![]() KBC Market Research Desk

KBC Market Research Desk

KBC Bank

On Thursday, the dollar rebound took a breather as the equity rally slowed and US inflation disappointed. This capped further USD gains, but the greenback quite easily maintained this week’s gains. That’s remarkable given the post-Fed weakness of late. EUR/USD closed the session at 1.1268, almost unchanged from Wednesday. USD/JPY finished the session at 109.40 (from 109.34 ).

Overnight, Chinese Q1 GDP was exactly in line with expectations at 6.7% Y/Y.

March industrial production was substantially stronger at 6.8% Y/Y. The market reaction to the data is muted. Most regional equity indices show modest losses, which is probably some short-term profit taking on recent gains. The Aussie dollar temporary gained a few ticks , but AUD/USD fails to break to new highs as the commodity rally slows. EUR/USD holds yesterday’s tight range and trades around 1.1260. USD/JPY remains well supported, trading in the 109.60 area.

Today, the eco calendar contains the US Empire State manufacturing index, US industrial production and the first estimate of April University of Michigan consumer confidence. Citigroup announces Q1 earnings, Fed’s Evans is scheduled to speak and the IMF/World Bank/G20 meetings take place in Washington. Consensus expects a limited further increase for the Empire State manufacturing index. We see risk for a stronger report. Industrial production is expected to have declined further in March, by 0.1% M/M, but manufacturing output, is forecast to show a limited increase. For both we see downside risks.

Finally, University of Michigan consumer confidence is forecast to have improved from 91 to 92 following three consecutive monthly declines. A continued improvement in labour market conditions and reports of higher wages should support sentiment. We see risks for a higher Michigan reading too. Yesterday, the dollar (and the US interest rate markets) ignored a lower than expected CPI report. Is this an indication that enough Fed softness is discounted and that the dollar is now more sensitive to positive US data surprises rather than negative ones? The jury is still out. In a day-to-day perspective, we assume that the downside of the dollar is rather well protected unless really bad news kicks in. EUR/USD and USD/JPY remain confined to tight ranges though. Even after the recent USD rebound, no key technical levels are broken. Oil and the comments from the G20 meeting are a wildcard. We maintain a cautiously positive dollar bias in a daily perspective.

The dollar lost ground after the March ECB and FOMC meetings. EUR/USD set a new 2016 high at 1.1465. However, the key 1.1495 resistance remained intact. This week’s price action suggests that the topside of EUR/USD became better protected. We see no trigger for a clear directional move in EUR/USD short-term. Medium term, the dollar probably needs really good news from the US to regain substantial ground. The soft Fed approach and risk aversion pushed USD/JPY below the 110.99/114.87 range. The pair reached a new correction low below 108. USD/JPY had moved into oversold territory though, so there was room for a technical rebound this week. A protracted USD/JPY rebound probably needs a sustained improvement global risk sentiment or can official talk on more BOJ easing or ‘verbal interventions’ stop the yen rebound (cf G20)? A move above 110.67 would call off the downside alert.

Sterling ignores BoE policy statement

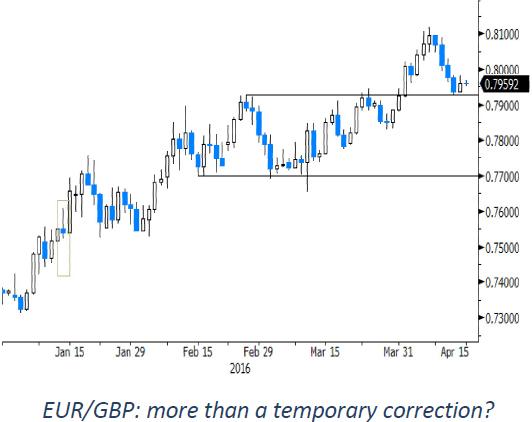

Yesterday morning sterling lost slightly ground ahead of the BoE policy announcement. There were rumours that two policy members seriously considered a rate cut. The BoE as expected left its policy unchanged, while sounding cautious on the economy. The bank elaborated in extenso on the potential impact of a Brexit scenario on the economy and on markets. As the recent fall of sterling was presumably mostly due to uncertainty regarding Brexit, the BoE doubted that it would persist over time. If so, it should also limit its economic impact. In the end, the BoE policy decision had no lasting impact on sterling trading. EUR/GBP closed the session at 0.7960 (from 0.7937); cable finished at 1.4155 (from 1.4204)

Today, only the UK February construction output data will be published. A modest rebound after a poor January figure is expected. Any market reaction to the report will only be of intraday significance at best. So, sterling trading will be at the mercy of global market trends. For now, it looks as if the topside in EUR/GBP is better protected as long as negative headlines on Brexit are avoided.

The technical picture of EUR/GBP improved further as the pair broke above the resistance at 0.7929/31 and 0.8066. The recent sterling decline has been fast, raising the chances for a (temporary) pause, which finally occurred this week. Even so, we assume that sterling sentiment will remain fragile as long as the polls indicate a neck-and-neck race for the 23 June referendum.

This non-exhaustive information is based on short-term forecasts for expected developments on the financial markets. KBC Bank cannot guarantee that these forecasts will materialize and cannot be held liable in any way for direct or consequential loss arising from any use of this document or its content. The document is not intended as personalized investment advice and does not constitute a recommendation to buy, sell or hold investments described herein. Although information has been obtained from and is based upon sources KBC believes to be reliable, KBC does not guarantee the accuracy of this information, which may be incomplete or condensed. All opinions and estimates constitute a KBC judgment as of the data of the report and are subject to change without notice.

Recommended Content

Editors’ Picks

EUR/USD extends gains above 1.0700, focus on key US data

EUR/USD meets fresh demand and rises toward 1.0750 in the European session on Thursday. Renewed US Dollar weakness offsets the risk-off market environment, supporting the pair ahead of the key US GDP and PCE inflation data.

USD/JPY keeps pushing higher, eyes 156.00 ahead of US GDP data

USD/JPY keeps breaking into its highest chart territory since June of 1990 early Thursday, recapturing 155.50 for the first time in 34 years as the Japanese Yen remains vulnerable, despite looming intervention risks. The focus shifts to Thursday's US GDP report and the BoJ decision on Friday.

Gold closes below key $2,318 support, US GDP holds the key

Gold price is breathing a sigh of relief early Thursday after testing offers near $2,315 once again. Broad risk-aversion seems to be helping Gold find a floor, as traders refrain from placing any fresh directional bets on the bright metal ahead of the preliminary reading of the US first-quarter GDP due later on Thursday.

Injective price weakness persists despite over 5.9 million INJ tokens burned

Injective price is trading with a bearish bias, stuck in the lower section of the market range. The bearish outlook abounds despite the network's deflationary efforts to pump the price.

US Q1 GDP Preview: Economic growth set to remain firm in, albeit easing from Q4

The United States Gross Domestic Product (GDP) is seen expanding at an annualized rate of 2.5% in Q1. The current resilience of the US economy bolsters the case for a soft landing.