The global stock markets did not have any sharp trend on Wednesday despite the positive data on increase of the U.S. wholesale inventories for April by 1.1% against expectations of 0.5%. This figure is included in the calculation of the GDP changes. Probably, low investor activity prevents the "rally" from continuation because they are confident about further price growth.

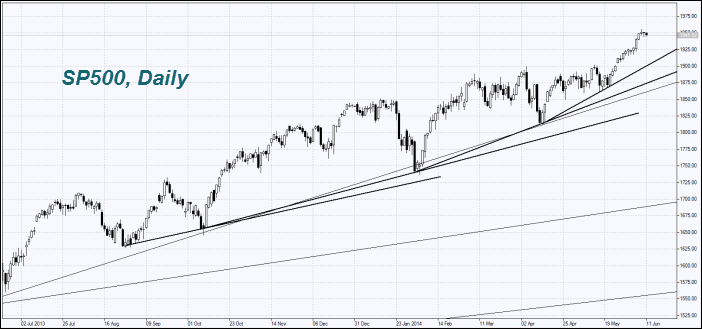

Yesterday trading volume on U.S. exchanges was 17% below the average for three months and made 5.2 billion shares. The S&P 500 index has grown within 32 months at least by 10% without any significant corrections, while its average non stop growth continuation since 1945 has been only 18 months. The last correction was observed only in 2011, from April to October. Note that market participants now expect aggregate profits of the companies included in the S&P 500 to increase in 2014 by 7.4%. There were more optimistic growth forecasts of 9.7% in January. In our opinion, the main growth driver for the U.S. stocks was the QE program or redemption of government bonds by printing money. During the three QE stages, since March 2009, the S&P 500 rose by 188%. Now this program is reduced by $10 billion per month. We do not exclude the U.S. stock market correction along with the QE completion and the Fed's monetary policy tightening (rate hikes). Recall that its next meeting will be held next week. Yesterday the yield of 10-year U.S. government bonds (notes) set a new monthly high at 2.65%. Today we do not expect any significant economic data from the U.S. and the Eurozone.

The U.S. futures, as well as European stocks are falling down this morning. The World Bank (WB) has lowered its forecast for the global economic growth this year from 3.2% to 2.8% in January. The U.S. GDP growth forecast is lowered from 2.8% to 2.1%. The World Bank expects EU economy to grow by 1.1%, Japanese economy by 1.3% this year.

Japanese Nikkei corrected upwards today after yesterday's fall. The MSCI indexes excluded South Korea and Taiwan indexes from the list of indices of developed countries. Thus, only Japan is left among the Southeast Asian countries. This has contributed to increased demand for Japanese stocks from large international hedge funds that invest, focusing on indices composed by MSCI. Tonight at 23-50 СЕТ Industrial Orders in Japan for April will be released. In our opinion, the forecasts are negative.

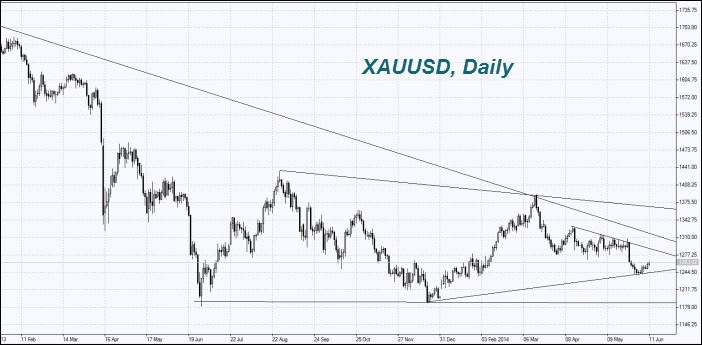

Due to uncertain growth in global stock indices, the price of gold reached a 2-week high. Earlier, we noted that it moves opposite to the U.S. securities market. This can be used to create a personal composite instrument.

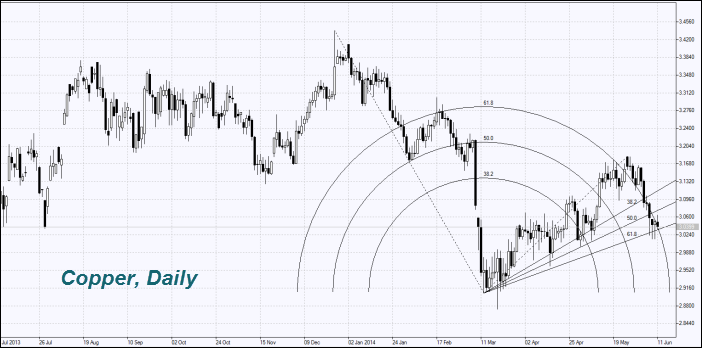

The Copper price stabilized. Investors have not decided yet what is more important - the Qingdao port lending investigation, which could reduce the demand in China or the cumulative reduction of copper reserves on London, New York and Shanghai exchanges by 42% to the lowest level since 2008, indicating that there is a high demand for this metal.

Today the USDA will publish its report containing the forecasts for the crop and stocks of cereals at 16:00 CET, which can affect the quotes. The consensus forecast is presented in the table. Note that the Wheat quotations were supported by forecast of reduction of its harvest in Australia due to El Niño by 1% despite the agricultural land increase by 2%. Investors do not exclude further negative meteorological forecasts.

Recommended Content

Editors’ Picks

AUD/USD rises to two-day high ahead of Aussie CPI

The Aussie Dollar recorded back-to-back positive days against the US Dollar and climbed more than 0.59% on Tuesday, as the US April S&P PMIs were weaker than expected. That spurred speculations that the Federal Reserve could put rate cuts back on the table. The AUD/USD trades at 0.6488 as Wednesday’s Asian session begins.

EUR/USD now refocuses on the 200-day SMA

EUR/USD extended its positive momentum and rose above the 1.0700 yardstick, driven by the intense PMI-led retracement in the US Dollar as well as a prevailing risk-friendly environment in the FX universe.

Gold struggles around $2,325 despite broad US Dollar’s weakness

Gold reversed its direction and rose to the $2,320 area, erasing a large portion of its daily losses in the process. The benchmark 10-year US Treasury bond yield stays in the red below 4.6% following the weak US PMI data and supports XAU/USD.

Ethereum continues hinting at rally following reduced long liquidations

Ethereum has continued showing signs of a potential rally on Tuesday as most coins in the crypto market are also posting gains. This comes amid speculation of a potential decline following FTX ETH sales and normalizing ETH risk reversals.

Australia CPI Preview: Inflation set to remain above target as hopes of early interest-rate cuts fade

An Australian inflation update takes the spotlight this week ahead of critical United States macroeconomic data. The Australian Bureau of Statistics will release two different inflation gauges on Wednesday.