prescriptions for fiscal and monetary policy; this austerity, while often necessary, can carry a tremendous economic cost. IMF Managing Director Christine Lagarde and ECB President Mario Draghi have recently sparred with one another on this front, with Lagarde criticizing the ECB’s inaction and Draghi offering that action might be less necessary had the IMF not dictated harsh terms to Europe’s periphery.

The United States is the biggest stakeholder in the IMF, contributing about 18% of the organization’s capital. The United States also is the only country not to embrace a 2010 plan to double the IMF’s commitment and reapportion directorships to match the composition of world output. Some of the hesitance is the result of legislative dysfunction (a rider that favored U.S. political action funds was attached to a bill supporting the IMF plan), but part is also concern about China’s advancing role in the direction of the Fund.

In the past generation, world trade and global finance have grown exponentially. But the governance of this activity still rests largely with individual nations, whose failure to coordinate can introduce broad consequences. However imperfect, the IMF is among the very few institutions in good position to think and act globally. It therefore deserves our full support.

Recommended Content

Editors’ Picks

AUD/USD hovers around 0.6500 amid light trading, ahead of US GDP

AUD/USD is trading close to 0.6500 in Asian trading on Thursday, lacking a clear directional impetus amid an Anzac Day holiday in Australia. Meanwhile, traders stay cautious due ti risk-aversion and ahead of the key US Q1 GDP release.

USD/JPY finds its highest bids since 1990, near 155.50

USD/JPY keeps breaking into its highest chart territory since June of 1990 early Thursday, testing 155.50 for the first time in 34 years as the Japanese Yen remains vulnerable, despite looming Japanese intervention risks. Focus shifts to Thursday's US GDP report and the BoJ decision on Friday.

Gold price lacks firm intraday direction, holds steady above $2,300 ahead of US data

Gold price remains confined in a narrow band for the second straight day on Thursday. Reduced Fed rate cut bets and a positive risk tone cap the upside for the commodity. Traders now await key US macro data before positioning for the near-term trajectory.

Injective price weakness persists despite over 5.9 million INJ tokens burned

Injective price is trading with a bearish bias, stuck in the lower section of the market range. The bearish outlook abounds despite the network's deflationary efforts to pump the price. Coupled with broader market gloom, INJ token’s doomed days may not be over yet.

Meta Platforms Earnings: META sinks 10% on lower Q2 revenue guidance Premium

This must be "opposites" week. While Doppelganger Tesla rode horrible misses on Tuesday to a double-digit rally, Meta Platforms produced impressive beats above Wall Street consensus after the close on Wednesday, only to watch the share price collapse by nearly 10%.