“The one thing I know for sure about China is, I will never know China. It's too big, too old, too diverse, too deep. There's simply not enough time.”

– Anthony Bourdain, Parts Unknown

Much of the world is focused on what is happening in Greece and Europe. A lot of people are paying attention to the Middle East and geopolitics. These are significant concerns, for sure; but what has been happening in China the past few months has more far-reaching global investment implications than Europe or the Middle East do. Most people are aware of the amazing run-up in the Shanghai stock index and the recent “crash.” The government intervened and for a time has halted the rapid drop in the markets.

There have been a number of concerns about what this means for the Chinese economy. Is China getting ready to implode? Certainly there are those who have been predicting that outcome for some time. In this week’s letter I am going to try to explain both what caused the Chinese stock market to rise so precipitously and then fall just as fast and why we have to view China’s stock market differently from its economy.

As I have been saying for several years, in order for the Chinese economy to continue to grow, the Chinese must shift their emphasis from industrial production and infrastructure investment to a services-oriented economy. That is indeed what they are trying to do, and we are beginning to see signs of the services sector taking on a role as important to the Chinese economy as services are to the US economy. They have a long way to go, but they have begun the trip.

A Transformation Like No Other

When the US stock market crashed in October 1987, commentators on that era’s primitive financial media (I recall seeing them on the large wooden box in my living room) rushed to distinguish between the country’s economy and its stock market.

The American economy, they said, is just fine. Life will go on, and businesses will make money. As it turned out, that was good analysis – and it still is today – and not just for the United States. Stock markets do reflect the economy over time, but they can lead it or lag it for years.

Anyone who owns China stocks has probably sought solace in such thinking the last few weeks. The Chinese stock bubble is deflating in spectacular fashion. The sharp decline and Beijing’s flailing efforts to stabilize the market have many economists seeing deeper trouble.

We’ll compare and contrast the Chinese stock market and economy by looking at an unusual but very reliable data source. With apologies to Anthony Bourdain, whom I quoted at the beginning of the letter, we can know China. We just have to ask the right people the right questions.

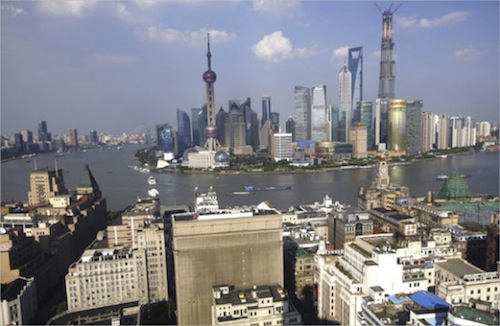

Back in 1987, as American investors were licking their wounds, the Shanghai skyline looked like this:

Here is a 2013 view from the same spot:

Photo credit: Carlos Barria, Reuters

A lot can change in 26 years. Transformations like this are commonplace in China. Gleaming cities now tower over what was undeveloped land a decade or two ago. Most of those cities even have people living in them, although the ghost cities are legendary.

You can crunch any numbers you like in any way you like, and it will be clear that China’s rapid growth is unprecedented. It is changing the course of human history. China has moved more than 250 million people from living a medieval lifestyle in the country to living and working in these fabulous new cities. And they have built the infrastructure to connect and supply them.

Worth Wray and I explored China from many different perspectives in our e-book, A Great Leap Forward? Our all-star cast of China experts variously see both opportunity and risk. The book is getting rave reviews. If you’re interested in an in-depth analysis of China, it’s the place to start.

In thinking about China last week, I skimmed through the book and noticed something that, with the benefit of hindsight, is simply stunning. The paragraphs I read brought all the pieces together to explain the Chinese stock market’s epic drawdown.

China GDP Versus China Beige Book

The part that made me sit up straight was in the contribution by Leland Miller of China Beige Book. His chapter “How Private Data Can Demystify the Chinese Economy” comes at the Chinese economy from a unique angle.

We all know government economic data isn’t always reliable. That is especially true in China. It is the only country in the world that can report its GDP quarter after quarter and never have to revise its calculations. That is just the most obvious of its economic data manipulations.

Even knowing that, most China analysts still rely on that GDP number, because it is all they have. That is beginning to change because of the work of Leland Miller. Leland, along with his colleague Craig Charney, decided to build an alternative analysis to government GDP numbers. Using the same methodology that the Federal Reserve uses in its quarterly Beige Book, they gather data from a network of observers all over China. Their clients – who include the world’s largest central banks – provide granular data that gives a much deeper view of the Chinese economy.

In A Great Leap Forward? Leland describes how China Beige Book picked up on a major change in Chinese businesses. He says the country’s 2014 slowdown was different.

The slowdown of 2013 was the result of subtle credit tightening, few signs of which were evident in official data right up until the June interbank credit crunch caused a market panic. Small and medium-sized companies during that period still wanted to access credit but found – TSF data notwithstanding – that it was difficult if not impossible to do so. 2014, intriguingly, has proven to be a very different story.

One of the most interesting dynamics we’ve tracked across corporate China has been the historical disconnect between company performance and the willingness of those companies to continue to borrow and spend. In many sectors, particularly troubled ones such as mining and property, firms typically reacted to poor results in a peculiarly Chinese way: they doubled down.

Too often, the thinking appeared to be: good results were good, but bad results were not necessarily bad, because the government was expected to step in and bail them out. Perhaps with subsidies, perhaps by ordering loans to be rolled over to another day. Firms often chose to act in demonstrably non-commercial ways.

Since early 2014, however, our data suggest a startling transformation. During the second quarter, CBB data showed a particularly broad deceleration in revenue growth nationwide: for the first time in our survey, not one sector showed on-quarter improvement. Yet firms reacted to this slowdown in a surprisingly rational way: capital expenditure growth fell broadly, as did capex expectations, as did loan demand – all to the lowest levels in the history of our survey. The third quarter then showed yet another quarter of weak loan demand, with even lower levels of current and expected capex.

Firms watching the economic slowdown didn’t want to spend – and they didn’t want to borrow either. For the time being, they preferred to watch events unfold from the sidelines.

Leland says, and I agree, that this was a positive development. Both businesses and investors need the discipline of free markets. Experiencing failure forces everyone to learn what works and what doesn’t work.

In a phone call this week, Leland told me their data actually pinpointed this change in the second quarter of 2014. He thinks it was the most important single quarter in Chinese economic history. I’m sure that Leland, as an Oxford-educated China historian, doesn’t say that lightly. It was in that quarter, Leland thinks, that Chinese business leaders “stopped acting Chinese.” Faced with falling demand, they did the rational thing and stopped adding new capacity. As he says in the excerpt above, they didn’t want to spend or borrow. They just sat on the sidelines. That was a good business decision. Unfortunately, it wasn’t consistent with Beijing’s master plan.

Recommended Content

Editors’ Picks

GBP/USD stays weak near 1.2400 after UK Retail Sales data

GBP/USD stays vulnerable near 1.2400 early Friday, sitting at five-month troughs. The UK Retail Sales data came in mixed and added to the weakness in the pair. Risk-aversion on the Middle East escalation keeps the pair on the back foot.

EUR/USD extends its downside below 1.0650 on hawkish Fed remarks

The EUR/USD extends its downside around 1.0640 after retreating from weekly peaks of 1.0690 on Friday. The hawkish comments from Federal Reserve officials provide some support to the US Dollar.

Gold: Middle East war fears spark fresh XAU/USD rally, will it sustain?

Gold price is trading close to $2,400 early Friday, reversing from a fresh five-day high reached at $2,418 earlier in the Asian session. Despite the pullback, Gold price remains on track to book the fifth weekly gain in a row.

Bitcoin Price Outlook: All eyes on BTC as CNN calls halving the ‘World Cup for Bitcoin’

Bitcoin price remains the focus of traders and investors ahead of the halving, which is an important event expected to kick off the next bull market. Amid conflicting forecasts from analysts, an international media site has lauded the halving and what it means for the industry.

Israel vs. Iran: Fear of escalation grips risk markets

Recent reports of an Israeli aerial bombardment targeting a key nuclear facility in central Isfahan have sparked a significant shift out of risk assets and into safe-haven investments.